The global crisis and the austerity programmes in most developed countries have cast light on the role of expatriated savings in widening the gap between domestic resources and financing requirements and also in eroding the tax revenues, thus reducing economic growth potential. Offshore tax havens have become the focus of academic research and a point of contention for governments, scholars and the media.

Indeed, the issue is of crucial importance for countries that face structural deficits, declining competitiveness and institutional weaknesses, striving to reduce national debt burdens in order to regain domestic and international credibility. In emerging market countries, private capital outflows have played a catalytic role in financial crises, while raising eyebrows in IFIs when development aid flows are recycled by corrupt elites outside of the home country.

In this article, we tackle capital flight from a country risk point of view. Risk meaning that things might not turn out as expected. This is so because risk stems from uncertainty, the latter being caused by a deficit of information and economic intelligence. Whatever the range of indicators a seasoned analyst will use to measure risk (liquidity, solvency, economic structure and socio-political data), he will never match the vantage point of residents who are immersed in their country’s volatile specificity. Hence our strategy of looking over residents’ shoulders to monitor the arbitrage between domestic savings and capital leakages.

1. The push and pull forces of capital flight

From a private economic agent’s standpoint, expatriated capital is a symptom of distrust in the country’s macroeconomic and socio-political stability. The internal “centrifugal forces” of capital pushed out of national boundaries are numerous. Capital flight reacts to, and often anticipates, bad economic policies, including mismanagement of interest and exchange rates, excessive tax burden, inflation, budget deficit, and an excessive public sector debt. One can also observe external “centripetal forces” that pull capital outside the home country, due to dynamic foreign financial systems, offshore tax havens, booming stock markets in foreign countries, and high external real interest rates. Econometric analysis has shown that private capital leakages stem from a combination of various policy and political factors conducive to private savings expatriation1.

First, money laundering flees a country because of fear of being caught by the tax and judiciary authorities. Second, private expatriated savings react to price misalignment between the domestic economy and the rest of the world, such as overvalued exchange rate and negative real interest rates. Third, private capital flees a country because corruption and institutional weakness do not provide a stable and conducive socio-political environment for safe savings and profitable investment. The key issue then is whether capital flight can be used as reliable early warning signal of country risk volatility.

Calculating and monitoring private capital outflows is a challenging ambition, for government officials and scholars, as well as risk analysts. The reason for this challenge seems evident: data, by definition, are scarce and of low quality. Investment in offshore financial and real assets boils down to a black box. One fruitful source, however, stems from the BIS (Bank for International Settlements) data on privately held deposits in banks by citizens outside their countries of origin. This method adopts a stock approach to capital flight2. The working hypothesis is that a significant increase in the rate of capital outflows will be reflected in the accumulation of private external assets held in international banks outside the home country. These statistics omit mutual funds, private trusts, custodian accounts, and money market funds that hold assets in international banks. Thus, these figures are conservative, understating such cross-border deposits belonging to either private individuals or corporations.

The two polarised cases of Vietnam and Norway illustrate these push and pull forces of capital flight.

2. The case of Vietnam: Econo-mic overheating, corruption, and capital flight

Vietnam is the archetype of a dynamic emerging country that has faced inflation, overvalued exchange rate, weak banking system, and twin deficits, i.e. both fiscal and balance of payments, coupled with shrinking official reserves. Vietnam, a country whose GDP per capita reaches $1500 with a widening wealth gap, has been in overheating mode for the last two decades, with GDP growth rates averaging 8% until the global crisis, and 6% since then. The acceleration in Vietnam’s inflation, particularly since 2005, led to a real effective appreciation of the Vietnamese Dong that the central bank (SBV) did not tackle until 2011, i.e. too late to enhance the competitiveness of the country and to stem capital leakages. In addition, the stock market crisis starting in the second half of 2007 stimulated “push forces”. Vietnam is a case study of economic overheating. Unsustainable growth rates of more than 8% in the mid-2000 fuelled rising inflation and large current account deficits that were financed by FDI, i.e. non-debt creating flows. The crisis was thus postponed and adjustment was avoided despite mounting signs of structural imbalances. The crisis erupted in 2008 when the deficit reached 12% of GDP with average inflation culminating at 23%. Exports dropped and international reserves shrank to only 2 months of import cover, until today. The combination of unabated inflation, negative real interest rates and overvalued exchange rates has led to growing expatriated savings.

