")

China is emerging as a trade and economic powerhouse, overtaking the West and drawing support from Southeast Asia. Dr Kalim Siddiqui discusses how China´s expanding trade relations with the region gained them an advantage, making them a force to reckon with in the global economy.

Introduction

As we closely examine the extraordinary economic expansion of the East Asian countries in the past decades, we find an interesting development. The region is emerging as a kind of economic powerhouse at a time when the Western economies are facing uncertainty and deepening crisis and little prospect of returning to the ‘‘good old days’’. In the last few decades, a huge transformation has taken place in the region. In the early 1950s, there was the Korean War, and soon after the Vietnam War. Korea was divided into two antagonistic blocs and the US position was solidified through bilateral defence treaties (with Japan, South Korea, Taiwan, and the Philippines). As Cumings notes: “All became semi-sovereign states, deeply penetrated by American military structures and incapable of independent foreign policy or defense initiatives.” (Cumings, 1994: 23)

During the Cold War, there was huge tension in East Asia between the US and Soviet Union and the US’s primary aim was to fight communism. Even nationalists were seen as a threat to its global strategic hegemony, which was the reason the US built several military bases and signed defence treaties with most of the East Asian countries. The US supported establishing the ‘‘rule of law’’ and institutions and economic reforms so that the region’s economies could be integrated with the West and more capital flow and investments was thought to keep the Soviet Union out of the region. Therefore, the international situation helped these countries to bargain and develop their domestic industries and in the early industrialisation phase, these countries were allowed to use the state to protect domestic industries and the US also supported land reforms to resolve rural inequalities (Siddiqui, 2021b). Furthermore, imports of technology and access to the Western market for their finished goods gave them the necessary impetus for industrialisation and steady growth (Siddiqui, 1995).

The simultaneous rise of China and India’s share in the global economy is remarkable (Siddiqui, 2017; also 2015). This led many researchers to acknowledge it. Here, I will analyse China’s trade and economic expanding relation with the ASEAN (Association of Southeast Asian Nations) countries and the changing trade pattern between China and East Asian countries, especially Southeast Asia as well as the important factors behind this shift and changing economic relations among East Asian countries which was unseen earlier. Southeast Asian region is important both in terms of the high concentration of population and because rapidly growing economic relations between them and China would have global economic consequences in coming years (Siddiqui, 2023a).

The international trade data indicates that the centre of gravity of power is indeed shifting from ‘West’ to ‘East’. The West’s hold over the global economy is weakening and the East is moving up and returning to its dominant position in the global economy, which it occupied for centuries in the past except for the last two hundred fifty years, when Europe and Japan occupied most of Asia and plundered its economy (Siddiqui, 2015).

In recent decades, the economic relations and trade patterns are changing rapidly due to many factors, and China is steadily emerging as an important economy (Siddiqui, 2021a). As the ASEAN economy is expanding, the region sees China as a new giant emerging which could be useful in terms of diversifying their economies and lessening their reliance on the West. There are three key reasons for the sudden changes in this region’s strategy in recent years. Firstly, the 1997 East Asian financial crisis and later the 2008 global financial crisis had a very severe impact on the East Asian economies. Secondly, China’s sharp rise in growth rates and rising income levels and trade provided new opportunities for ASEAN countries to take advantage of China’s expanding markets. Thirdly, the deepening crisis in the Western economies and near stagnation in the Japanese economy with little prospect of leading the region’s economy as was the case in the 1960s and 1970s, making the whole dynamism of the Western developmental module lose credibility due to repeated crisis (Siddiqui, 2024). Moreover, China’s ‘‘Belt and Road’’ initiative is bringing the region closer and more expected to increase further trade and economic relations (Siddiqui, 2019).

ASEAN Economies and China

The ASEAN countries consist of eleven member countries, which have impressive diversity in religion, culture and history (Siddiqui, 2012). These countries include Brunei, Myanmar, Cambodia, Timor-Leste, Indonesia, Laos, Malaysia, the Philippines, Singapore, Thailand and Vietnam. Together, they represent a market with a GDP of more than $2.9 trillion and a population of 647 million people.

The ASEAN economies are a geopolitical and economic organisation established in 1967 by five member states, but at present, the organisation consists of 11 countries. The ASEAN countries’ objectives have been to promote regional cooperation, advance economic, social and cultural development through regional initiatives and create peace and stability. The ASEAN economies have grown considerably since their inception in 1967 and doubled its share of the world’s GDP from 3.3 percent in 1967 to 6.2 percent in 2017. Moreover, by 2017, the ASEAN economies as a group have a total young population of 600 million, and alongside a high savings rate, the region’s future appears promising. However, the growth of the ASEAN economies was mainly driven by capital inputs, which is not sustainable in the long run, as the effects of capital investments as it is expected that it will diminish over time. Additionally, the ASEAN economies depended on external trade, as growth was primarily driven by technological progress and transfer through trade openness and foreign direct investment in the region.

I will briefly discuss East Asian economies as Northeast Asian countries such as Japan had played an important role in the transformation of the region’s economy, especially since the Plaza Accord was signed in 1985, and the value of the Japanese Yen was appreciated. As a result, Japanese exports became expensive, while at the same time imports became cheaper and also Japanese corporations found it more profitable to invest abroad to increase profits and take advantage of expanding markets in ASEAN countries.

Moreover, the rapid growth of most East Asia countries over the past fifty years has surprised policymakers and economists and this has encouraged many academics to study the main factors behind this upsurge in the growth and economic transformation of the region. The successful economies of the region are South Korea, Hong Kong, and Taiwan, which have experienced a dramatic change in the living conditions of their inhabitants. Since the early 1970s, the East Asian region, which is among the most populous regions of the world, has achieved enormous success in establishing peace, stability, and prosperity. This has not occurred at the same pace all over the region. Among East Asia, the North-West performed better than the Southeast (the Philippines, Cambodia, Laos, Indonesia, Thailand, and Vietnam). The worst performer was the Philippines, which grew at about 2 percent a year in per capita terms, while Malaysia and Thailand did better, achieving growth rates of 3 to 5 percent.

However, their rapid transformation is still modest compared with the phenomenal growth of South Korea, Hong Kong, Singapore, and Taiwan (Siddiqui, 2016). These four top-performing countries have had annual growth rates of output per person well above 6 percent. These growth rates were sustained over fifty years, apart from a brief interruption in the rise in their output, except during the brief period when the region was hit by the East Asian financial crisis in 1997-99.

The neoclassical growth model suggests that in achieving sustained growth, technology and technological progress is the only possible way, over the long run, for an economy to achieve a higher growth of output per person. This will lead to an increased labour participation rate initially, but it can be forever (Siddiqui, 2018). Therefore, to achieve long-term growth, an economy must continuously improve its technology. The Solow model (1956) conducted a growth accounting exercise on this presumption. He said that the accumulation of capital and an increase in the labour participation rate had a relatively minor effect, while technological progress accounts for most of the growth in output per person (Siddiqui, 2021c). Hence, the widely accepted view about the better performance of East Asian economies is due to the availability of technology in their high growth rates and the plan to catch up with the West.

