I. Introduction

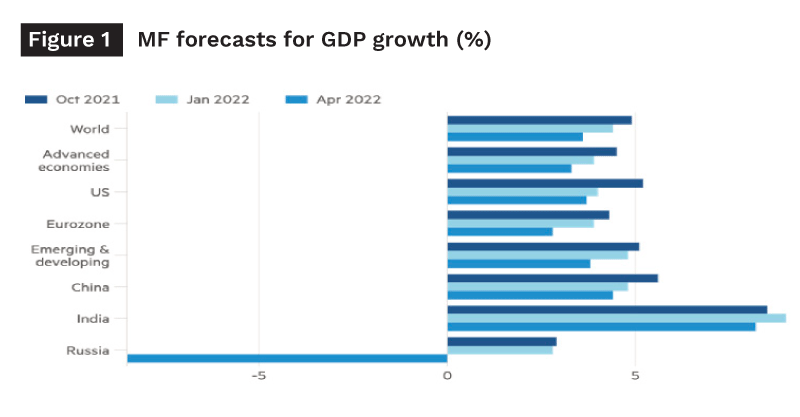

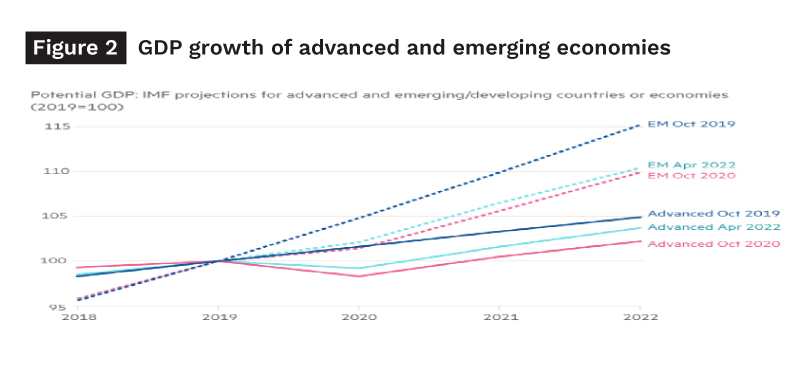

The International Monetary Fund (IMF) in its latest assessment of the world economy has downgraded prospects for economic growth and also expects higher inflation. The IMF Report (2022) notes: “Global growth is projected to slow from an estimated 6.1 percent in 2021 to 3.6 percent in 2022 and 2023. This is 0.8 and 0.2 percentage points lower for 2022 and 2023 than projected in January. For 2022, global economic growth has been reduced from 4.5 percent to 2.5 percent. Beyond 2023, global growth is forecast to decline to about 3.3 percent over the medium term” (see figures 1 and 2).

The IMF report forecasts that inflation will rise now to nearly 6 per cent annually in the advanced economies and 9 per cent in the developing countries (as indicated in figure 3). This is the result of higher commodity prices and other supply shortages. As Jason Furman of Harvard’s Kennedy School insists, this inflation is “demand-driven and persistent”. As in the 1970s, strong demand could sustain a wage-price spiral as workers seek to maintain real incomes (cited in Wolf, 2022).

For the UK, too, the growth forecast remains low for 2022 and this is expected to continue into the whole of next year, with growth averaging zero over those twelve months. Moreover, soaring energy prices will push the UK economy into recession later this year. The annual rate of inflation in the UK is currently 7 per cent. The Bank of England expects inflation to rise to double digits by September 2022. The Bank of England raised interest rates from 0.75 per cent to 1 per cent in April 2022 to combat rising inflation, but there is no guarantee that it will be enough to bring commodities prices down. In short, the UK economy is being hit by a series of shocks. The upheaval caused by a succession of lockdowns to contain COVID-19 has been followed by the war in Ukraine, which has further inflamed the market price of gas, oil, and a series of other vital commodities (Siddiqui, 2022).

