By Michel-Henry Bouchet and Robert Isaak

In this article, the authors advocate policies to counter the decoupling of finance from the real economy of productive job-creation resulting from short-term global hyperfinance and misguided government regulations: eg. future bank bailouts should be conditioned upon including ratios of new lending to start-ups and small firms with the greatest scaling up potential for employment.

The information technology revolution combined with globalisation has spawned Hyperfinance in which high frequency short-term gains have become the major priority of many financial institutions. The obvious excesses due largely to lack of concerted financial regulation resulted in the financial crisis of 2008. The government reforms instituted since this time have largely encouraged banks to keep a higher ratio of reserves and have dampened their higher risk lending to would-be start-ups and small-to-middle-sized firms, which are the source of the majority of new jobs in the global economy. As Wehinger observes: “Small- and medium-sized enterprises (SMEs) play a significant role in their economies as key generators of employment and income, and as drivers of innovation and growth. SMEs employ more than half of the private sector labour force in OECD economies”.1 The decoupling between the underlying economic system and global finance has resulted in frustrated attempts to regulate financial intermediation.

The issue of concerted regulation of the global financial system seems close to “real utopia projects” that have been developed in the 1990s by the Havens Center at the University of Wisconsin whose aim was exploring a wide range of proposals and models for radical socio-economic and institutional change. However, eight years after the inception of the global finance crisis, with combining symptoms of stock and bond markets bubbles, a fundamental alternative to global market-driven economic system lacks the optimism of the will that Antonio Gramsci considered essential to implement institutional innovations for transforming the world. Freewheeling global finance is as unregulated as before the crisis.

The short-term focus and risk aversion of Hyperfinance has a number of consequences of which three have long-term structural ramifications: (1) The emergence of Hyperfinance in the 1980s led to a distortion in the distribution of corporate profits, with rising dividends and stock buybacks at the expense of capital investment. In the US economy, the share of fixed capital investment in GDP declined to 13% in 2009 from 20% on the eve of the financial crisis, hence back to its mid-1970s level.2 (2) Banking deregulation intensified the emergence of financial innovations, such as securitisation and derivatives, at the expense of productive investment financing in the so-called ‘real economy’, with deeply-rooted impact on productivity and long-term growth trends. The Institute of International Finance, the representative of the global banking industry, deployed intensive lobbying to resist tighter financial regulation, including of non-bank financial services, opposing mandatory minimum haircut requirements and stricter control.3 (3) National regulatory authorities’ attempts to stem systemic risk in global finance with higher capitalisation ratios have resulted in a combination of larger capital holdings coupled with shrinking assets, hence at the expense of credits. In order to achieve improved capital adequacy, capital-constrained banks in developed and developing countries have resorted to collecting outstanding loans or have become reluctant to approve new lending. The resulting credit crunch has further aggravated the crisis.

The not-surprising result of this decoupling is an increase in mass unemployment and underemployment in most countries, particularly amongst the young. The government policies of bailing out the banks in trouble tend to ignore this socio-economic consequence in favour of established financial interests that work to prevent any over-regulation of derivatives and other financial instruments, resulting in a self-fulfilling spiral of low employment growth even if there has been very modest economic recovery since 2008. In a situation of rising employment, the overall contractual quality is poor, given the short-term focus of job contracts resulting in widespread ‘precariousness’.

This article posits potential solutions to cope with this dilemma by proposing conditions on any further bank bailouts, which include ratios of new lending to start-ups and small firms favouring those which leverage or have the greatest scope for scaling up in terms of future employment and long-term innovation. Another common sense solution would be to apply a scaling of capitalisation ratios depending on the bank’s willingness to finance productive and employment-generating investment.

