By Douglas Cumming, Grant Fleming, Sofia Johan & Dorra Najar

This article summarises recent research on the role of law, culture and corruption on venture capital and private equity fund structures, governance and performance. The authors focus on the role of law and corruption on two aspects of venture capital and private equity investment: the structure of manager compensation, and performance outcomes.

Since the 2007 financial crisis, there has been significant and growing concern in the venture capital and private equity industries worldwide of the role of corruption in influencing venture capital and private equity fund manager activities. For example, the high profile law firm S.J. Berwin noted in their Private Equity Comment1 that regulators are paying significantly more attention to venture capital fund manager corruption, particularly with respect to bribery, and environmental, social and governance issues. As they commented, ‘[i]t makes good business sense, therefore, for [fund] managers to understand the legal issues in every country in which the fund does business, and to take active steps to ensure that responsible business practices are adopted throughout the portfolio’. Indeed, a lack of understanding by the private equity industry on differences in legal practices, corruption and cultural norms around bribery could result in longer term (negative) effects for the industry. S.J. Berwin expressed particular concern with international venture capital and private equity transactions where exposure to firms could result in ‘corrupt linkages’ to local, regional and national governments.

The Role of Corruption, Culture and Law on Fund Manager Compensation

Venture capital and private equity fund managers are financial intermediaries between institutional investors and entrepreneurial firms. Venture capital and private equity funds are typically set up as limited partnerships whereby the institutional investors are the limited partners and the fund manager is the general partner.2Institutional investors include pension funds (which are most common across countries), insurance companies, banks and endowments, etc. Venture capital and private equity funds typically have a finite life of 10-13 years. This life-span enables fund managers time to select appropriate investees and manage such investments to fruition. A typical investment in an entrepreneurial firm can take from 2-7 years from first investment to the exit date. Entrepreneurial firms typically lack income, revenue and/or cash flows to pay interest on debt and dividends on equity; hence, returns to institutional investors are in the form of capital gains upon exit (such as an IPO or acquisition for successful entrepreneurial firms, or a write-off for unsuccessful firms).

Venture capital and private equity fund managers are compensated with a two-part fee. The first part is a fixed fee which is commonly 1-3% of the fund’s assets in the U.S., and paid annually. This enables an appropriate annual salary for the fund managers and enables the fund managers to meet overhead costs over the life-span of the fund, particularly in times prior to the realisation of investments in the investee firms. The second component is the performance fee, or carried interest, which is commonly 20% of the profits earned by successful fund investments. Fixed fees are higher and performance fees are lower among younger funds, which is consistent with a learning model whereby risk averse fund managers are more likely to prefer more certain compensation when their abilities are unknown to themselves. Fund managers may face clawbacks of their fees, which means that institutional investors in funds can retract performance fees paid out in the early years of the fund in the event of poor performance in latter years. Institutional investors into funds can state in limited partnership contracts that payment terms come in the form of cash or share distributions.

We expect countries with less corruption and superior legal settings to affect managerial compensation in a way that better aligns the interests of fund managers with their investors. Where there is less corruption, there is less uncertainty and risk of misappropriation of financial resources. Fund managers who believe that their efforts and higher risk taking will pay off will therefore prefer lower fixed fees and higher performance fees in countries with less corruption. Moreover, institutional investors are less likely to demand clawbacks rights on fees in countries with less corruption, and less likely to demand cash-only distributions.

Corruption is distinct from legal conditions in a country, and therefore we consider legal settings alongside measures of corruption. Legal conditions can be measured in a variety of ways, such as the many indices developed by La Porta et al. (1998)3 and others. The traditional La Porta et al. indices include efficiency of judicial system, rule of law, risk of expropriation, risk of contract repudiation, and shareholder rights. A weighted average of these indices was adopted by Berkowitz et al.4 and referred to as the Legality Index. It is natural to expect these indices to matter for cross-country determinants in fees, not because these indices were developed for limited partnerships, but rather because they affect the uncertainty faced by fund managers in carrying out their investments in those countries and as such their expected incomes. Risk averse fund managers prefer higher fixed fees in exchange for lower performance fees in order to garner a more certain income stream in countries with weaker legal conditions.

