By Karel Cool, Christophe Angoulvant and Brian Rogers

The article gives data on global investment in InsurTech ventures and discusses the most common strategies and business models these companies have pursued: technology-upgrade, customer-disintermediation, and transaction-enabling. The models are illustrated with a brief review of three companies: Shift Technology, Cuvva and ZhongAn. The article concludes with a discussion of whether and how InsurTech ventures are threats or opportunities for incumbent insurers.

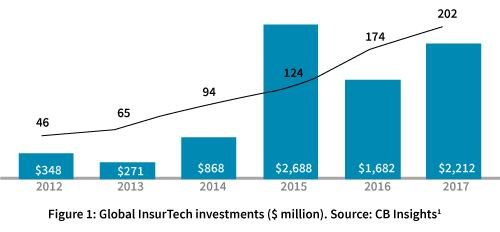

How large is the InsurTech wave?

According to CB Insights, global InsurTech investment continues to climb. The number of investment deals reached a five year high in 2017 at 202, and the value of these investments at $2.2 billion was up 31% from 2016 (see Figure 1).

InsurTechs have sprung up in many segments, including car insurance (e.g. pay-as-you-drive), home insurance (e.g. intrusion, leakage detection, video expertise of insurance claims), health insurer services (e.g. tele-consultation, doctor appointment booking, health coaching programs) and retirement planning services (e.g. simulation tools such as robo-advisors, video chats).

InsurTech in non-life insurance

InsurTech disrupters have especially targeted non-life insurance. Figure 2 gives a high-level view of the nonlife insurance supply chain.2 Taking the car insurance supply chain as an example, suppliers include car body shops and towing services. Administration and claims management refer to the back-office handling of policies and claims. Distribution and customer relationship are the client-facing activities performed by a variety of channels, including agents and brokers, call centers, price-comparison engines (such as Confused.com in the U.K.) and the insurers’ own sales channels. Figure 2 also shows where a number of the InsurTech firms have targeted their entry. We discuss below the most common strategies and business models these companies have pursued.

The “technology upgrade” business model

A first type of disrupter model targets some of the upstream activities in the insurance supply chain. The new entrants seek to improve the efficiency of incumbents by providing upgraded technological solutions, such as faster claims settlement (e.g. Snapsheet), machine learning towards fraud detection (e.g. Shift Technology), and data mining and analytics (e.g. Cytora). According to a recent count,3 the large majority of InsurTechs have adopted this model to enter the insurance sphere.

The technology upgrade model tends to be collaborative, generating win-win opportunities for insurers and start-ups alike. For example, Shift Technology, a Paris-based start-up, provides artificial intelligence solutions for insurance fraud detection and automated claims management (see sidebar – Shift Technology). Founded in 2015, the company now has 50 insurance clients and operates in 19 countries. While these InsurTechs disrupt activities the incumbents perform, they can also be valuable partners. Burdened by legacy costs and long overdue automation, traditional insurers have much to gain from working with start-ups in administration and claims management. The long-term competitive advantage of these InsurTechs is based on keeping a technology efficiency edge over the incumbents and continuing to create win-win opportunities.

The “customer disintermediation” business model

Opportunities for collaboration also exist downstream in the customer facing activities, but the relationship tends to be more competitive. Take Berlin-based simplesurance. As a digital broker, it offers its e-commerce partners a plug-and-play cross-selling digital solution that allows end-customers to buy insurance with just one click. While creating new business for traditional insurers such as Allianz, it also positions itself between the customer and the insurer as a new gateway or tollgate. While there are collaborative benefits in the short term, over the longer-term, simplesurance could become more of a competitor.

Cuvva, the mobile-only insurer from the UK4 is another such a player (see sidebar – Cuvva). Its pay-as-you-drive insurance by the hour is an extension of traditional insurance policies in the UK and as such does not lure away clients from incumbents. On the other hand, its subscription-based car insurance policy, which allows users who pay a minimal monthly fee to top up their insurance when the car is driven, and to switch off this extra payment when the car sits idle, is potentially disruptive for incumbents.

The InsurTechs that pursue customer disintermediation seek to compete by creating additional value, lowering prices, or both, to attract customers. Their long-term competitive advantage is dependent on efficiency, keeping costs low and innovating new customer value. The ongoing value creation actions by Cuvva illustrate this strategy and sustainability imperative.

The “transaction-enabling” business model

A new class of InsurTechs, led by Shanghai-based ZhongAn, is embracing a very different vision and business model. Rather than making existing insurance models more efficient, or substituting insurers in their supply chain, they are positioning insurance as a complement to transactions. The emergence of the many platforms with transactions of modest value, and buyers and sellers with short transaction histories, frequently make transaction risk a stumbling block. By offering tailored insurance products at “pocket money” rates, ZhongAn seeks to de-risk and enable these transactions.