The sharp rise in capital flight volatility during the 1993-2012 period can be attributed to (a) the 1997-98 Asian crisis and London Club debt reduction agreement coupled with large Errors & Omissions, (b) the 2005 rapid increase in inflationary expectations and the drop in FDI, (c) the 2007-08 inception in the global financial crisis that coincides with the Dong’s real appreciation despite several rounds of nominal depreciation, coupled with widening trade deficit and the stock market bubble, and (d) the 2010-12 devaluations of the Dong that are followed by tight capital controls and a narrowing of the official and parallel exchange rates gap. The devaluation alone did not solve the fundamental problems of lack of domestic confidence in the Dong; hence a drop in capital flight did not occur before end-2012. Tighter monetary policy and a more competitive exchange rate induced private nonbank agents to repatriate their savings at home, helping Vietnam to rely on domestic savings more heavily to finance long-term development objectives. The IMF praised Vietnam’s return to normalisation, though with moderate enthusiasm, in an April 2013 report: “Going forward, recent stabilization gains need to be consolidated through appropriate macroeconomic policies to further bolster international reserves and fiscal buffers.”3

The graph above illustrates the evolution of Vietnam’s private deposits in international banks over the 1993-2012 period (Source: BIS Quarterly Report). One can observe expatriated private savings climbing to $1800 million at end-2011 from roughly $500 million at end-2006.

The root causes of Vietnam’s crisis do not stem from the economic sphere only. Capital flight was also a rational reaction to the country’s poor governance track record. Vietnam has endorsed the so-called « 40+9 Recommendations » of the Financial Action Task Force to enhance financial transparency and to fight corruption and money laundering. The country belongs to the Asia/Pacific Group on Money Laundering since 2007. The conclusions of the first report that was released in July 2009 were, however, appalling: “Vietnam does not have any comprehensive anti-money laundering laws that criminalize laundering. The authorities cannot demonstrate that there is an effective system in place due to a lack of statistics provided.”4

Corruption is also a deeply rooted problem in Vietnam, with no sign of improvement. The corruption perception index of Transparency International gives Vietnam a stable ranking of 123, in the neighbourhood of Sierra Leone and Mozambique, among a total of 180 countries. As the NGO underlies: “The global financial crisis and political transformation in many Asian countries exposed fundamental weaknesses in both the financial and political systems and demonstrated the failures in policy, regulations, oversight, and enforcement mechanisms”.5 The World Bank’s governance indicators show no sign of progress of Vietnam in the two key domains of “voice and accountability” and “control of corruption”.6 Regarding the “Doing Business” rating of the World Bank, Vietnam’s rank is only 99 among 185 countries in 2013, thus in the neighbourhood of Zambia and Kosovo. Regarding COFACE’s country risk rating, Vietnam belongs to the C risk-rating category, with a Business Climate rating of only C, alike Uganda and Albania. COFACE considers Vietnam’s rating to be watchlisted with negative implication, given that “Vietnam’s Achilles’ heel remains its problems of governance and especially corruption, which perpetuates corporate credit risk, along with persistent business environment shortcomings.”7 And the latest WEF’s Global competitiveness index ranks Vietnam only 75 out of 144 countries, well below Sri Lanka, Indonesia, and Thailand.

The conclusion regarding Vietnam is that large and growing capital flight has proved to be a reliable early warning indicator of mounting country risk. A traditional analysis of the country’s macroeconomic indicators would have concluded in the mid-2000s that the country faced a “tighter but sustainable liquidity situation”. Indeed, the growing balance of payment deficits was financed by large FDI and international bank lending until recently. The looming risk of twin real estate and stock market bubbles did not cut Vietnam off from global capital markets. International bank lending grew 130% between the eruption of the global financial crisis in 2007 and end of 2012. On-going market access sharply contrasts with countries such as Indonesia, Laos, Malaysia, Myanmar, Philippines and South Korea which experienced abrupt reduction in bank lending. Indeed, while Vietnam’s external private deposits grew quickly since the 1997 Asian crisis, accelerating in 2005, the increase in international bank lending gets much larger, resulting in a declining ratio of bank deposits to bank credits, to 10% in December 2012 from 19% in December 2005. International banks were happy making profits on both sides of their balance sheets, as Vietnamese private agents kept shifting their assets overseas while Vietnamese companies kept relying on international bank loans.

3. The case of Norway: Sustainable development and good governance, with appreciating exchange rate

In emerging market countries, capital flight is a good early warning indicator of country risk. Macroeconomic mismanagement and bad governance are powerful push forces for private capital leakages. But then what about surplus countries that still enjoy a rare combination of dynamic growth, prudent macroeconomic policies and good governance? Norway illustrates the rational behaviour of private economic agents who profit from an appreciating currency for investing in offshore banking accounts. Offshore deposits, indeed, respond to, and often anticipate, the change in real effective exchange rate. That is, if a currency becomes severely overvalued, private deposits outside the country are likely to rise as a hedge against an upcoming exchange rate adjustment and also to benefit from a stronger external purchasing power.

