There is compelling evidence that the severity of COVID has had significant impact on equity performance in the Emerging Markets. But other factors have also influenced equity markets, in particular, relative monetary ease and the severity of shut downs pursued in different regions. There is reason for optimism for Emerging Market relative performance in the year ahead.

The COVID-19 pandemic has wreaked havoc this past year on economic activity across the globe and, as a consequence, financial market volatility has been thrown into turmoil over the past two. The impact of COVID while widespread has varied both because the spread of the virus varied and, perhaps more importantly, government response to the emergence of the virus also varied. Some countries were quick to adopt draconian lockdowns to deter the spread of the virus. Other countries were slower to control public behaviour either due to a differing philosophy on COVID response or the lack of infrastructure to enforce a lockdown. This paper assesses whether the variations of US and emerging market (EM) equity performance in the era of COVID can be explained by the path of disease and/or government policy measures.

For the purpose of this paper, the Exchange Traded Fund (ETF) of the Morgan Stanley Emerging Market Equity Index (EEM) will be used as a proxy for Emerging Market (EM) stock market performance. Table 1 to the right shows the regional breakdown of the exposure of the stocks in the EEM. Only the top ten markets were considered for comparison with the US Market so for the purpose of indexing EM events, the weight of “other” was reallocated to the top ten marketss as is shown in the Table. For consistency, an ETF of the S&P 500 index (SPY) is used as an indicator of performance of the US stock market.

Chart 1 clearly suggests COVID was a dominant factor for overall equity market performance since its onset in March of last year. The vertical access shows the local stock market performance using standard benchmarks for each market converted into US dollars from the end of March 2020 to the middle of December in 2021 for the United States and the 10 markets in the table in the EEM index. (Note that the chart is not significantly different if the returns are not adjusted for exchange rates.) The horizontal axis shows the cumulative number of COVID cases during this period per million population for each of these markets. It is clear there is a downward slope to the scatter diagram suggesting that a higher incidence of COVID has translated into weaker market performance.

While Chart 1 shows compelling evidence of a strong link between COVID and market performance, it does not indicate whether this relationship has consistently held over the course of the pandemic nor to what degree this might have been influenced by government policy. In addition the US market is a modest anomaly as it is stronger than the relationship would indicate given that the US has the highest incidence of COVID for the markets shown.

Chart 2 compares the inter-temporal relative performance of stock markets with the incidence of COVID. The orange line in the chart shows the relative performance of EEM and SPY from the end of March 2020 when the threat of the COVID pandemic became generally apparent, and the relationship over time is clearly not stable. There are two phases; the orange line declines in the early months of the pandemic indicating underperformance of SPY vs EEM but the trend inverted and the SPY has outperformed since early this year. The blue line in the chart compares the cumulative EM case load weighted by the adjusted share in the EEM index vs the cumulative case load in the United States. Based on the relationship established in Chart 1, a relatively high EM case load – i.e. a rising blue line – should be reflected in underperforming EM markets – i.e. rising orange line. This relationship does hold from October of last year into the summer of this year. However, the EM markets outperformed early last year despite a much higher gain in case load and has underperformed in recent months despite a growth in case load that is slower than the United States.

Differing responses for markets to the pace of COVID case accumulation could be explained by differing policy responses both in terms of direct restrictions on economic activity – e.g., requirements on isolation – or general support of the economy via monetary stimulus. According to the website Our World in Data (https://ourworldindata.org), the economic policy “stringency” index for the United States rose 67 points from the start of 2020 to mid-March 2020 as initial attempts to slow the spread of COVID were implemented. By contrast, the weighted stringency index for the EEM regions was up only 48 points. The more proactive US response is reflected in Chart 3 on the following page in the more severe dip in US GDP growth. The underperformance of the SPY hence may be reflective of this poor economic performance overwhelming the more modest gain in infections. Another factor that may have helped EEM performance is the perception in the early months of the pandemic that COVID mortality rates were lower than in the industrial world (see: https://www.lgimblog.com/).

While relative policy stringency provides an explanation of the underperformance of the US market in the early stages of the pandemic it does not help explain the more recent outperformance of the US market. Stringency has broadly declined across all regions over the course of the pandemic reflecting both progress in distributing vaccinations and better understanding of the transmission process. But the weighted stringency of the EEM area has declined 39 points since May of last year while the US policy remains relatively stringent with only a 19 point decline. Moreover, US GDP growth has lagged weighted EM growth for much of this period but more recently they are roughly aligned.

