")

Introduction

Globalisation today refers to the increasing economic integration beyond national borders, driven by the processes of trade liberalisation and financial deregulation. Large corporations have long sought to dominate global markets, viewing access to international markets as a means to exert control over resources and expand their influence. In theory, global governance aims to improve the effectiveness and efficiency of delivering public goods. Additionally, it calls for greater transparency, accountability, and representation to strengthen democratic processes (Siddiqui, 2020a).

Globalisation entails a growing proportion of economic, social, and cultural transactions occurring across countries, which is often equated with ‘internationalisation.’ Hirst and Thompson (1996) define it as a shift away from self-sufficient national economies, which may lead to inefficiency and stifle competition, toward a single, integrated global economy. However, Wade (1996) contends that the extent of globalisation has been overstated. (Stiglitz, 2002)

In the aftermath of the Second World War, international institutions such as the International Monetary Fund (IMF), the World Bank, and the General Agreement on Tariffs and Trade (GATT) were established as the United States emerged as the world’s dominant power. The GATT, which was later replaced by the World Trade Organization (WTO) in 1995, was originally designed to facilitate trade agreements among sovereign nations. Initially focused on free trade in manufactured goods, the WTO now also prioritises trade liberalisation in services, agricultural commodities, and financial sectors. While the inclusion of these additional areas is strongly supported by the US, the European Union, and large corporations, it faces strong opposition from developing countries. Meanwhile, the IMF was created to provide short-term financial assistance to nations experiencing balance-of-payments crises (Siddiqui, 2020a).

Following the collapse of the Soviet Union in 1991, the push for globalisation and market integration became a key policy goal for the US, sparking extensive debate among scholars. Proponents of globalisation argue that it fosters competition, efficiency, and trade, while critics contend that it represents a new guise for the historical Western policies of expansion and domination (Siddiqui, 2015).

A new phase of internationalisation emerged in the aftermath of the crisis that struck the post-war order in the mid-1970s, contributing to the expansion of the global economy while gradually undermining US hegemony. The intensification of international production, particularly after the 1970s crisis under Pax Americana, was coupled with domestic inflationary pressures, trade union militancy, rising unemployment, and declining profits – factors that propelled the evolution of capitalism.

The radical critique of capitalism has a long history, rooted in the works of Marx, Lenin, Luxemburg, and other early 20th-century theorists of imperialism. Marxist scholars have argued that capitalism, as it spreads, develops the forces of production globally. In contrast, other theorists emphasized that the underdevelopment of former colonies would persist, with global inequalities widening rather than narrowing. According to this view, capitalism has entrenched global inequalities, fostering the development of a select few countries while perpetuating the underdevelopment of others (Siddiqui, 2023).

Capitalism, Accumulation Crisis, and Global Markets

For capitalism to endure, there is a relentless pursuit of higher profits, greater market access, and rapid advancements in industrial and commercial production. These forces profoundly impact class relations, capital accumulation, and national economies. This fierce process of expansion and transformation is essential to capitalism’s survival. As Karl Marx (1974) observed, the “bourgeoisie cannot exist without constantly revolutionising the instruments of production, and thereby the relations of production, and with them the whole relations of society.” This insight is crucial not only for understanding the dynamics of the 19th century but also for interpreting the developments of the 20th century and the ongoing transformations of the 21st century (Siddiqui, 2023).

Globalisation also involves the deregulation of markets and the financial sector. Advances in financial technology, reductions in transaction costs, and the removal of restrictions on cross-border capital flows have led to significant capital movements between countries. Over recent decades, these large capital flows have often triggered currency crises and recessions in many nations. While currency crises are not new, the liberalisation of financial markets has made financial and banking crises more frequent. (Siddiqui, 2017)

Globalisation encourages the free flow of goods and capital across borders. However, the unrestricted mobility of capital means that if a country’s macroeconomic policies are deemed unsuitable by global financial markets, foreign capital can rapidly leave the country. Such an exodus of capital can trigger financial crises, highlighting the critical importance of maintaining foreign investor confidence to implement policies acceptable to international finance.

Democracy is founded on the principle that citizens have the freedom to elect a government that will pursue policies reflecting their preferences. However, in developing countries, if the policies of elected governments do not align with the expectations of global finance, this can lead to capital flight, with severe consequences such as reduced investments and slower economic growth. In such situations, the sovereignty of the people becomes secondary to the interests of foreign investors and financial markets.

For example, a government may seek to improve the socio-economic conditions of its citizens by increasing spending on health and education, funded either by taxing the wealthy or through a larger fiscal deficit. However, both of these policies are typically opposed by global finance. This is why global financial markets and international institutions like the IMF generally discourage fiscal deficits that exceed 3% of a country’s Gross Domestic Product (GDP). Additionally, under financial liberalisation, raising taxes on the wealthy can prompt investors to relocate to low-tax jurisdictions.

Historically, global empires extracted tributes (or surplus) from the territories they occupied. These empires fostered a world economy through a complex division of labour and extensive commercial exchange. Early modern empires, led by emerging merchants and traders from Spain, Portugal, Holland, France, and Britain, expanded outward in search of new economic opportunities. This expansion was supported by the development of strong states in the ‘core’ of the burgeoning capitalist world economy.