The ongoing war in Ukraine is raising the risk of global food shortage and the possibility of famine, as exports of foodgrains, fertilisers, and energy have been disrupted. As a result of this, the prices of essential commodities have risen sharply. It seems that the global economy is heading towards an economic recession. These events remind us of the vulnerability of food supply and food availability, particularly in poor countries.

António Guterres, secretary-general of the UN, said on 26 May 2022 that the conflict in Ukraine, coming on top of existing pressures on food prices, “threatens to tip tens of millions of people over the edge into food insecurity followed by malnutrition, mass hunger and famine”. Therefore, it is crucial for a country to pursue the policy of “food self-sufficiency” and “food sovereignty” (Siddiqui, 2021a).

There are several critical factors that would push the global economy into a deep recession. For example, in recent months in the United States the sharp rise in prices of essential commodities is adding the risk of stagflation in the economy, which is expected to be heading into deep recession by 2023. In the EU countries, costs and the prices of commodities are rising, while the situation is worse in many developing countries, where food crises are looming. If such a large economy as that of the US is heading towards recession, this will adversely affect the global economy and have an even more severe impact on the developing countries, who happen to be food importers as well. According to Robin Brooks, chief economist of the Institute of International Finance, the confluence of these shocks suggests the world economy is already in trouble. “We’re in another global recession scare now, except this time we think it’s for real” (Financial Times, 2022).

Financial markets are showing signs of a looming crisis. The MSCI world index of equities fell more than 1.5 per cent in the past week, more than 5 per cent in May, and more than 18 per cent since a peak in early January. Mr Joshi, the chief strategist at BCA Research, notes: “The last time that the ‘everything sell-off’ star alignment happened was in early 1981 when Paul Volcker’s Fed broke the back of inflation and turned stagflation into an outright recession.” He further says, “The US National Bureau of Economic Research defines a recession as ‘a significant decline in economic activity that is spread across the economy and that lasts more than a few months’” (cited in Giles, 2022).

There is no doubt that wars add to economic crises. For instance, the Vietnam War created a huge adverse impact on US public finances and, during the Korean War, prices rose sharply. The present war in Ukraine seems to be no exception and this war directly involves oil and gas, while Ukraine is also an exporter of food grain. This will raise the prices of vital commodities worldwide and hit people in poor countries hard (Wolf, 2022). In most countries, the central banks are now planning to raise interest rates in the coming months to counteract rising prices. This would reduce aggregate demand and push the world economy towards higher unemployment and stagnation.

However, the US Federal Reserve, which sets interest rates, claims that it will have little impact on the real economy. The current Fed chairman, Jerome Powell, argues that this is because of a money wages push, which in turn arises because people expect inflation to occur, and this increases interest rates. Money wages lag behind price rises, meaning that real wages decline. This means that inflation is due to the money wage push. As people expect abatement of inflation, this will end the money wage push and thus bring down inflation. This adjustment will remain confined to the sphere of expected prices and a slowdown in the economy will be short-lived. Such arguments are incorrect. It is said that the current inflation is due to the Ukraine war, which has created scarcities of essential commodities. This explanation is far from the whole truth and the war may cause price rises.

There is little evidence that any disruption of supplies has taken place in the US market due to the Ukraine war. But the key reason that commodity prices have risen faster than wages in the US is owing to an autonomous increase in profit margins. There might be some shortages because of supply chain disruptions due to the pandemic, but the rise in prices is more pronounced and seems to be due to MNCs’ speculative behaviour. This may also be due to the easy availability of credit with the policy of quantitative easing until recently, as well as the US Federal Reserve keeping interest rates at near zero, which created a liquidity overhang. Therefore, Keynes supported the “socialisation of investment” to avoid the Great Depression eighty years ago, and an active fiscal policy along with an appropriate monetary policy. This will mean subservience of financial capital to the needs of the whole of society. However, the free flow of capital is an important component of the current neoliberal globalisation and any control over capital movements is not acceptable to international finance (Siddiqui and Armstrong, 2017).