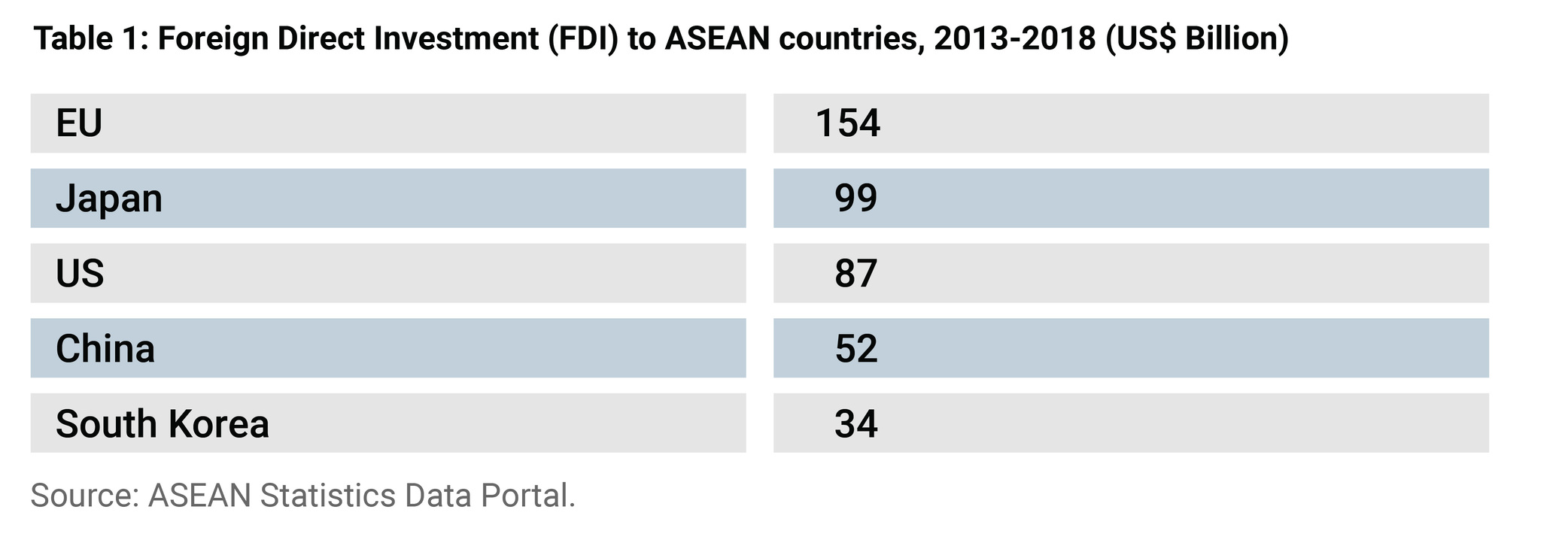

Moreover, the East Asian business culture and informal business networks with ramifications for the international economy played an important role. The strong ‘‘forward’’ and ‘‘backward’’ linkages connect the East Asian economies to the rest world. This means the expansion of the East Asian economy which began more than four decades ago with full US support and economic cooperation. As shown in Table 1 after EU, Japan and the US, China has emerged as the fourth largest capital investors in the ASEAN countries.

