By Geraint Harvey, Peter Turnbull and Daniel Wintersberger

There is now no doubt that the impact of the coronavirus pandemic has produced the most severe crisis to impact civil aviation. While the 9/11 terrorist attack on New York disrupted passenger flights, and the global financial crisis produced a sharp, but crucially short shock for airlines, neither of these events come close to the damage inflicted on airlines from global lockdowns in response to COVID-19.

Although airlines lost US$26.1 billion in 2008, the following year losses were just US$4.6 billion and, in 2010, the airline industry was back in the black with net profits of US$17.3 billion. In contrast, financial losses of more than US$370 billion in 2020 and an estimated US$330 billion in 2021 reflect the very different scale of the crisis.

When airlines don’t fly, they incur heavy losses. The health of the passenger airline industry is measured in revenue passenger kilometres (RPK). This represents the number of kilometres travelled by paying passengers. As data presented by the International Civil Aviation Organisation shows, passenger traffic drops sharply after a crisis, but it usually only takes a couple of years before there is a return to the pre-crisis growth path.

When it comes, what will the recovery after the pandemic look like? International Civil Aviation Organisation data reveals that there are signs of recovery in international traffic, but this is stuttering rather than smooth. Domestic air transport, which is very different from international air transport because it is subject to only one set of rules and one regulator, offers an indication of how the market will look when restrictions are lifted.

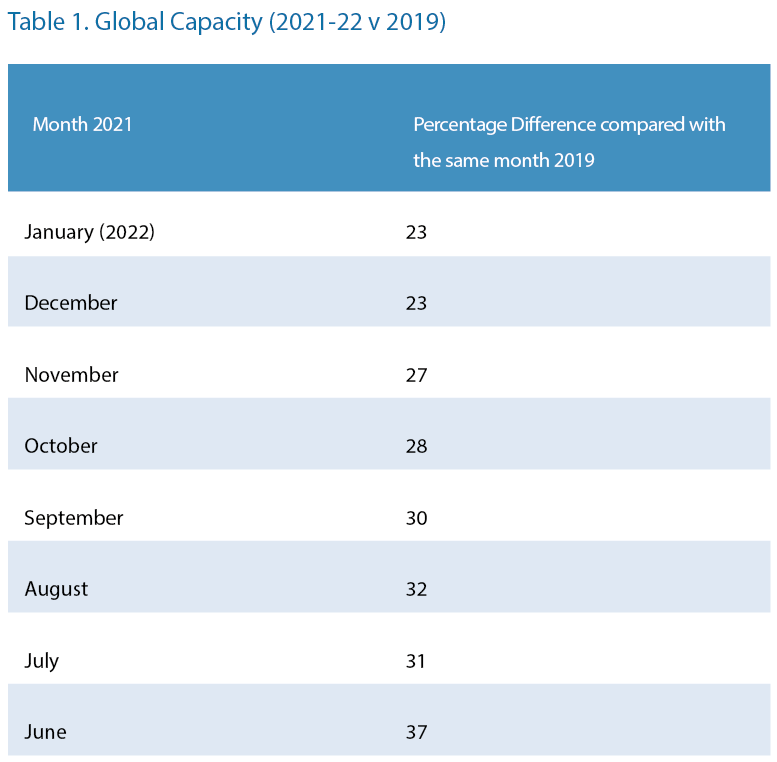

Official Aviation Guide (OAG) data on airline capacity (a measure of the seat availability on airlines worldwide and an indication of the health and scale of the industry) reveals that the deficit since the start of the pandemic has continually shrunk. Capacity was 31 per cent lower in July 2021 than it was in July 2019, and only 23 percent lower in January 2022 than it was at the same time in 2019.

In terms of specific markets, US domestic capacity reached 90 per cent of the 2019 levels in December 2021, while international capacity increased throughout the year, so that it was some 25 per cent lower in December 2021 than at the same time in 2019.