II. Looming Economic Recession

Here, I would first like to define economic recession and describe past recessions. The IMF and World Bank prefer to characterise a global recession as a year in which the average person experiences a drop in real income. They highlight 1975, 1982, 1991, 2008, and 2020 as the dates of the previous five global recessions (Siddiqui, 2019a; also, 2019b).

Recessions can happen for various reasons, and they are generally associated with rising unemployment and falling household incomes and spending. During the mid-1970s, recession was driven by oil price shocks and industrial disputes. Meanwhile, the recession of the early 1980s stemmed from high inflation and interest rates (Dahle and Siddiqui, 1989). And the early 1990s recession was sparked by high interest rates, falling house prices, and an overvalued exchange rate. The recession of the 2008 financial crisis was due to excessive credits, a mortgage crisis, and high interest rates, alongside excesses and imbalances in the banking and real estate sectors (Siddiqui, 2020a; also, 2019c).

A recession can have a devastating impact on people’s everyday finances, as low-income households witness a decline in incomes and loss of employment. For example, in the US and the EU, the wealthiest 1 per cent recovered from the 2008 crisis at a pre-crisis level within a few years, while it took much longer – around 2017 – for the bottom half of the wealth distribution in the West to regain pre-crisis wealth levels (Economist, 2022). This assumes that the government in these countries relies on monetary policy, not fiscal policy. The rich mostly prefer monetary policy to fiscal policy as a policy tool of macro-stabilisation, because monetary policy tends to benefit the rich disproportionately as they hold most of the assets whose price rises, while the poor rely on “trickle-down”.

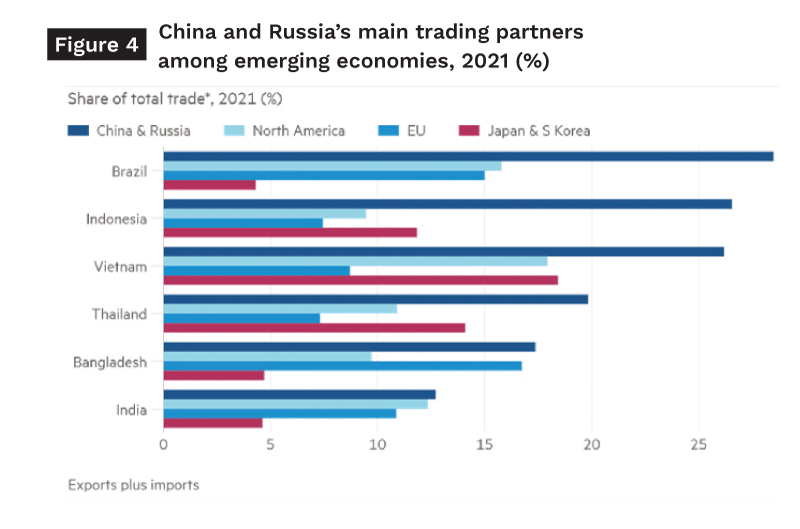

During the Ukraine war, the US has imposed sanctions against Russia. However, besides being a major global supplier of oil and gas, Russia is also an important supplier of foodgrains and fertilisers, and any sanctions will not only increase the prices of these commodities but also disrupt their supply (see figure 4).

However, unlike Russia, China is an economic superpower and it is wrong to ignore the Chinese economy and its prospects in the near future (Siddiqui, 2020b). The Chinese economy is the second-largest and its performance will have a major impact on the global economy. As figure 5 shows, Chinese output and consumer spending has declined in 2022 compared to the previous year. The contraction of its output will have a major impact on raw material imports and thus adversely affect income and employment in many developing countries. At this critical juncture, cooperation with China is needed to resolve the increasing foreign debts of the developing countries.