Similarly, as compensation contracts are the outcome of bargaining between fund managers and their institutional investors, and bargaining depends on culture in different countries, we may expect cultural measures developed by Hofstede to matter in setting fees. Perhaps most notably, Power Distance, Individualism and Masculinity influence the degree of inequality amongst contracting parties, and hence are likely to be associated with higher fixed fees and lower performance fees. The intuition, perhaps best illustrated by Power Distance, is as follows. Power Distance reflects the degree to which those in control or with bargaining power are able to dictate terms and those not in control are happy to accept terms. Typically bargaining power is greater among institutional investors than fund managers since raising a venture capital fund is challenging, particularly among first time fund managers in less developed countries where Power Distance is more pronounced. Institutional investors might be more inclined to prefer lower performance fees with higher fixed fees, not higher performance fees with lower fixed fees, if they do not want fund managers to be able to earn extremely large incomes from the contractual arrangement and thereby have a shift in the Power Distance between the parties. Similarly, Uncertainty Avoidance is also more likely to be associated with higher fixed fees and lower performance fees if both institutional investors and fund managers seek more predictable payoffs in terms of fees.

H1: Fixed management fee percentages will be in higher in countries with more corruption, weaker legal conditions, and in countries with more Power Distance, Individualism, Masculinity, and Uncertainty Avoidance.

H2: Carried interest performance fee percentages will be higher in countries with less corruption, stronger legal conditions, and in countries with less Power Distance, Individualism, Masculinity, and Uncertainty Avoidance.

While fund managers benefit from higher fixed fees and lower performance fees in countries with poor legal conditions, institutional investors nevertheless face a particularly pronounced risk of lower profits among funds in countries with poor laws. Institutional investors can lower the downside costs of low returns with the mechanism of a ‘clawback’. A clawback means institutional investors can retract performance fees paid out in the early years of the fund to the fund manager in the event of poor performance in its latter years, thereby reducing the overall compensation paid to fund managers in the event of poor performance. What may have been a friendly investment environment when the initial investments were made may be hostile by the time divestments have to be made over the life of the fund. The clawback allows the investors to recover excess distributions upon liquidation of the fund. We therefore expect clawbacks to be more frequently employed in countries with poorer legal conditions and in countries with more pronounced corruption.

H3: Clawbacks of fund manager fees in the event of poor performance are more common in countries with greater corruption, a weaker Legality Index and greater Power Distance.

We further expect legal conditions to influence the mode of distribution of fund profits to institutional investors in terms of cash versus share distributions. Poor legal conditions increase the financial risk of share positions in entrepreneurial firms; therefore, all else being equal, the greater the uncertainty created by a lower quality legal environment, the greater the probability of a cash-only distribution policy in the setup of a private fund.

H4: The weaker the legal environment, and the greater the corruption, the greater the probability of covenants mandating cash-only distributions from fund managers to institutional investors.

Johan and Najar’s5 regression results for fixed fees and performance fees are presented show that legal conditions significantly (at the 1% level) negatively influence fixed fees and positively influence performance fees, respectively, consistent with H1 and H2. The economic significance is such that the model predicts that a move from India (Legality index is 12.) to Canada (Legality Index is 21.13), for example, gives rise to a reduction in fixed fees by 1.16% and an increase in performance fees by 4.92%, which are very economically significant effects (and the actual difference, indicated in Table 2, is 1.67% for fixed fees and 1.33% for performance fees). English legal origin countries have lower fixed fees and higher performance fees, respectively, consistent with H1 since English legal origin countries offer superior flexibility and investor protection.3Similarly, the data shows higher rule of law countries have lower fixed fees, while higher efficiency of the judiciary countries have higher performance fees. Overall, the data provide very strong support for 1 regarding the effect of legality on fixed and performance fees.