1. The decline in traditional banking intermediation

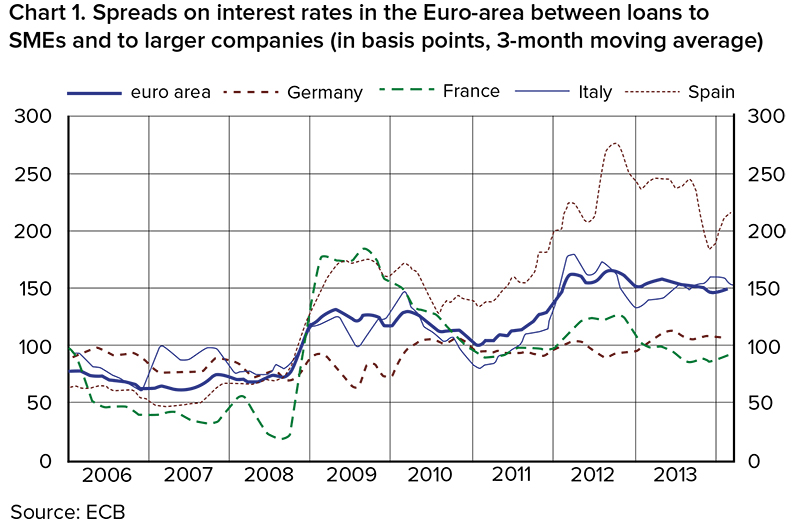

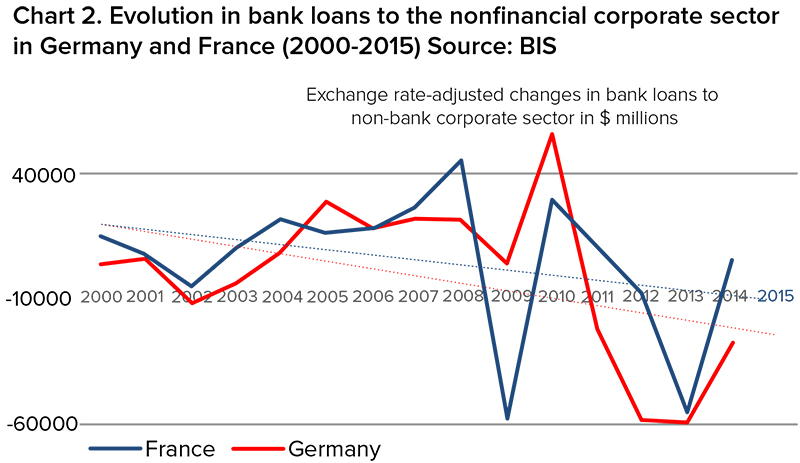

In the EU zone, SMEs play a key role in driving growth and employment. They constitute about 99% of all euro area firms, employ around two-thirds of the euro area’s workforce and generate 60% of value added. According to the European Commission, some 21.6 million SMEs in the non-financial sector employ 88.8 million people and generate 3,666 trillion euros in value added — illustrating how critical SMEs are for employment.4 Access to bank credit is thus crucial in maintaining economic momentum. As the ECB observes: “SMEs are relatively more dependent on bank finance and thus more likely to be affected by banks’ increased risk aversion than larger firms”.5 Not only SMEs suffered from reduced access to bank lending since the outbreak of the financial crisis in 2008, but also from tighter credit conditions. Between end-2008 and mid-2015, bank loans dropped by 13%, i.e., back to their mid-2007 level.6 In addition, the following chart (see Chart 1 above) illustrates the sharp spread between rates on loans to SMEs and to larger enterprises, i.e., the credit volume shrunk while the cost rose.The decline in bank lending to the corporate sector was synchronised in most European countries, particularly in Germany and France. French and German banks have been under pressure to reduce balance sheet leverage since 2008. Faced with tight competition for issuing fresh capital, European banks relied on asset restructuring via sale or run-off. As PwC notices regarding the specific situation of the European banking system compared to the US: “Europe’s medium-sized enterprises do not typically enjoy the same sort of access to bond markets as their counterparts in the US. European bond issuance has strengthened during 2012 and 2013 but total bank loans still comprise the large majority of European corporate debt, compared with less than 30% in the US.”7 Because of limited securitisation markets and protracted economic weakness, bank loans dropped sharply in two successive waves, first in 2009 as a way to improve the assets-to-capital ratios, and again in 2013 in the midst of an anemic regional economic recovery with disappointing corporate earnings and stubborn unemployment. (see Chart 2 below)

European banking authorities regularly take the pulses of the corporate sector to measure and compare across countries bank lending offer and bank lending demand. Most polls of SMEs between 2009 and 2013 show that shrinking bank credit would stem more from a decline in corporate demand than from tighter credit access. Concisely, SMEs would spontaneously cut their demand for bank loans. The reason is likely that bankruptcies surged in the aftermath of the global crisis while the economic environment sharply deteriorated, hence inciting SMEs to prudent financial management.