Recent statistics reinforce concerns about the Chinese economy’s growth prospects for 2022-3. China accounts for 19 per cent of the world’s total output, and it is now the largest world trading and foreign investor country. So the rest of the world cannot ignore its recovery and economic performance, after it overcomes COVID-19, especially because of its impact on global supply chains and its imports of goods and services from the rest of the world (Siddiqui, 2020c; 2020d).

For example, with COVID-19 lockdowns ending, ships are queuing outside Chinese ports and industries. But recently, its retail sectors have started to contract. Retail sales had fallen 11 per cent by April 2022, while industrial production was down 3 per cent. China’s home sales also dropped more in April 2022 compared to April 2019, when its economy went into reverse, despite the People’s Bank of China loosening monetary policy to encourage borrowing and spending.

In the US, the other global economic powerhouse, the economy is still suffering from the legacy of the pandemic and an excessive fiscal stimulus that arguably ran the economy too hot and generated high inflation, even with modest energy price rises. The US Fed has now moved decisively into a phase of tightening monetary policy to slow growth and bring inflation down. The Fed chair, Jay Powell, stated last month that the Fed would continue to raise interest rates until it saw that inflation was returning to the 2 per cent target. He was not concerned about rising unemployment. Many in financial markets think that with such a policy alone, it might be hard to achieve low inflation. Krishna Guha from the Global Policy and Central Bank Strategy, based in Washington, warns, “Bringing inflation under control without a recession and large increase in unemployment. . . will be challenging.”

The Bank of England now expects “a major recession” from late 2023 to early 2024, according to a recent note to investors entitled, “Why the coming recession will be worse than expected,” although the bank predicts that the economy could pick up in mid-2024. Perhaps things will get worse before they get better.

The other powerful economic block, namely the EU, is not showing good signs either. Inflation reached 7.6 per cent in May 2022 and prices in the EU are rising much faster than incomes, as a result adversely impacting living standards. Rising prices will reduce spending and overall household demand and, thus, economic recovery from the pandemic seems to be far away. Already, the recent forecast from the European Commission expects stagnation in late 2022.

The European Commission expects the economy to get over this difficult period and return to normal growth of about 0.5 per cent by August 2022, but economists think that the crisis will have a longer effect. Christian Schulz, an economist at Citi, says that the official forecasts appear too optimistic and it is more likely there will be “virtually no growth for the rest of the year”. If Europe is facing difficulty in adjusting to much higher energy prices, then the developing countries will find it even harder to deal with the sharp rise in food prices, which account on average for more than 30 per cent of expenditure in developing countries.

Currently, Sri Lanka is facing economic collapse and bankruptcy. However, the country has faithfully followed the IMF’s recommendations for several years, including tax reductions on foreign investors, investing disproportionately in infrastructure and export-led growth, while ignoring the domestic agriculture and industrial sectors. The government hoped that the increased concession to the rich would lead to higher investment and the economy would grow, but this miracle did not happen. Now, Sri Lanka has made some dire choices, also faced by many other poor countries, when it decided last week to default on its foreign debt for the first time. This, it said, was necessary to use its hard currency to import fuel, food, and medicine.

India, meanwhile, intensified the foodgrain problems in other emerging economies by reneging on a pledge not to ban the export of grain this week. Due to the ongoing war in Ukraine, wheat prices in India rose again and are up more than 60 per cent within the last three months.

Ukraine and Russia together constitute about 30 per cent of the world’s total wheat exports. Many poor developing countries are heavily dependent on food imports, and foodgrain supplies are being disrupted due to the conflict in Ukraine. Moreover, the war itself is affecting the cultivation of land and production of foodgrain. Ukraine alone accounts for 30 per cent of the world’s maize exports, which is also the staple crop consumed in Africa.

Russia is also the main supplier of chemical fertilisers for many developing countries. Fertiliser is an important input of the “Green Revolution” technology and the disruption of its supply from Russia will have a severe impact on its prices; and a reduction in the supply of fertilisers would adversely affect foodgrain output in the developing countries. Prior to the Ukraine war, on 10 February 2022, and soon after the start of the war, on 10 April, within such a short period foodgrain prices alone rose by 17 per cent (see figure 6).