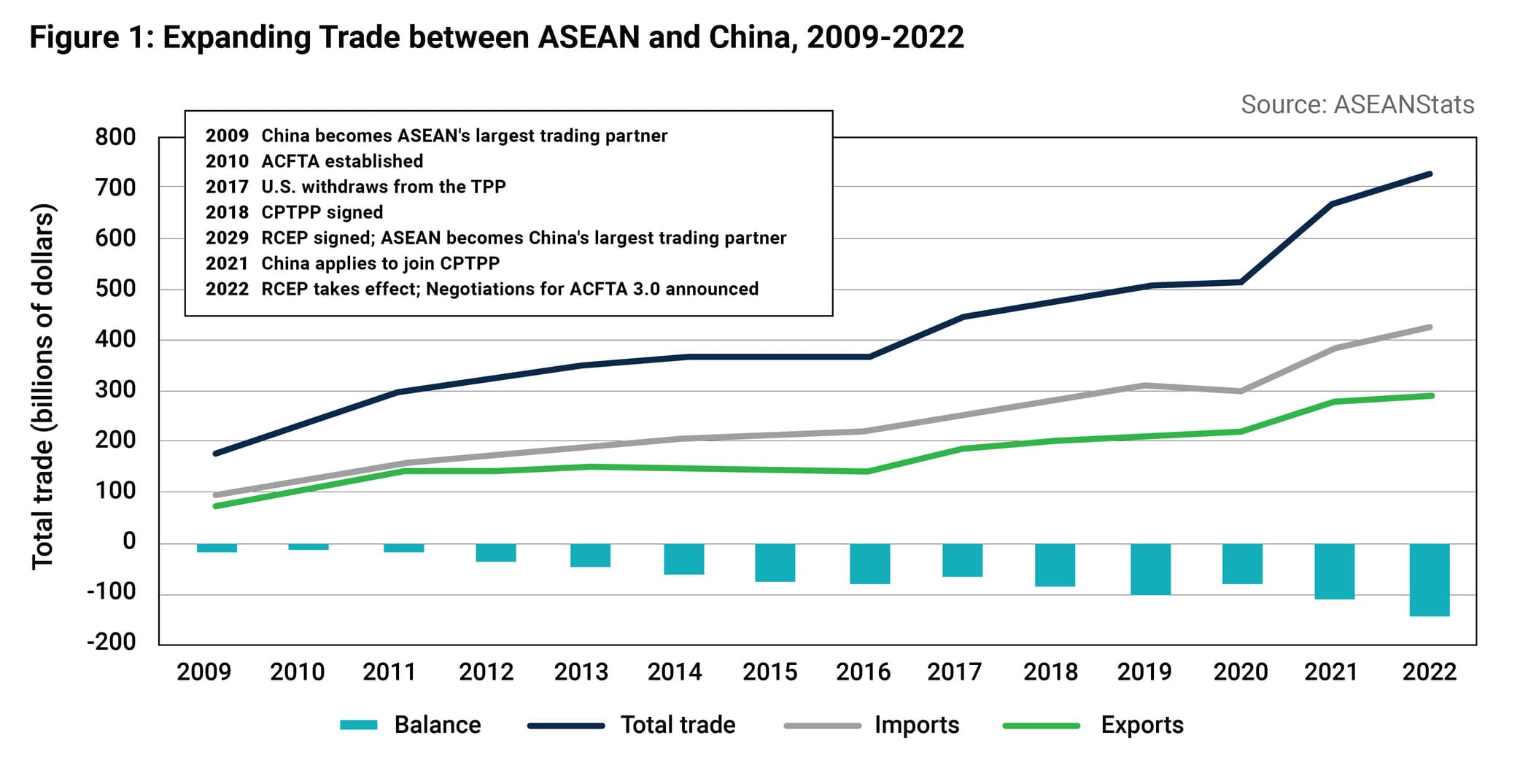

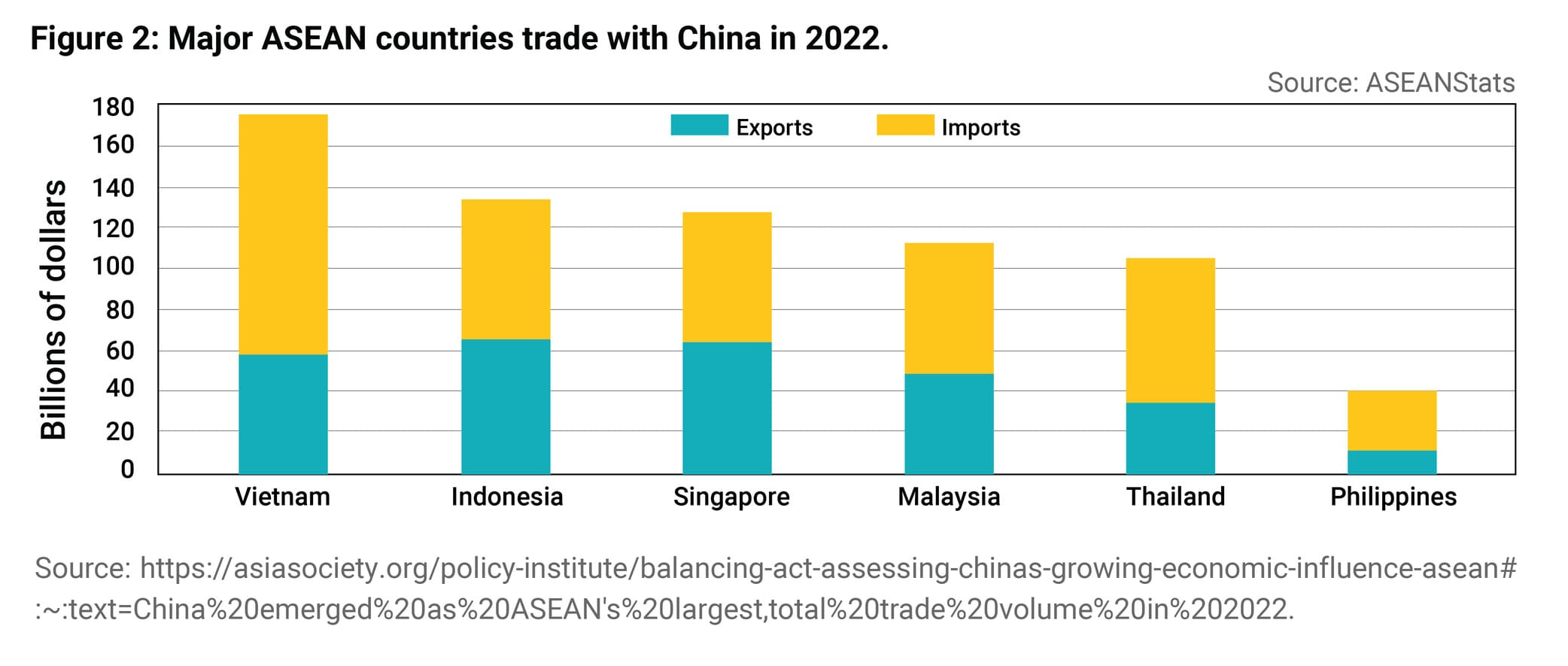

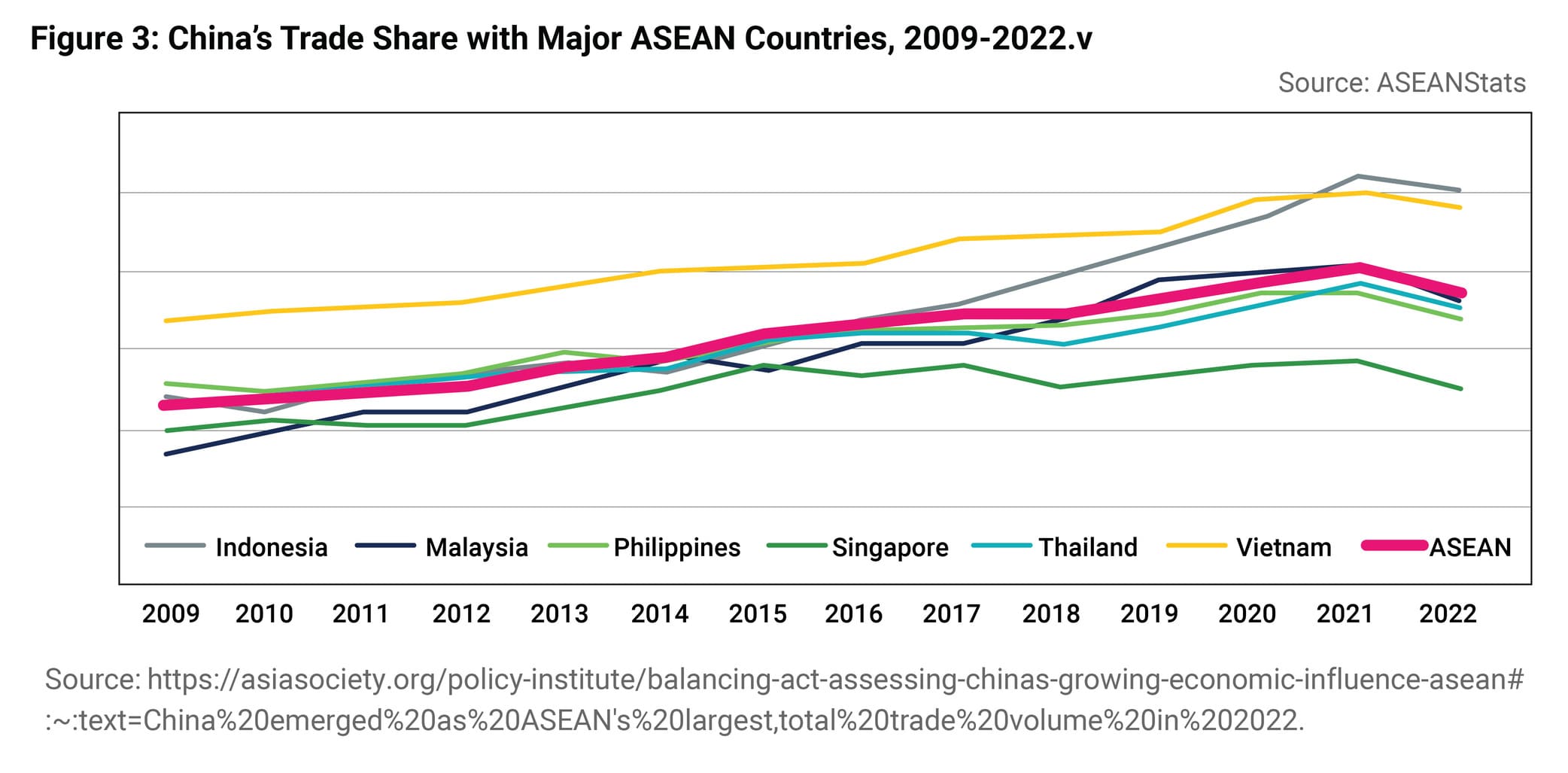

China emerged as ASEAN’s largest trading partner in 2009, and trade between the two economies more than quadrupled by 2022 (See Figure 1). China’s trade with ASEAN countries has also seen a corresponding rise. ASEAN became its largest trading partner in 2020, accounting for 11.4% of China’s total trade volume in 2022 (as shown in Figure 2 and Figure 3).

As the largest economy in Asia, China’s economic performance has a significant impact on the economies of its neighbours. With the emergence of new and enhanced regional trade agreements and deepening ties of trade and investment, ASEAN’s economies are linked more than ever to China’s. According to the Asian Development Bank, in 2000 a 1% increase in China’s economic output led to a 1.7% rise in ASEAN’s output. The 1% increase in Chinese output led to a 4.9% increase in ASEAN output in 2010 and a 6.3% increase in 2020. ASEAN countries enjoy significant benefits when China’s economy grows, but if it slows down, then they will also face greater vulnerabilities.

ASEAN’s imports from China have led to a sizeable and growing trade deficit, reaching US$140 billion in 2022 – nearly 4% of ASEAN’s overall GDP. Trade deficits arise for a variety of reasons and are not inherently a problem, but they can also be symptomatic of other concerns, including overreliance on particular sources for certain products. Vietnam and Thailand account for most of ASEAN’s deficit with China, underscoring their reliance on Chinese imports. The Philippines and Malaysia have also seen their deficits grow, reflecting a broader regional trend of mounting trade imbalances with China. Among smaller ASEAN economies, Cambodia’s situation is particularly alarming – its trade deficit with China soared to 30% of its GDP in 2022.

