In this article Manoel Bittencourt argues that corruption is killing economic growth and prosperity in Brazil. Using standard economic theory and data he shows that the demonstrations taking place in Brazil are a natural reaction of a population that wants a brighter present in “the country of the future”.

Back in the early 1980s, when I was a kid growing up in Brazil, my late father would tell my brother and I that Brazil was “the country of the future”. Fast forwarding in time, in 2005, when I was a PhD student, I flew from Bristol to Frankfurt and the British Airways aircraft was a Brazilian Embraer 190. As a Brazilian, I confess that at first I felt a sense of trepidation, but then I felt proud that Brazil was already exporting that sort of technologically-advanced equipment to a company such as British Airways. Moving in time again, in 2013, when I was a visiting Professor at Heidelberg University, I watched on TV the massive demonstrations taking place in Brazil and, if I remember well, the main grievances at the time were corruption and poor public services delivery. Moving even closer in time, in 2015 more demonstrations are taking place and the main grievance this time is, well, corruption again (by now everybody has heard of the Petrobrás scandal). Coincidentally enough, in 2005, when Brazil was flying high, the economy was growing at a respectable 3.14% and in 2014, when the demonstrations had already kicked in, at just 0.14% per year.

Given the above, the first question one would ask is: does economic growth matter? I would argue that it does. For instance, using the 70/g rule one can easily predict that an economy growing at a mere 2% per year doubles its income per capita every 35 years (no small feat). Thus, growth matters for economic (and all sorts of) welfare.

The second question one would ask is: okay, if growth matters, then what are the determinants of growth? Making use of a standard undergraduate textbook, Barro (2008), we learn that growth is determined by:

1. Saving rates, which finance investment, and therefore we expect a positive relationship between savings and growth

2. Fertility rates; lower fertility increases capital per worker and productivity, and therefore we expect that lower fertility encourages growth

3. Rule of law (which includes the concept of corruption), provides an environment conducive to production and we expect a positive relationship between rule of law and growth

4. Government consumption; we expect that lower nonproductive government consumption encourages growth

5. Trade openness, which fosters competition and technological transfers, and we expect a positive relationship between trade openness and growth

6. Investment in education and health; an educated and healthy population can use new technologies and also create new technologies, therefore we expect positive relationships between education, health and growth

7. Inflation rates; low inflation means macroeconomic stability, therefore we expect that lower inflation encourages growth

8. Finance, which is needed for investment to take place, and therefore we expect a positive relationship between finance and growth.

In addition, Easterly and Levine (1997) suggest infrastructure, i.e. telephones per worker, paved roads and the quality of the electricity system, as an extra growth determinant. We expect a positive relationship between infrastructure and growth.

Well, now that we know what the growth determinants are and how they affect growth, we can collect economic data on those eight (textbook) growth determinants and see how those determinants fare in Brazil and perhaps understand why Brazil has been deaccelerating recently.

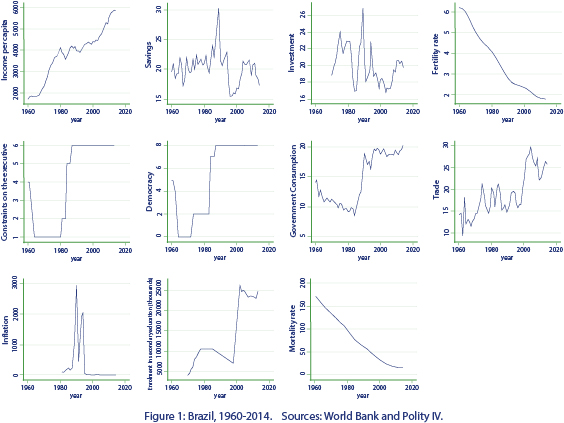

Let’s look at the data then (See Figure 1 below). I downloaded standard data on the growth determinants, mostly from the World Bank and Polity IV websites, and Figure 1 depicts the data. Income per capita is higher than in 1980 and the overall trend is positive. Savings, as percentage of GDP, are lower than in the 1980s and investment, or fixed capital formation, is lower than in the 1980s as well. Fertility is lower than in the 1980s. Constraints on the executive (a proxy for political accountability and checks and balances) and democracy are much higher than in the 1980s. Government consumption, as percentage of GDP, is much higher than in the 1980s, but international trade is higher and inflation is much lower. Secondary education enrolment is much higher and mortality rate is much lower than in the 1980s.

All in all, there are positive signs in the Brazilian economy: on one hand, higher income per capita is the outcome of lower fertility (Brazil is going through its own demographic transition), higher constraints on the executive and democracy (Brazil redemocratised in 1985-1989), more international trade (Brazil started opening up its economy in the 1990s), lower inflation (macroeconomic stabilisation came in 1995 with the Real Plan), more people attending school (and acquiring skills required by a knowledge economy) and lower mortality (a sign of a healthier population).