The most vulnerable countries are those that have witnessed civil wars, such as Afghanistan, Congo, Mali, Nigeria, Somalia, Yemen, Sudan, and South Sudan. These counties have had a history of conflicts and long-term political instability and poor governance. Thus, their vulnerability to famines and loss of life has been affected by the disruptions in domestic food production. So, it is rooted in and related to poverty and the prevailing domestic crisis. These countries also had debt crises and were forced to adopt neoliberal economic policies, including trade liberalisation and the abandonment of “food self-sufficiency”, under IMF pressure. As a result, these countries experienced a sharp fall in per capita foodgrain output from the mid-1990s (Siddiqui, 2019d).

The free trade policy is backed by the World Trade Organisation, which is based on David Ricardo’s policy of “comparative advantage” (Siddiqui, 2018), meaning that the developing countries should abandon achieving food self-sufficiency. “Free trade” in agricultural commodities is fully supported by mainstream economists in the name of efficiency and competition (Gallaghar and Robinson, 1953). However, the mainstream economic policy is also known as neoclassical orthodoxy. On such views, Joan Robinson, a prominent Keynesian economist, said: “One of the main effects of the orthodox traditional economics was … a plan for explaining to the privileged class that their position was morally right and was necessary for the welfare of society” (Robinson, 1937: 76).

We should mention here that, at present, the advanced capitalist countries have a surplus in food grains and are looking for overseas markets. The poor tropical countries have been advised by the IMF to produce cash crops for exports to earn foreign exchange, repay their foreign debts, and overcome the foreign exchange crisis. As a result, these countries neglected their foodgrain production, and resources were moved into the cultivation of cash crops. All these culminated in a situation where they began to increase imports of foodgrains and the advanced countries were able to get rid of their surplus.

Neoliberal capitalism is defined so as to explain the phase of capitalism where restrictions on the global flows of capital and products are removed. As a result, such development leads to the centralisation of capital. The capital is allowed to take advantage of low wages and produce and sell to the global market. The role of the state is changed, so that, instead of defending the interests of most of the population, including workers and farmers, it becomes the defender of the interests of foreign investors and, further, this means the withdrawal of state support from farmers and petty producers.

It is widely recognised that economic stagnation and the long-term decline in growth have led to an extraordinary increase in economic inequality, which has been emphasised by Thomas Piketty’s book Capital in the Twenty-First Century. These two issues, namely deepening stagnation and growing inequality, have created a severe crisis in the mainstream economist theories.

During the Great Depression, unemployment in the US rose to 25 percent in 1934. It was in this context that Keynes became critical of the neoclassical orthodoxy in his well-known book The General Theory of Employment, Interest and Money (1936). He attacked the notion of Say’s Law that “supply creates its own demand”. He did not accept the notion that full-employment equilibrium exists in the long run. Instead, Keynes contended, “When effective demand is deficient, there is under-employment of labour in the sense that there are men who are unemployed who would be willing to work at less than the existing real wage.”

The recent globalisation and the collapse of the Soviet Union and the integration of Eastern Europe and China into the advanced capitalist economies saw the multinational corporations (MNCs) taking advantage of cheap resources and expanding global markets, and establishing global value chains as the dominant form of capitalism in the twenty-first century. In recent years, we have witnessed not only consumer goods and high tech, but capital equipment and advanced research, being produced in several countries or regions, integrated through global value chain production. For instance, according to the International Labour Organisation, between 1999 and 2018, employment via global value chains increased from nearly 300 to 500 million, constituting one in five jobs in the world (World Development Report, 2020).