In France, SMEs’ loan demand shrunk after the global crisis due to a decline in economic activity and market expectations. The result was that 25% of these small companies had no banking liabilities in their balance sheets.8 According to Banque de France, the annual growth rate of banking credits to SMEs dropped to only 2.5% in mid-2015 from 8% the year before.9 A gradual process of bank disintermediation took place since 2008 and accelerated more recently. The share of banking credit in corporate debt dropped to only 61% at end-2015 from 74% in 2008.10 This disintermediation has hurt SME’s access to financing much more strongly than large companies that have access to a wide range of market financing tools. In France, the consequence of tighter banking regulations on credit has been more pronounced than in other European countries, with a larger impact on SMEs activities, on investment, and on job creation. Stubborn high unemployment, reaching more than 11% in late 2015, illustrates the perverse effect of the decoupling between finance and real economic growth.

In Germany, the rise in bank loans has been slower though the demand for loans remained very depressed, hence the percentage of SME’s managers who did not feel constrained bank credit access was one of the highest in the EU, namely 88% compared with 75% in France, and only 45% in Ireland and 47% in Greece.11

In Spain and Italy, under-regulated and overexposed banks strongly cut lending to the corporate sector at the time of the financial crisis. SMEs suffered a typical scissor effect, facing higher rates of interest on shrinking credits. The level of lending rates was substantially higher for Spanish and Italian SMEs than for firms in France and Germany, but also the premia SMEs paid over and above the rates charged for larger enterprises increased substantially after the eruption of the crisis, particularly in 2011 and 2012. The increase in the spread of interest rates paid on small sized loans reflected the impact of the sovereign debt crisis on the financing costs of banks, with higher bank refinancing costs being then passed on to their SME customers. The volatility of bank lending to the corporate sectors of the Euro-zone’s distressed countries, namely Italy, Spain and Greece was brutal in 200912 Spanish companies suffered the most from the abrupt tightening in bank lending standards. Between 2007 and 2009, bank loans shrunk by more than $25 billion. In the meantime, unemployment in Spain surged to 26% of the working population in mid-2013. Worse, youth unemployment in Spain sharply rose from around 18% on the eve of the crisis in 2006-07 to a peak of 55% in mid-2013.

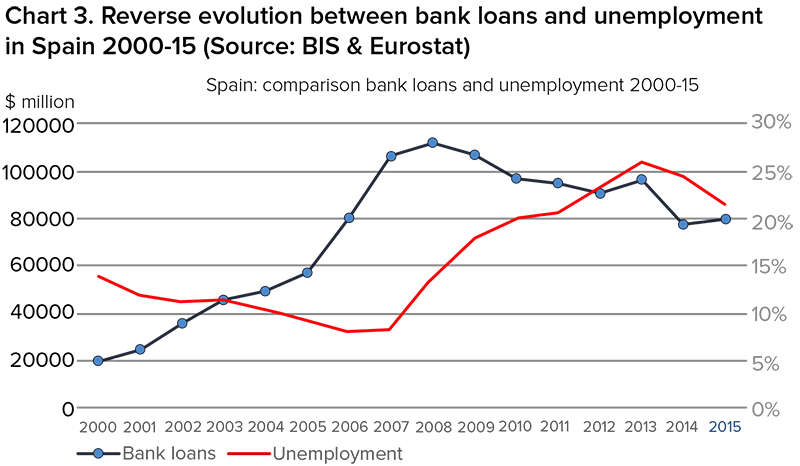

The Chart 3 cast light on the “scissor effect” between the sharp reduction in bank loans to Spain’s nonfinancial sector and rising unemployment in the 2008-2013 period, while the Spanish labour market shed nearly 3.5 million jobs. During 2014, when banks started to lend more to the nonfinancial companies, with strong incentives from European monetary authorities, the process reversed itself and employment grew by half a million people. Consequently, while remaining stubbornly high, the unemployment rate declined to 20%. (see Chart 3 below)

The solvency problem of Spain’s weakest banks during the Great Recession caused a reduction in credit supply and employment. This credit supply shock produced a negative impact on company business activities and on employment. The poor health of the weak banks caused significant employment losses at firms of all sizes. At the level of firms, the additional employment losses are in the range between 6 and 7 percentage points.13 Spanish SMEs’ creditworthiness and financial health deteriorated more sharply than those of large firms, in particular — profits, liquidity buffers and economic prospects, hence exacerbating the financial fragility of this group of firms, and the negative impact on employment. To illustrate this tighter bank credit access for Spanish SMEs, the proportion of approved loan applications reached only 40% in 2012, compared with more than 55% in Italy. It reached a bottom of 25% for Greek SMEs.14