On the other hand, there are not so positive signs as well: savings and investment are lower than in the 1980s (if income per capita has been growing over time, why are Brazilians not saving and consequently investing more?). Moreover, how easy is it for Brazilians to have a savings account and consequently invest more? Or, what are the incentives for banks to attract more savers, and for people to save and invest in a growing economy? What is happening to consumption? Are Brazilians consuming more instead of saving and investing? Perhaps, once Brazil reaches a particular income threshold Brazilians will start saving more. It remains to be seen though. All the same, understanding savings and investment behaviour is an important question that researchers should look at.

Furthermore, government consumption is higher than in the 1980s and this is one of the burning issues being raised by those demonstrating in the streets of Brazil: poor public services delivery. If public services delivery is poor (as the demonstrators say) and government consumption is higher than in the 1980s, then the burning question is: what is the government consuming then? Well, according to the demonstrators, certainly not better services delivery. Better understanding of how governments spend and consume is another important question that researchers should look at.

Nevertheless, taking the issues raised by the demonstrators a bit further, I visited the Transparency International website for a more in depth look at corruption in Brazil. In 2010 Brazil ranked 69 in the world and Botswana ranked 33. In 2014 Brazil ranked 69 again and Botswana 31 in the world. To be clear, there are 68 countries in the world which are less corrupt than Brazil. Moreover, the World Justice Project gives countries a score of absence of corruption. In 2012-2013 Brazil had a score of 0.52 and Botswana of 0.75. In 2014, Brazil dropped to 0.50 and Botswana to 0.73. Overall, Botswana is a less corrupt country than Brazil (and Botswana also managed to improve its position in the Transparency International rank). Brazil, to say the least, worsened slightly its position, or to put it differently, it showed no improvement in reducing corruption, at least from 2010 onwards.

Well, making use of another standard undergraduate textbook, Jones and Vollrath (2013), and attempting to put everything together now, corruption affects investment negatively (remember that Brazil saves and invests less than in the 1980s and the government consumes more), it raises the costs of production and the incentives to invest are lowered. With less investment, one of the determinants of growth, the economy does not grow as fast as it is possible. Easterly (2002), in his best-selling book, states that “requiring private business people to pay bribes is a direct tax on production, and so we would expect it to lower growth.” Furthermore, Hall and Jones (1999) synthesise the process of growth well when they state “we document that the differences in capital accumulation, productivity, and therefore output per worker are driven by differences in institutions and government policies, which we call social infrastructure” and social infrastructure captures the roles of an environment that favours production over dispersion. Looking at the data, and always keeping standard economic theory and the demonstrators grievances in mind, that seems to be the case in Brazil, i.e. corruption, conspicuous government consumption, lower investment and consequently lower growth. In essence, corruption is either killing investment or growth, we decide. All the same, prosperity in Brazil is going down the drain.

Some would argue that the problems of Brazil are much deeper than what the usual textbook growth determinants suggest, e.g. colonialism, slavery and inequality are usually suggested as historical-structural problems that Brazil has yet to face. I will not argue otherwise. In addition, I will not claim that just looking at the data as I did above is enough to understand Brazil. Looking at the data and at the variables suggested by standard economic theory is just the first step. No doubt that much more is needed, i.e. rigorous economic analysis is needed before we start talking about policy prescription.

However, economics is not rocket science and the demonstrators know all too well that corruption kills growth, and they do not want that to happen. Needless to say, a growing economy keeps its people happy and, according to the 70/g rule, richer, and also its government alive with revenues. And, yes, my father was right, Brazil is (still) the country of the future. Let’s not forget that it has come a long way since the bad-old days of colonialism, slavery, coups, juntas, hyperinflation, default crisis, etc. But it still has some way to go until it builds an even better civil service (and, to be fair, a lot has been done in making the civil service meritocratic and also to train top-level civil servants abroad), and better institutions and checks and balances on government designed, so that the future becomes a brighter present.

About the Author

Manoel Bittencourt is Associate Professor of Economics at the University of Pretoria. He holds a PhD in Economics from the University of Bristol. His research papers have appeared in journals such as Journal of Banking and Finance, Economics of Governance, Economic Modeling, Journal of Policy Modeling and CESifo Forum. In addition, he is a National Research Foundation of South Africa-rated researcher and elected member of the Council of the Economic Society of South Africa.

Manoel Bittencourt is Associate Professor of Economics at the University of Pretoria. He holds a PhD in Economics from the University of Bristol. His research papers have appeared in journals such as Journal of Banking and Finance, Economics of Governance, Economic Modeling, Journal of Policy Modeling and CESifo Forum. In addition, he is a National Research Foundation of South Africa-rated researcher and elected member of the Council of the Economic Society of South Africa.

References

1. Barro, Robert (2008). Macroeconomics: a modern approach. (Thomson South-Western, Mason).

2. Easterly, William (2002). The Elusive Quest for Growth. (Cambridge, Massachusetts & London, England: The MIT Press).

3. Hall, Robert and Charles Jones (1999). “Why do some countries produce so much more output per worker than others?” (Quarterly Journal of Economics, 114 (1):83-116).

4. Jones, Charles and Vollrath, Dietrich. (2013). Introduction to Economic Growth. (New York, W.W. Norton).

{kind=link}