The global value chain productions represent the latest form of monopoly capital in the twenty-first century. Now this is how surplus value is created and captured from workers in the developing countries, where there is a large pool of unemployed people who are hired by MNCs based in the advanced economies at low wages and to make higher profits. This exploitation is called by the mainstream economists “value-added”. The current globalisation and free trade and capital movements allow MNCs to take advantage of wage differentials and intensify the exploitation of workers and resources in the developing countries (Suwandi, 2019; Siddiqui, 2020e; Lin and Ha-Joon, 2009).

The World Development Report (WDR) claims that “global value chains” are helping the developing countries’ economic development by raising incomes, employment, and living conditions (WDR, 2020). However, in reality, most developing countries have witnessed rising income inequalities and unemployment, and intensification of the exploitation of their workers.

The “global value chains” are based on David Ricardo’s “comparative advantage trade” theory, which assumes that free-market transactions take place between companies with no power differentials. According to the report, encouraging the development of participation in global value chains is the road to more jobs and sustainable growth. For example, the WDR (2020: XII) notes, “Participation in global value chains can deliver a double dividend. First, firms are more likely to specialise in the tasks in which they are most productive. Second, firms can gain from connections with foreign firms, which pass on the best managerial and technological practices. As a result, countries enjoy faster income growth and falling poverty.” The report further emphasises that “global value chains boost incomes, create better jobs and reduce poverty… that global value chain-led development generates mutual gains for lead firms (concentrated in developed countries) and supplier firms (concentrated in developing countries)” (WDR, 2020: 3).

The comparative advantage theory is based on mainstream economists’ assumptions of perfect competition. On this notion, Joan Robinson has noted that perfect competition is most unrealistic for the present phase of capitalism and such an assumption is a myth and capitalist competition is characterised by the tendency toward monopolistic competition (Robinson, 1937). The “free trade theory” ignores the fact that the MNCs wield unprecedented economic power over the workers and suppliers in the developing countries. The increased competition to attract foreign investors and to facilitate higher profits leads to lower wage rates. Contrary to the claims, the “comparative advantage” theory does not provide mutual gains to all trading countries.

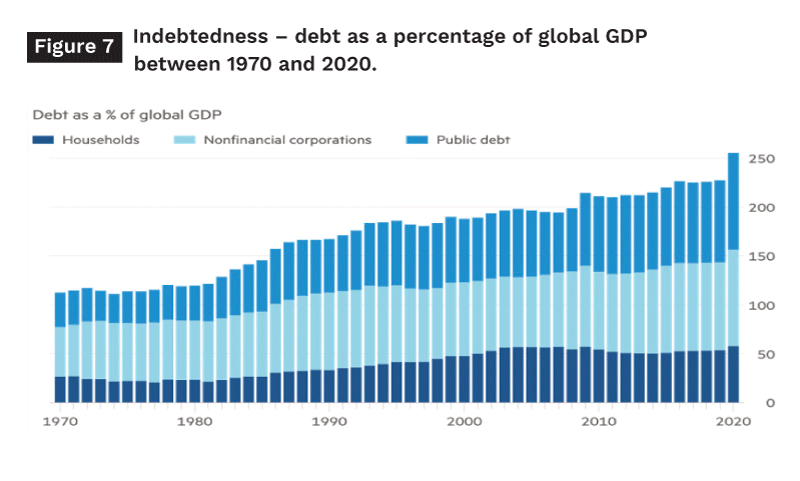

The upshot is that the world economy is now in a debt trap (see figure 7). Levels of debt and equity valuations are so high that central banks cannot tighten monetary policy without posing a serious threat to economic stability. In short, the world economy now carries explosive levels of debt and is in a debt trap.

However, despite the sharp rise in Asia’s share of global GDP, especially due to the Chinese and East Asian economies (Siddiqui, 2021b), Europe and North America dominate in terms of top leading global companies and investment in R&D. The advanced economies are defined as high-income and have a disproportionately greater share of the global GDP. According to the IMF, these countries will still account for 57 per cent of global output, against China’s 19 per cent, at market prices in 2022. They also issue all the main reserve currencies (see figure 8). China holds more than US$3 trillion in foreign currency reserves, while the US holds none. But the US can print them. Moreover, the advanced economies, led by the US, are not just a strong economic power but also have the largest and most modern armies.