ZhongAn’s most popular product has been the Shipping Return Policy. In the Chinese context, buyers are often concerned about the origin and quality of the products they buy. To remove the anxiety of return shipping costs, ZhongAn developed a policy for buyers who wish to return unsatisfactory products, and a policy for sellers to cover the shipping costs of a replacement product. The cost is a mere RMB 0.15–3.3 (€ 0.02–0.4) per policy for sellers, and RMB 0.2–9.9

(€ 0.03 –1.3) per policy for buyers.

ZhongAn’s business model is similar to the original Google model in web search and transactions. Google’s AdWords and AdSense programs have allowed many millions of people to advertise their products and services at a very small cost to millions of customers, thus enabling transactions. Prior to these programs, similar transactions were much more difficult to complete, as advertising on alternative media was prohibitive for small transactions.

Similar to Google, ZhongAn’s business model has enabled millions of transactions between buyers and suppliers by de-risking the transactions at a very small cost.5 This creates benefits for buyers and sellers, and thus for the ecosystem, which in turns draws in more buyers and sellers, thereby accelerating the growth of the ecosystem. ZhongAn benefits from these positive effects, which is why its own growth has been stellar (see sidebar – ZhongAn Online P&C Insurance Co).

The long-term advantage in this business model is very different from that of Shift Technology and Cuvva. ZhongAn relies on its superior ability to tailor insurance products for discrete, temporary situations and offer the products at very modest premiums. The company analyses vast amounts of data on customer behaviour in different transaction scenarios and customers’ hesitation points in the decision-making process. The company states, “We have broken down the online [car insurance] purchase process into 45 parts, and monitor and analyse data flows from each part. If we notice that users spend too much time in one part, then we know something may be wrong with it, or it has potential to be optimised.”6

Opportunities for insurance incumbents

The burgeoning innovative activity of the FinTechs offers significant opportunities to the insurance incumbents. Disintermediation negatively affects incumbents’ revenues, but it also offers acquisition and partnership opportunities. Allianz, AXA, Generali, Munich Re and Swiss Re have been particularly active. Very similar to the relationship between biotechnology startups and large pharmaceutical companies that built a biotech capability, incumbents that build a FinTech capability may significantly enhance their competitive position by selecting from a portfolio of FinTechs.

The challenge from the transaction-enabling business models to incumbents is different from the technology-upgrade and customer-disintermediation models. As the former is embedded in the transactions of platforms, which often have critical mass characteristics leading to dominance in their ecosystems, it may prove difficult for latecomers to dislodge early InsurTech movers. Moreover, early movers may leverage their position across platforms and ecosystems into a long-term advantage. Incumbents need to analyse whether such transaction-enabling strategies can be applied in the markets they operate and whether and how they can pre-empt the position of transaction enablers. Similar to the field of web and mobile search, where Google built an almost unassailable position – and power, a similar reality may develop in some insurance markets.

About the Authors

Karel Cool (left) is Professor of Strategy and BP Chaired Professor of European Competitiveness at INSEAD. Christophe Angoulvant (center) is Senior Partner and Global Head of Insurance at Roland Berger. Dr Brian Rogers (right) is Research Editor at Swiss Re Institute.

Karel Cool (left) is Professor of Strategy and BP Chaired Professor of European Competitiveness at INSEAD. Christophe Angoulvant (center) is Senior Partner and Global Head of Insurance at Roland Berger. Dr Brian Rogers (right) is Research Editor at Swiss Re Institute.

References

1. CB Insights. Fintech trends to watch in 2018. January 2018.

2. C. Angoulvant, K. Cool and B. Rogers. InsurTech is hitting critical mass, INSEAD Knowledge, November 2017.https://knowledge.insead.edu/blog/insead-blog/insurtech-is-hitting-critical-mass-7791

3.Willis Towers Watson – CB Insights. Quarterly Insurtech briefing. January 2018. https://www.willistowerswatson.com/en/insights/2018/01/quarterly-insurtech-briefing-Q4-2017

4. B. Rogers, K. Cool and C. Angoulvant (2018). Disrupting the Car Insurance Industry. INSEAD Knowledge. January 2018. https://knowledge.insead.edu/blog/insead-blog/disrupting-the-car-insurance-industry-8126

5. ZhongAn also provides customer credit, credit insurance and many other services.

6. http://www.scmp.com/busness/companies/article/2131948/big-data-and-ai-future-car-insurance-according-chinas-first

7. Willis Towers Watson – CB Insights. Quarterly Insurtech briefing, January 2018.

{kind=link}