Indeed, data on domestic passenger traffic in 2021 was higher in July-August 2021 than it was pre-pandemic (the same period in 2019) on routes in South Korea (Jeju-Gimpo, +4 per cent) and Mexico (Cancun-Mexico City, +7 per cent). These aren’t aberrations with small numbers of passengers (>1.5million and >700,000, respectively, travelling these routes in July-August 2021).

What is true of all crises in civil aviation history is that while cost reduction strategies invariably focus on labour, recovery is fundamentally contingent upon labour – with airlines requiring sufficient skills to meet increasing demand. We argued in 2020 that culling jobs in response to the pandemic would prove problematic for many airlines because these airlines would consequently struggle to deal with the demand as the world emerges from the pandemic. The depth of the crisis along with its duration meant that many airlines have lost a significant number of employees.

In 2022, several airlines struggled to cope with the increase in passenger numbers. In the US, government aid of $60 billion to the airline industry and a further $15 billion for “payroll support” did not prevent widespread furlough of staff. United Airlines and American Airlines furloughed around 32,000 workers in total. American Airlines and United Airlines have been forced to cancel flights due to staffing shortages, while United Airlines has offered its pilots triple pay in order to take on extra trips in January 2022. Across the Atlantic, British Airways announced plans to make up to 12,000 staff redundant and reduce the terms and conditions of 30,000. This policy has resulted in the need for airline management to contact staff laid off in 2020 to offer remuneration double what it was in 2019 in order to have sufficient staff to meet the anticipated summer 2022 boom.

Low-cost airlines are expected to be well-placed to take advantage of more immediate pent-up demand, especially in the VFR (visiting friends and relatives) and tourism markets, due to their ability to rapidly (re-)hire aircrew.

For example, Ryanair, Europe’s largest low-cost airline, hires cabin crew via agencies on short-term contracts and pilots who are ‘”self-employed’”. In the week of 30 November to 6 December 2021, Ryanair flights were up 5 per cent on the same week in 2019, whereas other low-cost airlines were still operating fewer flights (e.g., easyJet down 43 per cent and WizzAir down 28 per cent). The network or ‘”legacy’” airlines were still down more than 20 per cent (e.g., KLM and Air France), more than 30 per cent (e.g., Lufthansa and SAS), or more than 40 per cent (e.g., BA).

The post-pandemic recovery in passenger demand occurs amidst one of the tightest labour markets advanced industrial economies have experienced in recent history. While the unemployment rate in the US has returned to its pre-pandemic low of 3.9 per cent, a significant proportion of the workforce has recently left the labour market, and Americans continue to quit their jobs ‘”at record pace’”. This trend is not confined to the US, with similar patterns emerging in virtually all major (ageing) advanced industrial economies. Not only are airlines likely to find it difficult to take on new staff under the current circumstances, but they are also likely to incur heavy costs associated with the training of new recruits.

It should also be noted that the implicit knowledge lost in the course of redundancies is difficult to replicate. It is likely that, with seasoned members of cabin crew leaving, rich experience and know-how (for example in dealing with irate passengers) also leaves the airlines. Cabin crew are safety professionals, first aiders as well as ‘skilled emotion managers’ and, as such, add significant value to the airline.

A final point concerns the incalculable damage to employee relations as a consequence of staff lay-offs introduced in response to the crisis. British Airways has recently offered a 10 per cent bonus to operational staff in an attempt to rebuild relationships damaged by decisions taken in 2020. Although this gesture will doubtless be welcomed by many workers at the airline, no offer of a financial bonus can reset employee relations.

The sting in the tail of the pandemic is that survival strategies based on labour cost minimisation create the very conditions that will hamper recovery and prolong its impact on airlines.

About the Authors

Geraint Harvey is DANCAP Private Equity Chair and Professor of Human Organization at Western University, Ontario. Harvey’s research has focused on the changing nature of work. Harvey has been commissioned to undertake research by a variety of international organizations and his findings have been published in a range of media.

Peter Turnbull is Professor of Management & Industrial Relations at the University of Bristol, UK. He has written numerous reports on the civil aviation industry for the International Labour Organization (ILO), global union federations and the European Commission. He is currently researching the global impact of COVID-19 on air traffic management.