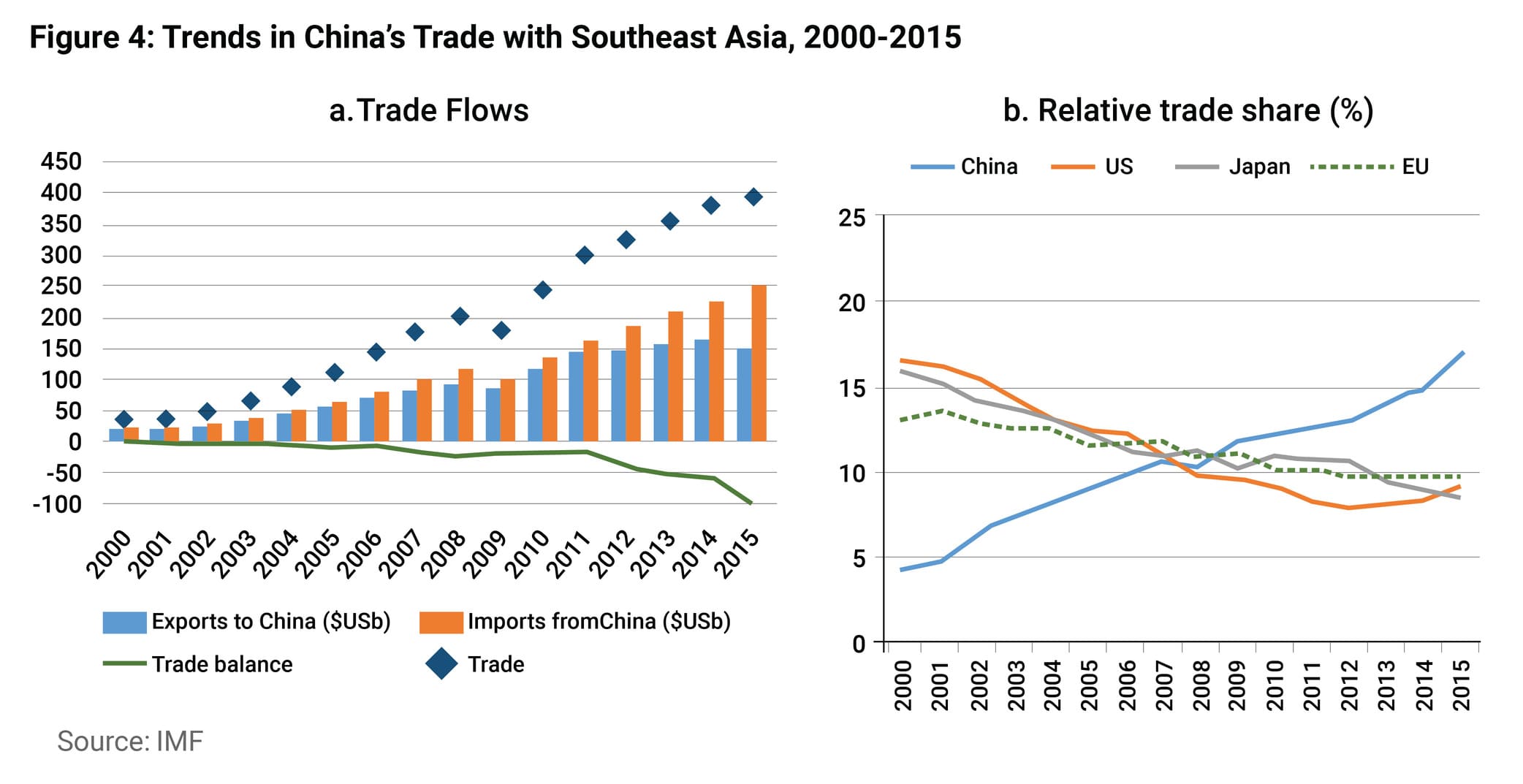

Moreover, due to the end of the Cold War, the region’s importance for the US has also changed dramatically. In the last fourteen years, the trends indicate that China’s share has risen steadily whereas the shares of SEA’s traditional partners, such as the US, EU, and Japan have been gradually declining. But also within the expansion of bilateral trade where Southeast Asia’s trade deficit with China has been rising fast since 2010 (See Figure 4). This period also coincided with the signing of the ASEAN-China Free Trade Area, which has opened increased investment in the region, especially in the electronics sector, especially in Vietnam, which increased the region’s imports of intermediate inputs and capital goods from China.

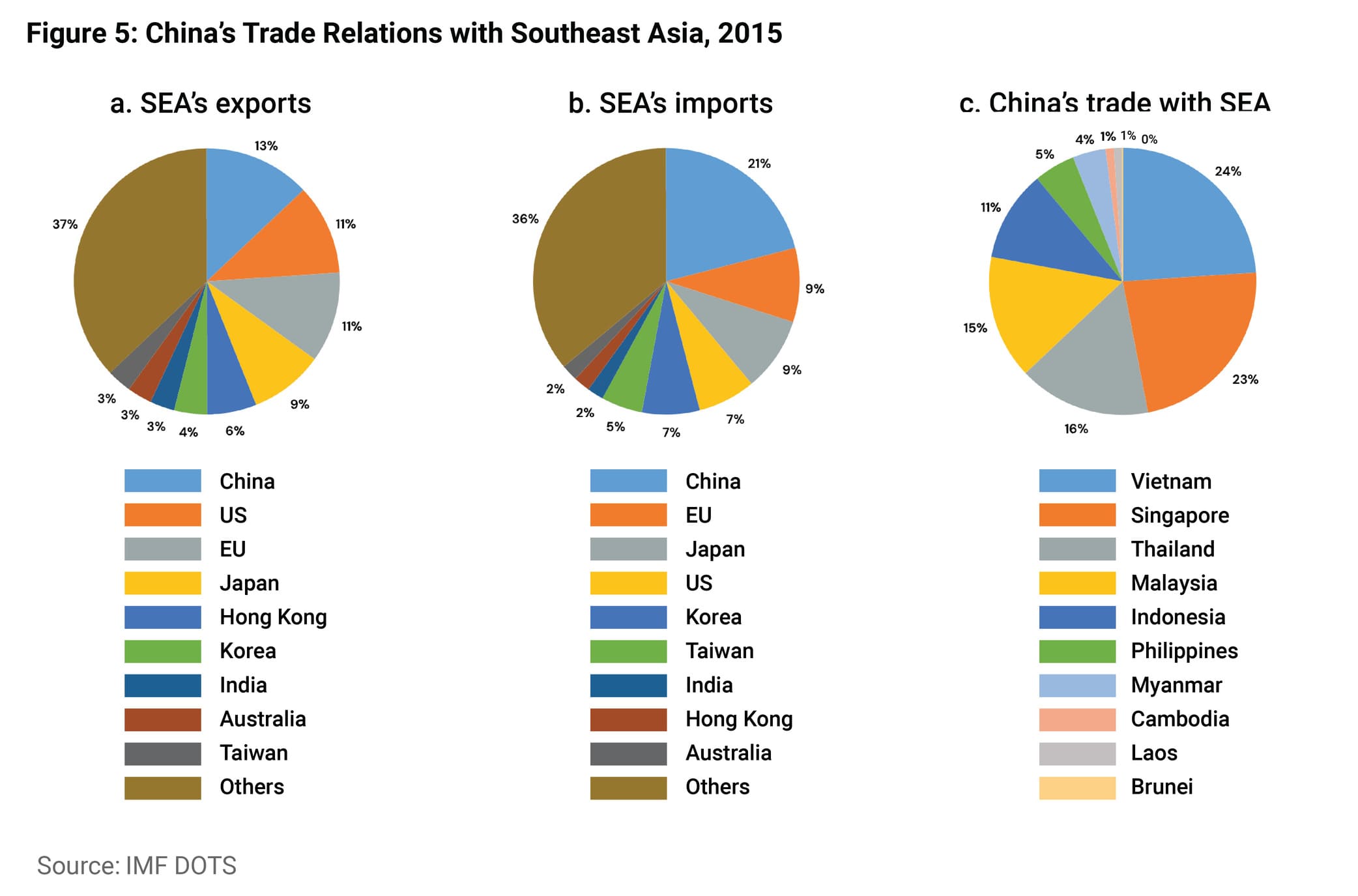

China is SEA’s top export market, its share has risen sharply in recent years. China is the overwhelmingly largest import partner for SEA, accounting for 21 percent. Imports from China not only include consumer products but also intermediate goods for the regional production network. China’s largest trade partner in SEA is Vietnam, which accounts for 24 percent of its total regional trade, as shown in Figure 5. Singapore is the second largest partner and is a regional hub for trans-shipment and re-export.