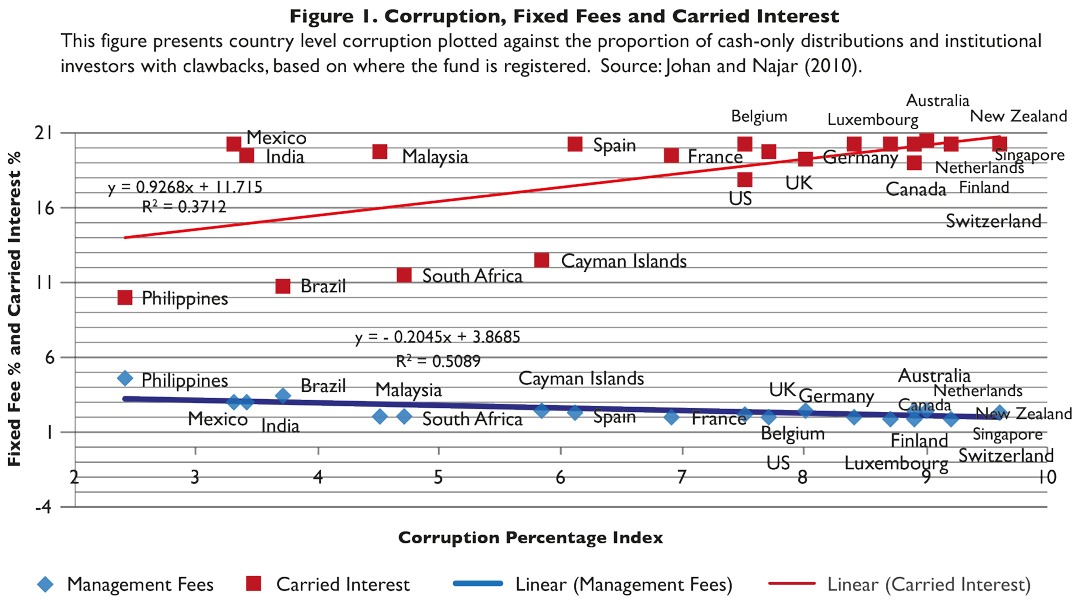

Corruption is one of five components of the aggregated Legality Index. The data show that for all specifications, the corruption index is significantly negatively related to fixed fees. Also, corruption is significantly positively related to performance fees, but the statistical significance of the effect depends on the model specification. A move from India (corruption index of 3.4) to Canada (corruption index 8.63), for example, gives rise to lower fixed fees by 1.84% and higher performance fees by 4.2%. Again, the data are strongly consistent with the predicted effect in H1 and H2. The effect of corruption on fees is graphically illustrated in Figure 1.

Johan and Najar5 also analyse the relation between legality and payment terms to a fund’s institutional investors in terms of cash versus share distributions from realised investments in entrepreneurial firms. The Logit regression indicates a robust relation between legality and cash distributions, consistent with H4. An improvement in legal conditions such as from India to Canada, for example, gives a reduction in the probability of cash only distributions by 31.65%. The components on the legality index that appear to be the most significant are the rule of law and corruption. The strong effect of corruption on cash distributions and clawbacks is graphically illustrated in Figure 2.

The Role of Law and Corruption in Investment Returns

We expect that Legality matters for venture capital and private equity returns for a number of reasons. Higher legality implies stronger investor protection, and therefore a more active stock market which affords an exit outcome for venture capital deals. Furthermore, better legal conditions facilitate better enforcement of private equity contracts, and help to alleviate information asymmetry between transacting parties, both at the time of initial investment and at the time of exit (consistent with La Porta et al.).3 Private equity funds see to maximise returns, and new owner(s) will pay more when information asymmetries are lowest, which is in countries with better legal conditions. IPOs are more likely in countries with better legal conditions, and buybacks are more likely in countries with worse legal conditions.2Therefore, all else being equal, higher returns are expected in countries with better legal conditions.

H5: Venture capital and private equity returns are higher in countries with superior law quality.

While legal systems may matter, it is also possible that private equity managers can mitigate the potential costs of inefficient legal systems (and thus the likelihood of expropriation of rents) by actively changing the governance and incentive structures inside private companies. By contrast, non-active private equity funds that do not bring about organisational change to alleviate the expected costs of corruption would likely experience lower returns in countries with higher levels of corruption.

H6: Venture capital and private equity returns are higher in countries with higher levels of corruption.