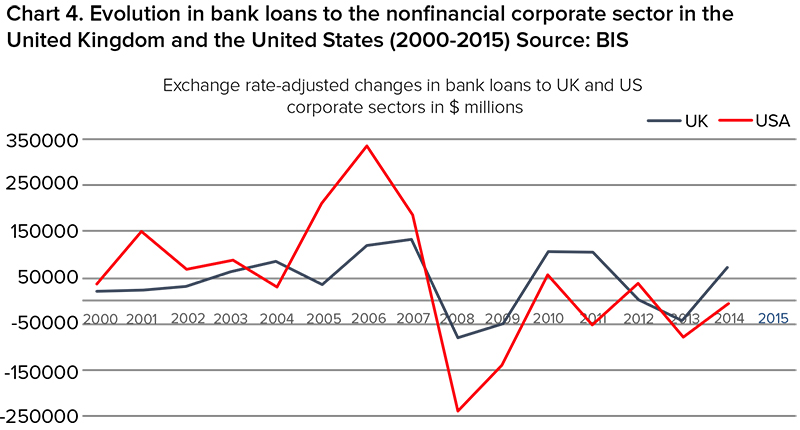

In the UK, bank overdrafts and term loans dropped significantly from 2008-2009 to 2011-12: from 39% to 14% in overdrafts, and from 11% to 7% in term loans.15 SMEs suffered credit restrictions accordingly. (see Chart 4 below)

In the US economy as in most industrial countries, small businesses are critical to fueling the nation’s economic growth. They employ roughly half of all Americans and account for more than 60 percent of net new jobs.16 Their ability to generate new jobs depends in large part on access to credit. In the wake of the protracted recession, SME demand for credit waned as they faced the immediate challenges of weak sales and heightened business uncertainty. The credit crunch hit SMEs much more than larger globalised companies relatively. The share of all small business loans dropped from roughly 35% in the 1995-2000 period to 30% in 2007 dropping to only 20% in 2015.17 The credit shock that SMEs suffered from during the financial crisis resulted in massive job losses that averaged nearly 800,000 per month between November 2008 and April 2009 as the unemployment rate climbed.18 Net job losses rose much more sharply in small businesses than in large businesses, particularly in 2008-09.

Still more dramatically, jobs at SMEs fell 40% during the recession and represented 60% of total private sector job losses according to the US Bureau of Labor Statistics. While the number of start-ups averaged roughly 620,00 between 1998 and 2007 on the eve of the financial crisis, the number of new business formations dropped by more than 10% during the six following years while the size of new businesses also declined. Within the category of SMEs, the very small companies (i.e., <4 employees) have suffered the most from the recession. A sharp increase in net job losses occurred in 2008-09 for this category of US companies.

2. German and British exceptions within Europe

The general economic outlook since 2008 reduced an already slowing demand. And 35% of SMEs surveyed in the European Union noted the success rates for finance sought severely declined between 2007 and 2010 — particularly in the UK, but also in Germany and to a lesser extent in France.19 Banks were the most envisaged sources of finance in the 2011-2013 period.20 However, high tech start-ups were less likely to use bank finance and faced more difficulties than low-tech start-ups in raising bank finance.21 Northern EU countries had greater ease of access to loans in 2007-2010 than those to the south and France and the US had greater ease of access than did Germany or the UK.22

Germany clearly was set apart immediately after the crisis in creating more jobs than in other countries through SMEs: between 2009 and 2013 alone more than 160,000 SMEs were set up, creating more than 1.5 million new jobs for a total of 16.7 million in 2013. Yet a dichotomy emerged here with most jobs created by existing firms taking advantage of access to finance, state aid and public procurement, while the conditions including financing for new start-ups were not as positive in Germany as in other peer EU economies. However, in terms of access to finance, the proportion of rejected loan applications for SMEs is only a sixth of the EU average (2.5% versus 14.4%).23 The demographic aging crisis could lead to a paucity of entrepreneurs willing to start-up companies in the future in Germany. While the Angela Merkel policy of open welcome for refugees may well help to restock Germany with more young entrepreneurs in the long run, it is apt to require an expensive transition of several years in terms of training and positioning in order to bring such a vision to fruition.