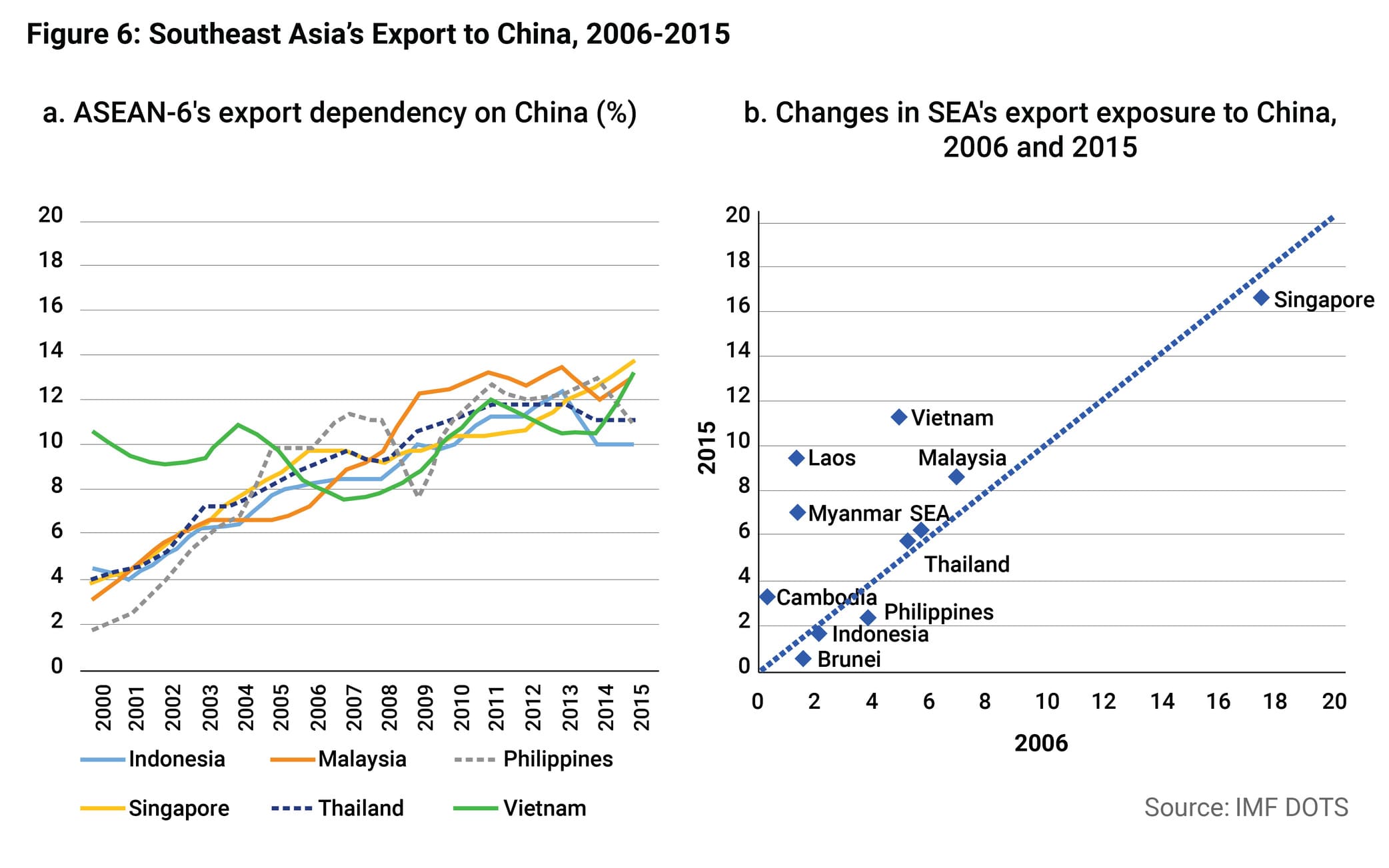

For more developed economies in the region, China’s share is concentrated between 10 and 14 percent (Figure 5). In the poor countries in the region such as Cambodia, Laos, and Myanmar, the variance is huge, ranging from 5 percent (Cambodia) to 38 percent (Myanmar). Looking at China’s share to the country’s total export can be misleading since it does not take into account the importance of exports to the country’s economy. Thus, an additional measure of export exposure can be calculated where the export dependency on a certain country is standardised by its export-to-GDP ratio. And this lowers China’s share for most countries significantly except for Singapore (see Figure 6).