Daniel Wintersberger is a lecturer in HRM and employment relations at University of Birmingham, Business School, UK. His research has been funded by the International Transport Workers’ Federation and his research findings have been published in a range of media.

References

- How the Airline Industry Survived SARS, 9/11, the Global Recession and More, June 9, 2020, https://apex.aero/articles/aftershocks-coronavirus-impact/ British Airways hunts for 2,000 cabin crew ahead of summer boom (msn.com)huawei-looks-cloud-services-2021-us-sanctions)

- https://www.iata.org/en/pressroom/pr/2008-09-03-01/

- Net profit of commercial airlines worldwide from 2006 to 2022, October 5, 2021, https://www.statista.com/statistics/232513/net-profit-of-commercial-airlines-worldwide/

- Economic Impacts of COVID-19 on Civil Aviation, https://www.icao.int/sustainability/Pages/Economic-Impacts-of-COVID-19.aspx

- The impact of the financial crisis on labour in the civil aviation industry, January 1, 2009, https://www.ilo.org/sector/activities/topics/crisis-recovery/WCMS_161566/lang–en/index.htm

- World Aviation and the World Economy, https://www.icao.int/sustainability/Pages/Facts-Figures_WorldEconomyData.aspx

- Effects of Novel Coronavirus (COVID‐19) on Civil Aviation: Economic Impact Analysis, March 8, 2022, https://www.icao.int/sustainability/Documents/

- COVID-19/ICAO_Coronavirus_Econ_Impact.pdf

- OAG Frequency & Capacity Statistics, July 2021, https://www.oag.com/hubfs/free-reports/Frequency_and_Capacity_Reports/OAG-Frequency-and-Capacity-Statistics-July-21.pdf?hsLang=en-gb

- OAG Frequency & Capacity Statistics, January 2022, https://www.oag.com/hubfs/free-reports/Frequency_and_Capacity_Reports/OAG-Frequency-and-Capacity-Statistics-January-22.pdf?hsLang=en-gb

- https://www.oag.com/monthly-airline-frequency-and-capacity-trend-statistics

- US Market Recovery Edging Closer, December 23, 2021, https://www.oag.com/blog/us-market-recovery-edging-closer

- Passenger Bookings & Load Factors: Every Summer has a Story, December 21, 2021, https://www.oag.com/blog/passenger-bookings-load-factors-every-summer-has-a-story

- Coronavirus is hurting airlines but they shouldn’t rush to cut jobs, July 21, 2020, https://theconversation.com/coronavirus-is-hurting-airlines-but-they-shouldnt-rush-to-cut-jobs-142943

- American Airlines cancellations pile up as omicron fetters holiday travel, December 27, 2021, https://www.dallasnews.com/business/airlines/2021/12/27/american-airlines-cancellations-pile-up-as-omicron-fetters-holiday-travel/

- United Airlines (UAL) Offers Staff Higher Pay Through January, January 3, 2022, https://ca.news.yahoo.com/united-airlines-ual-offers-staff-154503182.html

- British Airways plans to make up to 12,000 staff redundant, April 28, 2020, https://www.theguardian.com/business/2020/apr/28/british-airways-plans-to-make-up-to-12000-staff-redundant

- British Airways hunts for 2,000 cabin crew ahead of summer boom, January 1, 2022, https://www.msn.com/en-gb/travel/news/british-airways-hunts-for-2000-cabin-crew-ahead-of-summer-boom/ar-AAThJFx?ocid=BingNewsSearch

- Trolley Dolly or Skilled Emotion Manager? Moving on from Hochschild’s Managed Heart, June 1, 2003, https://journals.sagepub.com/doi/abs/10.1177/0950017003017002004?journalCode=wesa

- BA offers one-off bonus to pilots and crew to rebuild relations with staff, February 15, 2022, https://www.ft.com/content/7df6d516-bfb4-4f7c-b4d3-8acfcce29aeb

{kind=link}