The IMF has praised Norway’s robust economic performance amidst considerable global turbulence. Its economic recovery has been assisted by buoyant consumer spending, improving terms of trade, a rebounding housing market and supportive monetary policy, resulting in a relatively shallow recession compared to its regional peers. Norway is widely considered as a country that enjoys good governance, sustainable development and a good business environment that is illustrated by an impressive investment/GDP ratio of 24%. The most recent “Doing business index” of the World Bank ranks Norway 6th out of 185 countries. Regarding governance, Transparency International ranks Norway as one of the less corrupt country, namely 7th out of 176 countries and territories. All in all, Norway remains one of the very few members still in the elite club of Triple A countries, with Canada, Germany, Sweden, Switzerland and a few others.

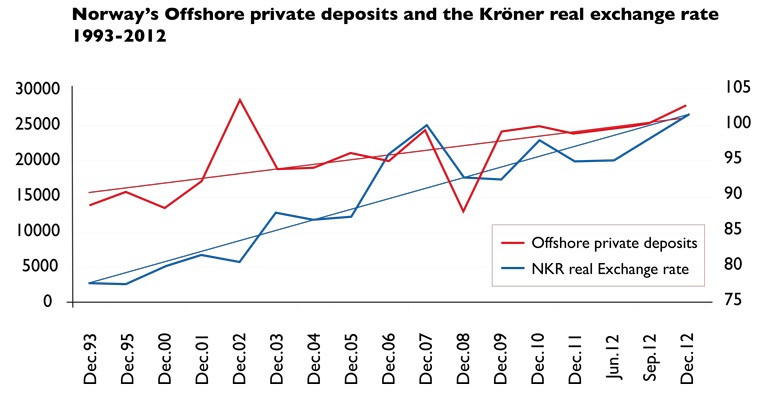

Despite these strong socio-economic credentials, private offshore deposits in international banks have reached over $26 billion at end of 2012, equivalent to NKR 151 billion, a ten-fold increase since the mid 1990s. This volume of expatriated deposits amounts to around 4% of GDP, or 50% of official reserve assets currently. A sharp increase occurred in 2003, when private capital outflows increased twofold. The chart above provides some explanation for the rising volume and volatility of expatriated savings outside Norway. One can observe a strong correlation between the real effective exchange rate of the Kröner and external bank deposits. The former takes into account both nominal exchange rate developments and the inflation differential vis-à-vis trading partners. It is a measure of international competitiveness, and it serves as an operational target for the conduct of monetary policy. When the Kröner gets stronger vis-à-vis the US dollar, the Euro or emerging market currencies, private individuals and corporations shift their liquid assets outside Norway to benefit from their comparative advantage to acquire foreign currency assets. When the Kröner gets weaker, like in 2008, one observes a marked decline in offshore private deposits.

Norway is thus a rare example of a country where expatriated private deposits cannot be claimed “capital flight” given the quality of the socio-economic environment. However, private capital outflows illustrate the rational behaviour of economic agents who benefit from a (sometimes too) strong currency to shift their assets outside the home country. In the current “currency war” environment, it seems that every country, except for Norway, strives to weaken its national currency. Expatriated private savings are not about to dry up just yet.

About the Author

Michel Henry Bouchet, former Senior Economist at the World Bank and CEO of Owen Stanley Financial SA, is currently Distinguished Finance Professor at SKEMA Business School and Chief Strategist – North Sea Global Equity Management SA. He has published widely in both professional journals and books in North America, Europe, and Latin America in the areas of International Finance, Globalization, and Country Risk (Pearson, Wiley, Greenwood, Felaban, ESAN…etc.) www.developingfinance.org

References

1. For a review of literature, see: Bouchet, MH & Groslambert, B, ESAN Cuadernos de Investigacion, 11 (20), June 2006.

2. Bouchet, MH – Institute of International Finance 1986, Bouchet MH & Kharrat O, 2013 (forthcoming).

3.http://www.imf.org/external/np/sec/pr/2013/pr13143.htm

4. http://www.apgml.org/documents/docs /17/Vietnam%20ME1.pdf

5. Transparency International, Regional Highlights, 2009. Vietnam’s regional ranking is 22nd among 33 countries of the Asia-Pacific region.

6. http://info.worldbank.org/governance/wgi/sc_chart.asp 7. Coface ‘s risk assessment of Vietnam (June 2013):http://www.coface.com/Economic-Studies-and-Country-Risks/Viet-Nam

{kind=link}