III. Conclusion

During the COVID-19 pandemic, there was a huge contraction of the global GDP and a rise in unemployment. In fact, even before the pandemic, the global economy was already slowing down. Ever since the global financial crisis of 2008 following the collapsed housing bubble, the world economy never fully recovered. There were short-term recoveries but these lasted for a short period and did not experience steady, smooth upward growth.

Since the late 1990s, the growth rates of Asia’s economies are faster than the West and are most likely to become the dominant economy of the world (Siddiqui, 2016; also, Siddiqui and Armstrong, 2017). The Asian countries constitute nearly 60 per cent of the world’s population. According to the IMF, the average real output per head of these Asian economies will increase from 9 per cent of that of the advanced economies in 2000 to 23 per cent in 2022. This upward trend will most likely continue in the coming years. In the past, we have ample evidence that the level of “financial fragility” is dangerously high in much of the West, especially the US and the UK, and China, too, reflecting very high levels of wealth and income inequality, now combined in the West with the pandemic crisis.

In the past, we have ample evidence that the level of “financial fragility” is dangerously high in much of the West, especially the US and the UK, and China, too, reflecting very high levels of wealth and income inequality, now combined in the West with the pandemic crisis.

During the COVID-19 crisis, we saw that the big, rich corporations were able to increase their wealth and assets disproportionately. There is a need to scale down rising inequality within countries. Beyond strengthening regulation of finance, business and political leaders must stop being so mulishly unquestioning of billionaire wealth and act to reduce it. And a progressive and inclusive policy is needed to increase real income support for vulnerable households and more progressive taxes on income, wealth, and profits.

At present, inflation continues to soar and the increasing cost of living hits households across the nation. Most economists are predicting another recession by next year. It will mean a phase of both high unemployment and inflation. To combat inflation, the US and the UK will most likely adopt the tightening cycle of monetary policy. The risk of recession, worsened by defaults and financial disruption, could be high. In addition to this, it seems that the economic recession would have worse implications due to growing tensions between Russia, China, and the West.

Due to the current war in Ukraine, the key affected areas are economic sanctions, disruption in trade, rise in commodity prices, financial instability, and economic uncertainty. It is obvious that, under such circumstances, global cooperation seems to be very important. However, the rising tensions and conflicts will push toward economic collapse and the destruction of the environment.

About the Author

Dr Kalim Siddiqui is an economist, specialising in International Political Economy, Development Economics, International Trade, and International Economics. His work, which combines elements of international political economy and development economics, economic policy, economic history and international trade, often challenges prevailing orthodoxy about which policies promote overall development in less developed countries. Kalim teaches international economics at the Department of Accounting, Finance and Economics, University of Huddersfield, U.K.. He has taught economics since 1989 at various universities in Norway and U.K.

Dr Kalim Siddiqui is an economist, specialising in International Political Economy, Development Economics, International Trade, and International Economics. His work, which combines elements of international political economy and development economics, economic policy, economic history and international trade, often challenges prevailing orthodoxy about which policies promote overall development in less developed countries. Kalim teaches international economics at the Department of Accounting, Finance and Economics, University of Huddersfield, U.K.. He has taught economics since 1989 at various universities in Norway and U.K.

References

- Dahle, T. and Siddiqui, K. (1989). “World Economy Heading Towards Recession”, Bergens Tidende, (in Norwegian) 3 July, Bergen, Norway

- Economist. (2022). “A toxic mix of recession risks hangs over the world economy”, 9 April, London. https://www.economist.com/leaders/2022/04/09/a-toxic-mix-of-recession-risks-hangs-over-the-world-economy

- Financial Times. (2022). 2 June, London. https://www.ft.com/content/517fbdac-507a-4e55-97fd-55375c1fe1f

- Gallaghar, J. and Robinson, R. (1953). “Imperialism of Free Trade”, Economic History Review, 6(1): 1-15.