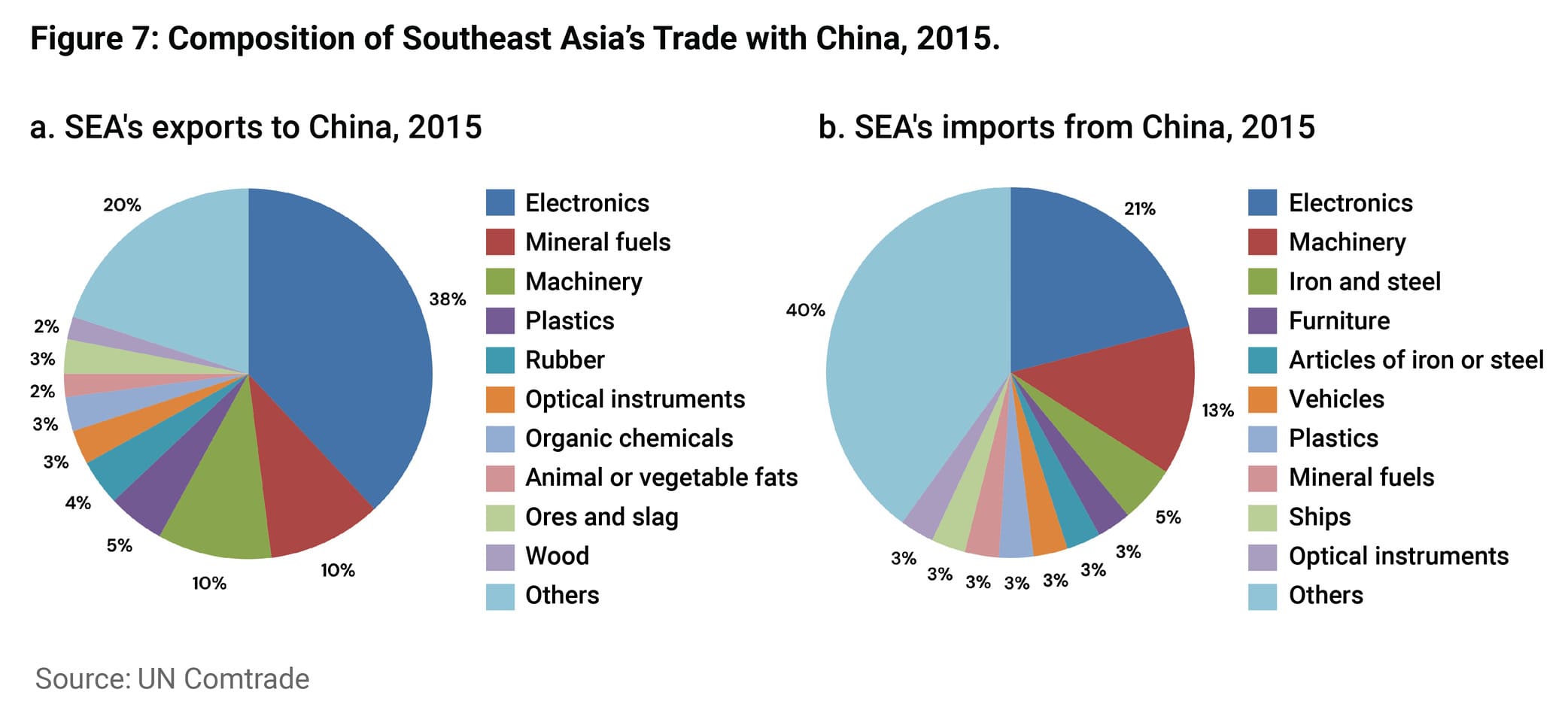

Southeast Asia has become a very important part of the global Value Chains across China and Southeast Asia. China’s trade with Southeast Asia is dominated by electronics and machinery in exports and to a lesser extent imports, suggesting high levels of intra-industry trade. Electronics and machinery, these two sectors account for 48 percent of SEA’s exports to and 34 percent of its imports from China in 2015 (See Figure 7). The high shares of these two areas are the result of an extensive regional production network established across East Asia where China is the processing hub for final destinations.

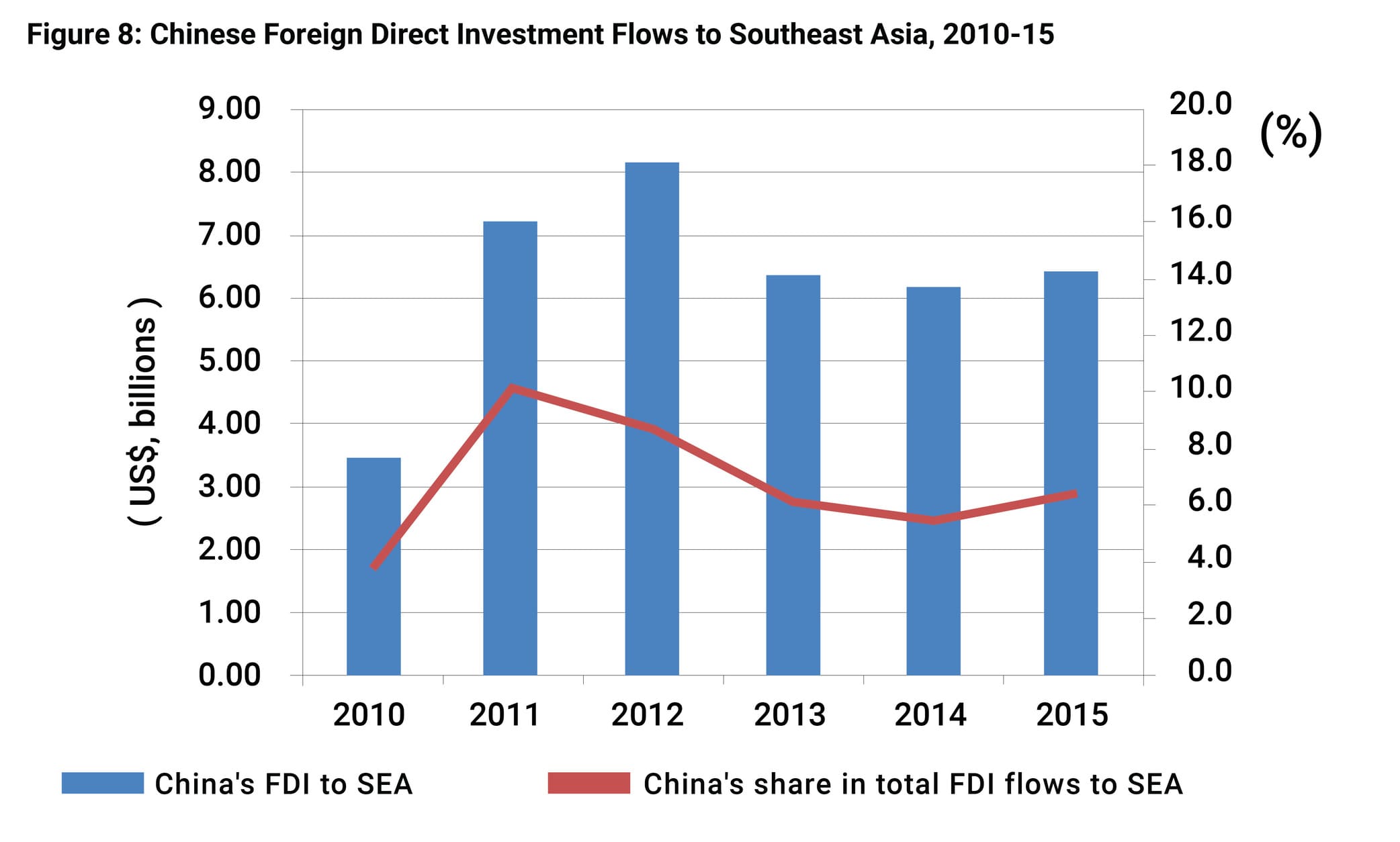

China is the fourth-largest investor in Southeast Asia, following the EU, Japan, and the US, although it only accounts for 7 percent of SEA’s inbound Foreign Direct Investment (FDI) flows from 2011-2015. The growth rate of Chinese FDI in SEA is higher than the top three investors. Its FDI in the region rose sharply after the global financial crisis. Singapore is the top destination for Chinese FDI in the region (see Figure 8). The relative importance of Chinese FDI varies significantly across countries, depending on their level of economic development.

Southeast Asia’s economies showed an overall good performance in 2023. Malaysia, the Philippines, Singapore, and Vietnam saw GDP growth increase in this period, while Indonesia and Thailand were slower. The external conditions and demand for the region’s manufactured and commodity exports are the main reasons behind the slower growth in this quarter. On the other hand, robust domestic demand, government spending, and a continued recovery of the services sector — particularly tourism, have contributed to maintaining higher levels of employment and incomes, which in turn have supported growth, particularly in Vietnam and the Philippines.

The tiny state of Singapore is the richest country in Southeast Asia, with a per-capita GDP of US$ 107,690. Singapore owes its wealth not to oil but to high productivity and skills, a low level of government corruption and a business-friendly economy.

The mainstream economists argue this is possible mainly due to the establishment of a market-based financial system. Theoretically, it is argued that efficient markets are more effective as they reduce the need for investors to research firms as new information will be reflected in public stock prices (World Bank, 1997). In some developing countries, large banks such as state-owned banks, are less interested in performing financial functions and are more focused on political goals while extracting rents. We must not forget that the market-based financial system promotes corporate governance, particularly in equity markets through the hostile takeovers of under-performing companies.

However, the differences in the performance in the financial structures on growth tell that there could be other factors that can affect growth like the institutional development of the country. For example, recent research has shown support for stock market development, particularly for highly developed countries with strong institutions. Additionally, developed economies benefit more from market-based financial systems compared to less-developed countries, where bank-based financial systems affect growth more effectively due to a lack of access to finance. Institutions could include financial intermediaries and markets, and institutions are referred to as those that do not include banks and financial markets. Institutions can be defined as human-developed constraints that structure interaction and can be made up of formal and informal organisations with enforcement characteristics.

With China’s accession to the World Trade Organization (WTO) in 2001, it was clear that Washington and Beijing were — as a Chinese idiom has it — “sharing a bed but dreaming different dreams”. Bill Clinton, the then US president, hailed China’s membership as “removing [Beijing’s] government from vast areas of people’s lives” and promoting political reform. Jiang Zemin, China’s then leader, had a different take (Kynge and Fray, 2024).