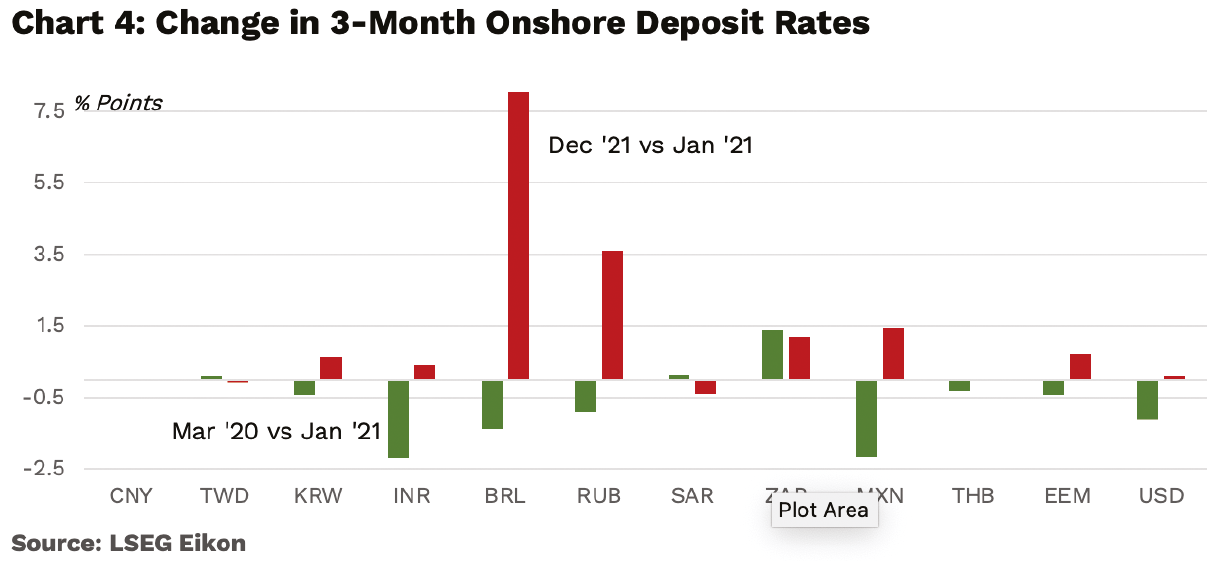

Chart 4 compares central bank policy – as reflected in changes in 3-month local deposit rates – for the United States and each market included in EEM as well as the weighted average interest rate change. The blue bars shows the change in rates during the first phase into the beginning of this year when EM markets were outperforming. The orange bars show how rates have changed since then. During the first phase, US rates actually dropped more than the weighted EM average – though some individual EM markets saw substantial rate cuts – so relative monetary policy does not seem to be a factor behind US market underperformance during phase I.

One well reported by-product of the disruption of COVID has been surging inflation across almost all world markets. The United States, in particular, saw CPI inflation hit a near 30-year high 6.8% last month. The US Federal Reserve Bank until recently has blamed most of the inflation surge on supply disruptions due to COVID that would self-correct so they felt there was little need for tighter monetary policy. Although recent comments from Fed Chairman Powell indicate growing recognition that inflationary pressures may not be purely transitional, the Fed has yet to take any specific actions to tighten policy. Plans for cutting back on bond purchases and higher policy rates while now part of the discussion there is still no intent to take action until sometime in the next year and only if US inflation does not show signs of abating.

EM central banks have not been able to share the Fed’s patience on reacting to inflationary pressures. In general, a more recent history of inflation problems in many EM markets leaves them with less institutional credibility than the Fed. Also, many EM market currencies are vulnerable to investor sentiment forcing interest rate hikes as a way to head off weakening exchange rates. The consequence is that while the Fed’s policy rate – Fed Funds – has remained flat and the 3-month deposit rate is only marginally higher, the weighted average EM 3M deposit rate is up almost a full percentage point and several markets – especially, Brazil and Russia – have seen hikes that are far bigger than the average. Relatively tighter monetary policy in EM markets is likely the primary source of SPY outperformance in recent months.

Will EM markets outperform in 2022?

Uncertainties on how the spread of the omicron variant and potential for yet more COVID mutations makes it difficult to assess market prospects for the year ahead with great confidence. That said, it looks probable that EEM stocks have potential to outperform the SPY. Based on the Our World Data site cited above, the implementation of vaccines in the markets included in the EEM while highly varied, on average, are roughly equivalent to the United States. Recent research from Oxford (see: https://www.reuters.com/business/healthcare-pharmaceuticals/astrazeneca-shot-third-dose-works-against-omicron-study-2021-12-23/) suggests that the AstraZeneca vaccine which has been more widely used in the EEM region is effective against omicron (although its effectiveness, as with Pfizer and Moderna, is contingent on a booster). Thus it seems the projected case load in the US and EM markets should not vary substantially. This leaves the biggest potential factor the potential for the Fed to play catch up on rate hikes in 2022 which could significantly weigh on US equities.

About the Author

Dr. Ronald Leven joined the economics faculty at Duke University in 2018, a capstone to his 35-year career serving as a strategist at top tier banks like JP Morgan and Morgan Stanley. He has also worked as an Economist at several major corporations and managed his own hedge fund. Dr Leven started his career researching Emerging Market default risk at the Federal Reserve Bank of New York.

References

- https://ourworldindata.org

- see: https://www.lgimblog.com/

- see: https://www.reuters.com/business/healthcare – pharmaceuticals / astrazeneca – shot – third-dose-works-against – omicron – study-2021-12-23/)

{kind=link}