- Giles, C. (2022). “Is the global economy heading for recession?”, Financial Times, 20 May, London. https://www.ft.com/content/35b31fb0-f8ad-4557-9d95-267e0ed958eb

- IMF. (2022). World Economic Outlook, April, Washington DC: IMF. https://www.imf.org/en / Publications/WEO/Issues/2022/0 /19/world economic-outlook-april -2022

- Lin, J. and Ha-Joon, C. (2009) “Should Industrial Policy in Developing Countries Conform to

- Comparative Advantage or Defy It?” Development Policy Review, 27(5): 483-502.

- Robinson, Joan. (1937). Essays in the Theory of Employment, New York: Macmillan, p.176.

- Siddiqui, K. (2016). “Will the Growth of the BRICs Cause a Shift in the Global Balance of Economic Power in the 21st Century?” International Journal of Political Economy, 45(4): 315-38.

- Siddiqui, K. and Armstrong, P. (2017). “Capital Control Reconsidered: Financialization and Economic Policy”, International Review of Applied Economics 32(6): 1-19, March.

- Siddiqui, K. (2018a). “U.S. – China Trade War: The Reasons Behind and Its Impact on the Global Economy”, World Financial Review, Nov/Dec, p.62-8.

- Siddiqui, K. (2018b). “David Ricardo’s Comparative Advantage and Developing Countries: Myth and Reality”, International Critical Thought, 8(3): 1-28.

- Siddiqui, K. (2019a). “Financialisation, Neoliberalism and Economic Crises in the Advanced Economies”, World Financial Review, May-June, 22-30.

- Siddiqui, K. (2019b). “Government Debts and Fiscal Deficits in the UK: A Critical Review”, World Review of Political Economy, 10(1): 40-68.

- Siddiqui, K. (2019c). “The US Economy, Global Imbalances under Crapitalism: A Critical Review”, Istanbul Journal of Economics 69(2): 175-205.

- Siddiqui, K. (2019d). “Economic Transformation of China and India: A Comparative Political Economy Perspective”, Asian Profile, 47(3): 243-59.

- Siddiqui, K. (2020a). “The US Dollar and the World Economy: A critical review”, Athens Journal of Economics and Business. 6(1): 21-44.

- Siddiqui, K. (2020b). “The Rise of the Chinese Economy and Growing Concerns in the United States”, World Financial Review, Sept/Oct, 40-9.

- Siddiqui, K. (2020c). The Impact of Covid-19 on the Global Economy, World Financial Review, May-June, 25-31.

- Siddiqui, K. (2020d). “Prospects of a Multipolar World and the Role of Emerging Economies”, World Financial Review, Nov/Dec, 65-77.

- Siddiqui, K. (2020e). “Globalisation, International Trade and the Developing Countries”, European Financial Review, August/September, 60-71.

- Siddiqui, K. (2021a). “Agriculture, Sustainable Development, and the Government Policy in the Developing Countries”, World Financial Review, Jan.-Feb., 44-59.

- Siddiqui, K. (2021b). “Can 21st Century be an Asian Century?”, Asian Profile, 49(1): 1-19, March.

- Siddiqui, K. (2022). “Problems of Inflation, War in Ukraine, and the Risk of Stagflation”, European Financial Review, April/May, 5-13.

- Suwandi, I. (2019). Value Chains: The new economic imperialism, New York: Monthly Review Press.

- Wolf, Martin. (2022) “War in Ukraine is causing a many-sided economic shock”, Financial Times, 26 April, London. https://www.ft.com/content/d4bde497-edbf-4baa-bfa3-d06b07c63f79

- World Development Report. (2020). Trading for Development in the Age of Global Value Chains, Washington DC: World Bank.

{kind=link}