The sharp divisions between the US and China widen as trade friction escalates between China and the West. As the world trade body falters, China is accelerating efforts to construct an alternative trade architecture that is insulated from US influence and centred upon the developing world (See Figure 9). With this challenging situation, China’s main strategy is to capitalise on ties with the “global south” fostered through its $1tn Belt and Road Initiative (BRI), an investment programme launched in 2013 that counts more than 140 countries in Asia, Africa, Latin America and elsewhere as its participants. The architecture under construction revolves around a China-centric network of bilateral and regional “free trade agreements” (FTAs), which allow for trade at low tariffs while also promoting direct investment flows.

China has free trade agreements with countries and territories accounting for almost 40 percent of its exports, which means that if the WTO’s mandate to keep the world open for liberalised trade unravels, China will have at least a partial back-up system in place, they add. None of China’s FTAs include the US or countries inside the EU. China, by far the world’s biggest exporter – shipped some $3.43tn around the world, its FTA network took roughly $1.3tn of that total. To put the size of this FTA footprint into context, China exports more to its FTA network than the world’s fourth and fifth-biggest exporters, the Netherlands and Japan, did all over the world during 2022.

The establishment of China’s FTA ecosystem gained impetus after the 2008 financial crisis instilled a deep sense of anxiety in Beijing over the stability of the world’s economy. A China-Singapore FTA in late 2008 was followed in 2010 by a China-ASEAN FTA with all 10 countries that make up the Southeast Asian economic grouping. But it was after the US excluded China from talks to join the Trans-Pacific Partnership, a big multilateral trade deal that was signed in 2016, that Beijing really threw its FTA programme into overdrive.