Curiously, initially in 2009 after the 2008-9 financial crisis, lending growth rates for SMEs was stronger than for businesses overall in the United Kingdom. But as of late 2009 through 2011 lending growth rates for all small and medium-sized businesses (SMEs) turned negative and were below that for large companies.24 After rising in 2013, both the availability and demand for credit for small business fell sharply in 2014.

According to the Bank of England’s credit conditions survey, demand for bank lending was expected to increase for all except small businesses in 2015.25 The sharply negative shift in lending growth for SMEs has significant implications for employment. In 2013 there were over 1.2 million firms in the UK: 99.5% of these were SMEs with fewer than 250 employees, which employed 51% of the workforce (81.5 % were micro enterprises which less than 10 employees).26 Of course, in terms of SME lending the stock of SME loans and loans for new British SME businesses marked a general downward trend even before the financial crisis, showing only a slight improvement during 2013. New loans had fallen by more than half from their peak in 2008 to a low point at the beginning of 2013.27 Nevertheless, SMEs added some 700,000 new jobs in the UK from 2008 to 2010, a 7% increase. This business rebound was stimulated by a business environment conducive to SMEs, particularly in terms of giving entrepreneurs a second chance, responsive administration and internationalisation.28 However, while finance is more difficult in a number of other EU member states, it remained hard for SMEs to get financing, particularly in terms of bank lending.

3. Policy alternatives to remedy unemployment through credit enhancements to SMEs

Government bailouts of banks have proceeded with few conditions requiring banks to pay attention to the impact of their lending upon employment. It is important to set ‘job-creating’ conditions on any further bank bail-outs which include ratios of new lending to start-ups and small firms favouring those which leverage or have the greatest scope for scaling up in terms of future employment and long-term innovation.

1) Innovation itself, of course, is no guarantee of greater employment growth and can even have the opposite effect if new technology replaces more human hiring than it generates. So a contextual trade-off should be a part of the conditionality of loans with persuasive positions on why a particular culture is apt to generate more jobs than employment lost in anticipated technological developments within a given time period. If indexes can be created to measure the rise and fall of real estate prices and stock market valuations, there is no inherent reason why indexes of job losses vs. gains cannot be measured in certain economic sectors given applied innovations.

2) A second related solution would be to apply a scaling of capitalisation ratios depending on the bank’s willingness to finance productive and employment-generating investment. Government could rank specific sectors as the most likely to generate scalable employment country by country (eg. health care in Germany and the US).

3) A third avenue would be to compensate for the relatively higher lending risk of SMEs by providing banks with several offsetting incentives such as specific guarantees and privileged refinancing conditions for job-creating investment in SMEs. The cost of these support measures should be weighed against the sheer cost of unemployment that reaches in France at least €32 billion, supported by the State agency UNEDIC. While the US economic recovery has brought unemployment back to its floor of 5%, unemployment remains an acute economic problem in the European Union, with the unemployment rate reaching above 20% in some countries. To reduce unemployment, the European Commission has emphasised the need for member states to give priority to the provision of services and compensation. The cost of unemployment varies from a high of €33,500 per person in Belgium, to €29,000 in France, €25,550 in Germany, to a low of €18,000 in Britain.29 Encouraging bank lending to SMEs would clearly boost jobs as well as tax revenues, while helping to stabilise the social situation in the EU. In the United States, unemployment benefits still constitute a heavy burden on state and federal government budgets, despite a sharp reduction in unemployed workers in 2014-15. Insurance programs paid by state and federal agencies have cost roughly $520 billion in 2014, according to a Congressional Budget Office report.30 At the same time, those agencies cannot collect the same levels of income tax as before — forcing the government to borrow money or cut back on other spending, hence exacerbating deflationary pressures.

4) A fourth fruitful sector is for governments to target entry-level jobs for company lending for new immigrants who have been granted asylum. Such a policy could be linked to a scale of exceptions to the minimum wage standard and would clearly have to embrace indigenous candidates with long-term unemployment histories as well in order to dampen animosities and resentment. Corporate sponsored training systems linked directly to this policy objective could generate additional employment. The digital IT revolution complicates man-machine collaboration at higher levels of education, which will require significant funding as well if secular economic stagnation is to be overcome.31 The funding for such training should be targeted for specific job sectors, processes and products where the region has a comparative advantage given long-term investment.