The regressions in Cumming et al.6 provide strong support for H5 for the Legality index. On average, Cumming et al. estimate that a 1-point improvement in legality is associated with a 17.5% increase in IRRs. For example, moving from Malaysia (legality 15.506) to Singapore (Legality 18.291) gives rise to an estimated 48.7% increase in expected returns, which illustrates that the legality effect is economically large. In some specifications, however, collinearity across explanatory variables is problematic and as such this finding is not robust in every one of their model specifications.

Cumming et al.’s 6 data also provides strong support for H6. Indeed the effect of corruption on returns is significant across all six regression models. Higher levels of corruption (indicated by lower values of the Corruption Perception Index) are associated with higher IRRs, and this effect is statistically significant at least the 5% level in all models.

The statistical and economic significance associated with H5 and H6 is graphically illustrated in Figure 3 which presents the results for median levels by country. Figure 3 shows a negative relation between the corruption index and returns, consistent with H6 and the regressions models, and a positive relation between corruption and legality, consistent with H5 and the regressions models.

Concluding Remarks

In this paper we have reviewed theory and evidence on how law and corruption influence manager compensation and performance outcomes. Our research has been motivated by growing popular concern since the financial crisis over manager compensation and the ‘economic benefits’ of venture capital and private equity investing. Media and political debate has questioned whether compensation structures in asset management lead to the appropriate alignment of interest and to ‘value creating’ behavior by fund managers.

Institutional investors have not, until recently, been able to draw upon empirical analysis to improve their understanding of the impact of legal and political systems on private equity returns around the world. The evidence reviewed herein is a first contribution to what we hope is a growing body of work on this topic. The data are strongly consistent with the view that fund fee structures and performance strongly depend on law, culture and corruption.

About the Authors

Douglas Cumming, J.D., Ph.D., CFA, is a Professor of Finance and Entrepreneurship and the Ontario Research Chair at the Schulich School of Business, York University. His research interests include venture capital, private equity, hedge funds, entrepreneurship, and law and finance.

Grant Fleming, Ph.D., had worked in private capital markets for over 10 years, with a particular focus on private equity, credit, and distressed opportunities. He is a partner at Continuity Capital Partners established in 2010 and operating from offices in Australian and Hong Kong. From 2010-2010 Grant was a senior professional at Wilshire Associates.

Sofia Johan, LL.B (Liverpool), LL.M. in International Economic Law (Warwick), Ph.D. in Law and Economics (Tilburg), is the Extramural Research Fellow at the Tilburg Law and Economics Centre (TILEC) in The Netherlands and Adjunct Professor of Law and Finance at the Schulich School of Business, York University.

Dorra Najar is an associate professor of finance at Ipag Business School in Paris (France). She received her Ph.D in Management Science from the University Paris Dauphine in 2012. Her research revolves around corporate finance, law and finance, private equity /venture capital and market surveillance.

References

The data used to test H1 – H4 come mainly from a survey conducted over the period December 2009 and March 2010. These data are described by Johan and Najar (2010). Survey data were gathered for a final sample of 123 funds in 23 countries.

1.http://www.sjberwin.com/latestpublicationdetails.aspx?title=privateequitycomment; On the political and economic debate see, for example, discussion of the regulation after the mid-2007 financial crisis in The Economist 19 November 2009, “Europe’s War on Hedge Funds”.

2.Cumming, D.J., and Johan, S.A. (2013).Venture Capital and Private Equity Contracting: An International Perspective, Second Edition, San Diego: Elsevier.

3.La Porta, Rafael, Florencio Lopez-de-Silanes, Andrei Shleifer, and Robert Vishny (1998). “Law and finance,” Journal of Political Economy 106(6), 1113-1155.

4.Berkowitz, D., Pistor, K and Richard, J.F. (2003). “Economic development, legality, and the transplant effect,” European Economic Review, 47, 165-195.

5.Johan, S., and Najar, D. (2010). “The role of corruption, culture and law in fund manager fees,” Journal of Business Ethics, 95(2), 147-172.

6.Cumming, D.J. Fleming, G, Johan, S., and Takeuchi, M. (2010). “Corruption, legality and buyout returns,” Journal of Business Ethics, 95(2), 173-193.

{kind=link}