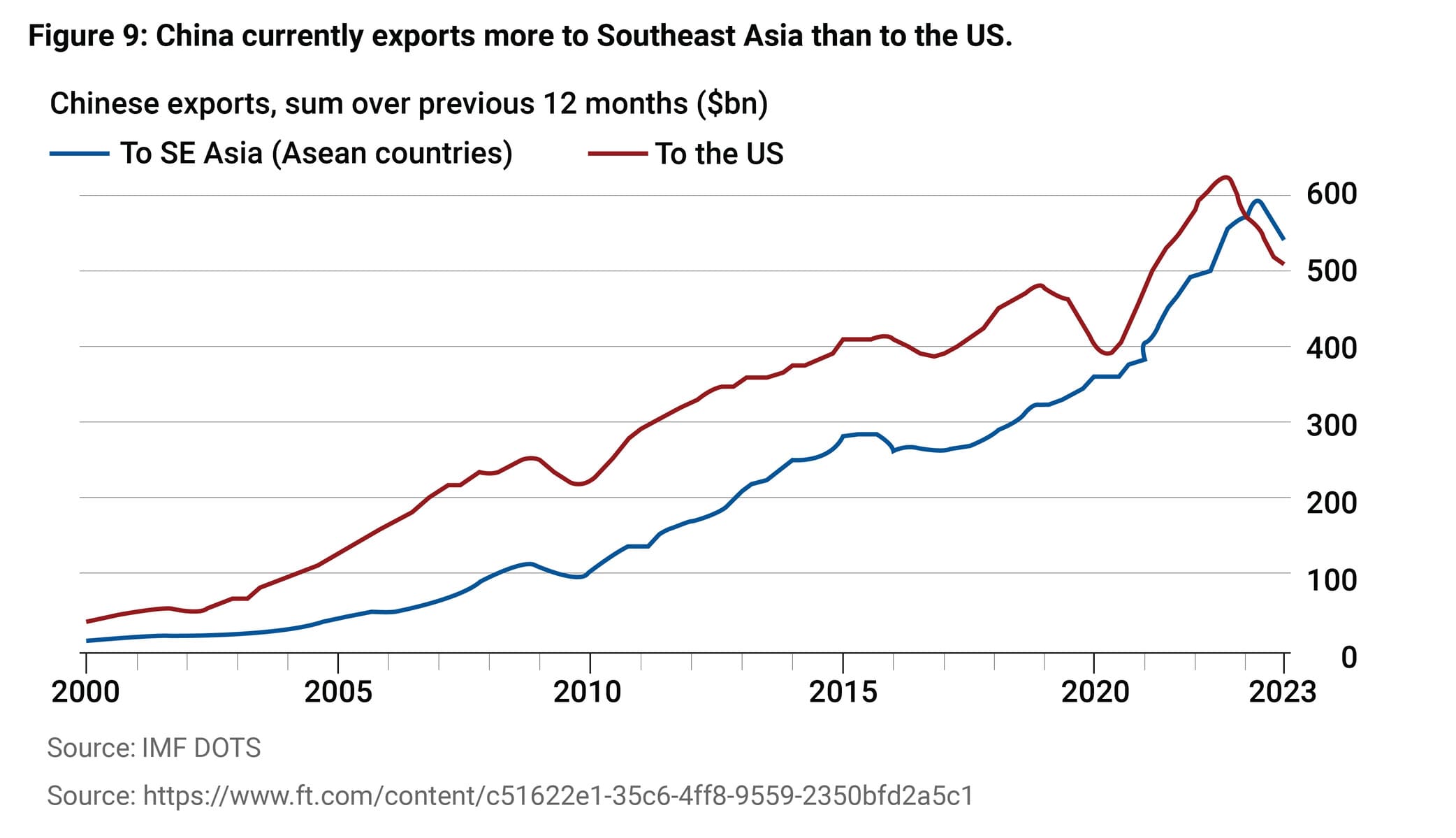

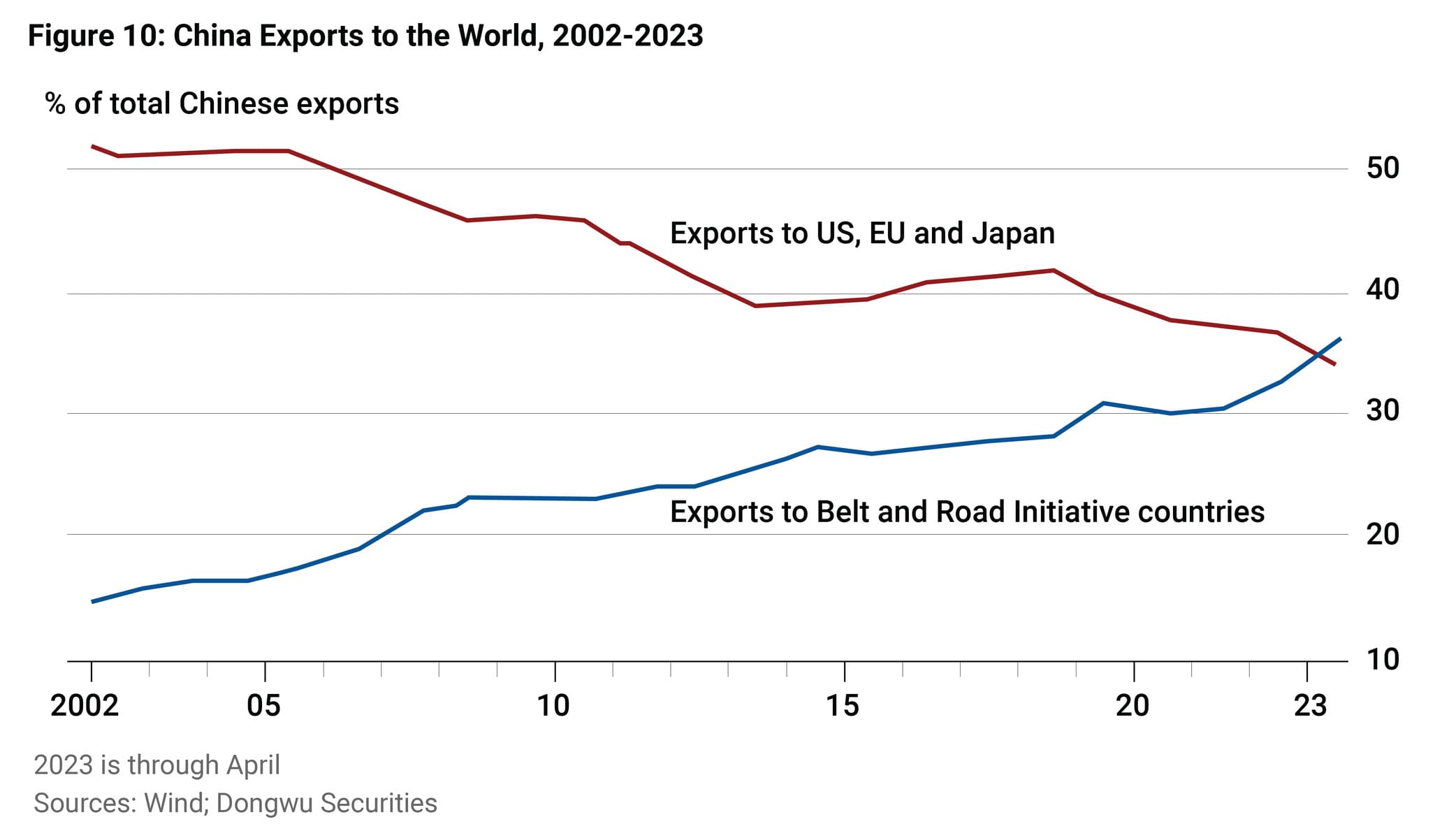

Its biggest success to date has been negotiating membership of the 15-country Regional Comprehensive Economic Partnership (RCEP), a huge regional FTA that went into force in 2022. The members of the RCEP contribute around one-third of the world’s GDP. But China is also negotiating 10 FTAs which, not including those that are upgrades of FTAs already in force, would account for around a further 4.3 percent of its global exports. Over the longer term, China would focus its trade towards the developing world by using its ties with the more than 140 countries covered by the BRI and signing FTAs with them where possible, Chinese experts say. This trend is well underway, says Gao, adding that China’s exports to the 10 member countries of ASEAN all of which are included in the BRI exceeded exports to the US in the year to October 2023 (See Figure 10). More broadly, China’s trade with the BRI countries exceeded that with the US, EU and Japan put together.

China’s commercial engagement with developing nations is evidence the world is tilting on its axis. It seems that China is not just trying to create an alternative world order. For example, the changes underway lie in an upsurge in investment flows and the signing of FTAs. Direct Chinese investment into ASEAN, which rose sharply from merely US$9 billion in 2019 prior to the COVID-19 pandemic to US$15.4 billion in 2022, is helping to transform the region’s economic destiny. ASEAN countries are sharply increasing their share in high-tech manufacturing sectors, which has attracted huge foreign inflows of capital in the region such as Penang in Malaysia for semiconductors and Kalimantan in Indonesia for electric vehicles and EV batteries.

Conclusion

Southeast Asia is emerging as a very important economic region, with a large population and a very integrated regional economy. We have discussed how for the last five decades the region’s economy has steadily grown and general living conditions have improved. Of course, the economic performance differed, but still, there is a strong optimism that the region would have a greater economic role in the future. China’s emergence as the second largest economy and its strategy to build more economic and trade ties with ASEAN countries has certainly boosted the region’s economic prospects. Of course, there will be challenges in the future but certainly, the world is changing and the four centuries of domination of the West is coming to an end sooner rather than later.

How these challenges and tensions are dealt with will depend on how aggressively China pursues its strategic goals, how the other two principal interested powers (the US and Japan) react, and how the ASEAN states singly and collectively move to assure their own interests and security. The present evolving relationship between China and the countries of Southeast Asia cannot be understood simply in terms familiar to hard-headed realists among international relations analysts. It is not enough to compare political institutions, economic strengths and weaknesses and military force levels: while these considerations are important, they do not of themselves determine how states will relate to other states in crises. Other, often emotive, factors come into play, such as national pride or traditional enmity.

The rapidly changing trade pattern is being seen in the Southeast Asian region. For example, in Southeast Asia, bilateral trade reached US$395 billion in 2016, accounting for 15 percent of SEA’s external trade and China is the top trading partner for the Southeast Asian region. Since 2009, China emerged as the most important trade partner of the SEA countries, after the global financial and economic crisis. The countries of SEA increasingly look towards China for closer economic relations to protect their economies after the 2009 global financial crisis.

About the Author

Dr. Kalim Siddiqui is an economist specialising in International Political Economy, Development Economics, International Trade, and International Economics. His work, which combines elements of international political economy and development economics, economic policy, economic history and international trade, often challenges prevailing orthodoxy about which policies promote overall development in less-developed countries. Kalim teaches international economics at the Department of Accounting, Finance and Economics, University of Huddersfield, UK. He has taught economics since 1989 at various universities in Norway and the UK.

References

- Cumings, B. (1994). “Japan and North East Asia into 21st Century”, Conference on Japan in Asia, May, New York: Cornell University.

- Siddiqui, K. (2024). Revisiting the Japan’s Economic Stagnation. World Financial Review, February-March.

- Siddiqui, K. (2023). Developmental Challenges: Export vs Import-Substitution in Industrialisation in Developing Countries. World Financial Review, October-November, pp.1 – 15.

- Siddiqui, K. (2023). The Political Economy of Shanghai Cooperation Organisation (SCO) and the Growing Regional Multilateral Ties. World Financial Review, February-March, pp. 2-14.

- Siddiqui, K. (2021). The Import Substitution Policy in the Post-Colonial Countries. World Financial Review, November-December, p.76 – 84.

- Siddiqui, K. (2021). Trade Liberalisation, Comparative Advantage, and Economic Development: A Historical Perspective. World Financial Review, May-June, p.65 – 74.

- Siddiqui, K. (2021). The Importance of Industrialisation in Developing Countries. World Financial Review, January February, p.60 – 73.

- Siddiqui, K. (2019). One Belt and One Road, China’s Massive Infrastructure Project to Boost Trade and Economy: An Overview. International Critical Thought. 9(2): 214 – 235.

- Siddiqui, K. (2018). David Ricardo’s Comparative Advantage and Developing Countries: Myth and Reality. International Critical Thought, 8(3): 1-28, September.

- Siddiqui, K. (2017). Globalization, Trade Liberalisation and the Issues of Economic Diversification in the Developing Countries. Journal of Business & Economic Policy 4(4): 30 – 43.

- Siddiqui, K. (2016). A Study of Singapore as a Developmental State. (Edit) Young-Chan Kim. Chinese Global Production Networks in ASEAN, 157 – 188, London: Springer.

- Siddiqui, K. (2015). Perils and Challenges of Chinese Economic Development. International Journal of Social and Economic Research 5 (1): 1 – 56.

- Siddiqui, K. (2015). Political Economy of Japan’s Decades-Long Economic Stagnation. Equilibrium Quarterly Journal of Economics and Economic Policy 10(4): 9 – 39.

- Siddiqui, K. (2012). Malaysia’s Socio-Economic Transformation in Historical Perspective. International Journal of Business and General Management, 1(2): 1 – 50.

- Siddiqui, K. (1995). Role of the State in South-East Asia. The Nation, May 27.

- Kynge, J. and Fray, K. (2024). China’s Plan to Reshape World Trade on its Own Terms. The Financial Times, February 26, London. https://www.ft.com/content/c51622e1-35c6-4ff8-9559-2350bfd2a5c1

- World Bank (1997). East Asian Miracle, Washington DC: World Bank.

{kind=link}