About the Author

Michel-Henry Bouchet is currently Distinguished Global Finance Professor at SKEMA Business School and Chief Strategist of North Sea-Global Equity Management. He specialises in country risk assessment and global financial issues. www.developingfinance.org

Michel-Henry Bouchet is currently Distinguished Global Finance Professor at SKEMA Business School and Chief Strategist of North Sea-Global Equity Management. He specialises in country risk assessment and global financial issues. www.developingfinance.org

Robert Isaak is currently a Visiting Professor of Entrepreneurship at the Institute for SMEs and Entrepreneurship of the University of Mannheim and Professor Emeritus teaching Public Policy at Pace University, New York. He specialises in global political economy and cross-cultural management and particularly issues related to social and ecopreneurship.

Robert Isaak is currently a Visiting Professor of Entrepreneurship at the Institute for SMEs and Entrepreneurship of the University of Mannheim and Professor Emeritus teaching Public Policy at Pace University, New York. He specialises in global political economy and cross-cultural management and particularly issues related to social and ecopreneurship.

References

1. Wehinger, G. “SMEs and the credit crunch: Current financing difficulties, policy measures and a review of literature”. OECD Journal: Financial Market Trend, Vol 2013/2

2. Source : Federal Reserve Bank of St Louis, Economic Research 2015

3. https://www.iif.com/topics/shadow-banking-0

4. See European Commission, Annual Report on European SMEs: A Recovery on the Horizon? Final Report, Oct. 2013.

5. ECB Monthly Bulletin, July 2014, page 79.

6. Eurostat and ECB

7. PwC, Increasing European SME Access to Credit with Non-bank Lenders, April 2014.

8. Source: Banque de France, Bulletin n°192, Q2 2013.

9. FBF, October 20, 2015: http://www.fbf.fr/fr/espace-presse/fiches-reperes/financement-des-tpe-pme

10. Credit Agricole, Etudes Economiques, December 2015.

11. SAFE enquiry, ECB 2015

12. Source: BIS Quarterly series.

13. When Credit Dries Up: Job Losses in the Great Recession, Bentolila, Jensen, Jimenez and Ruano, July 2014, http://www.uam.es/personal_pdi/economicas/mjansen/CreditJobsREStud.pdf

14. PwC, July 2014 report on SMEs access to bank credit.

15. Angus Armstrong et al, ‘Evaluating Changes in Bank Lending of UK SMES’, London: National Institute of Economic and Social Research, Department for Business Innovation & Skills (April 2013)

16. FDIC https://www.fdic.gov/consumers/banking/businesslending/solutions.html. (In the US, the Small Business Administration (SBA) defines small businesses as firms with fewer than 500 employees)

17. Source : FDIC https://www2.fdic.gov/qbp/

18. What Happened to America’s Small Businesses during the Financial Crisis? McCarthy, B. Fundera Ledger, September 16, 2014.

19. Elisaveta Ushilova and Manfred Schmiemann, Access to finance statistics. Eurostat: Structural business statistics unit, data from September 2011, pp.1-2.

20. Ibid.

21. Martin Brown et al, How do Banks Screen Innovative Firms? Evidence from Start-up Panel Data, Discussion Paper No. 12-032. Mannheim: ZEW Centre from European Economic Research, May 2012.

22. OECD Science, Technology and Industry Scoreboard 2011, Chapter 5: Ease of Access to Loans, Figure 5.7.1 Paris: OECD, 2011.

23. European Commission, Enterprise and Industry, 2014 Small Business Act for Europe Fact Sheets-GERMANY, Brussels, 2013.

24. Bank of England, Trends in Lending, 2012.

25. Bank of England,Trends in Lending, 2015.

26. U.K. Department for Business Innovation and Skills, in Country Profiles for SME and Entrepreneurship Financing, 2007 13: U.K.

27. OECD, Financing SMEs and Entrepreneurs, 2015, p. 357.

28. The European Commission: 2014 SBA Fact Sheet: the U.K.

29. Source: EuroActiv.com, January 2013 and European Federation for Services to Individuals (EFSI)

30. CNN-Money http://money.cnn.com/2012/11/29/news/economy/unemployment-benefits-cost/

31. See Erik Brynjolfsson and Andrew McAfee, The Second Machine Age (NY: Norton, 2014)

{kind=link}