In the latter half of the 15th century, monarchies in Western Europe, benefiting from the decline of feudalism, identified trade and territorial conquest as new avenues for wealth. These states defended the interests of their merchants and traders with military force, playing a key role in building the structures of modern capitalism. Initially, they colonised the Americas, economically incorporated other European nations, and eventually extended their influence across the globe during the 19th and early 20th centuries.

European control over foreign territories resulted in a global division of labour, with the ‘core’ representing economically and militarily dominant centres, and the ‘periphery’ comprising regions forcibly subordinated through colonisation and occupation, such as Latin America, Africa, and Asia. In this international division of labour, the core and periphery engaged in unequal exchanges—high-wage commodities like manufactured goods flowed from the core, while low-wage commodities, such as raw materials, were extracted from the periphery.

Economic surpluses appropriated from colonies and semi-colonies were transferred from the periphery to core countries, enriching the latter while leaving the former underdeveloped. This accumulation resulted in wealth for the core and widespread poverty, famines, and mass starvation in the periphery (Siddiqui, 2020b). The international division of labour was designed to benefit the core, sharply increasing global inequalities. The expansion of capitalism has always been characterised by uneven accumulation. Through the processes of capitalist globalisation, accumulation has become increasingly transnational, as global circuits of finance and production extend across borders. Samir Amin (1997) criticised the rise of giant corporations, describing it as an alliance between corporations and the state, leading to greater control over resources in the Global South.

Similarly, Britain unilaterally adopted ‘free trade’ by repealing the protectionist ‘Corn Laws’ in 1846 and later signing the Cobden-Chevalier Treaty with France in 1860. In contrast, the US never fully embraced the free trade system and instead increased protectionism from the 1870s onward. Adam Smith and David Ricardo argued that it was in a country’s best interest to adopt free trade, regardless of whether other nations followed suit (Siddiqui, 2018).

Britain had adhered to the ‘Gold Standard’ since 1819, but other countries joined much later—Germany in 1871, France in 1875, and the US in 1879. However, the gold standard was not the result of any international negotiation or agreement, nor was it managed by any international organisation.

At the end of the Second World War, the US emerged as the world’s most dominant economy, producing more than 50% of global output and 35% of global manufacturing. In contrast, European economies were devastated by the war and needed to import commodities, technology, and capital to rebuild their industries. However, over the past forty years, the global economy has shifted, with European, Japanese, and more recently Chinese economies experiencing significant growth, leading to dramatic changes in global trade patterns. For instance, ASEAN countries are now larger trading partners than the US, and China has surpassed the US as Africa’s largest trading partner.

Since the 1950s, the US dollar has served as the backbone of US global power, functioning as the world’s reserve currency. Without a strong dollar, the US would struggle to maintain its global hegemony. “De-dollarisation” refers to the declining role of the US dollar in international financial transactions and its status as a reserve currency. This would involve a shift toward using multiple currencies in international trade. For example, US sanctions forced Russia to seek alternative currencies for its transactions.

Exports and foreign capital have been central to the neoliberal globalisation model, with developing countries encouraged by institutions like the IMF, World Bank, and mainstream economists to focus on export promotion and attracting foreign investment as pathways to economic development (Siddiqui, 2019). This approach, known as “export-led growth,” is often exemplified by the successful transformation of East Asian economies over the last fifty years. Once impoverished, these economies are now seen as prosperous, a phenomenon frequently referred to as the East Asian “miracle.” In contrast, countries like India and Brazil, which, according to the World Bank, pursued an “inward-looking” development strategy and did not prioritise exports, have experienced slower growth, persistent unemployment, and widespread poverty (Siddiqui, 2016).

Current globalisation is heavily reliant on neoliberal economic policies, which emphasize pro-market reforms (Girdner and Siddiqui, 2008). These reforms focus on policies that increase reliance on private capital for resource mobilisation and involve major economic shifts such as privatisation, deregulation of trade and finance, financialisation, and globalisation. In the US and Britain, these changes began in the late 1970s and early 1980s under President Reagan and Prime Minister Thatcher. Privatisation involves selling off public assets, including essential utilities like water, gas, electricity, railways, and public housing, while outsourcing services within public sectors such as the NHS, education, and public administration. Deregulation meant removing legal restrictions on markets, particularly in areas such as finance, labour, and capital flows. Financialisation transferred power to private enterprises in sectors such as finance and insurance, with the rise of complex financial instruments like derivatives. Globalisation facilitated further economic integration through increased trade and the free flow of capital (Siddiqui, 2019).

These changes represented a shift in power from the state to the private sector, particularly to large corporations. Historically, this trend can be traced back to attempts in the 1930s to revive liberal capitalism in Europe, the UK, and the US, which had come under pressure from increased state intervention. However, the crisis of the 1930s, followed by global conflict, resulted in a shift toward social democratic policies. These policies included expanding welfare and labour rights, implementing active fiscal and monetary measures, and constructing a global capitalist order under US hegemony. This system allowed individual nation-states to develop institutions and practices suited to their own economic and historical contexts.

When examining countries that have pursued export-led growth strategies, there are two distinct cases. The first includes nations with large current account surpluses and substantial foreign exchange reserves, such as China, South Korea, Taiwan, and Germany. The second group consists of countries with significant trade deficits, such as Brazil, India, Indonesia, and Mexico. These countries often rely on private financial inflows to reduce current account deficits and balance payments. Even when they accumulate foreign exchange reserves, these are typically financed through borrowing, a reality for many nations in the Global South.

The idea of export-led growth was discredited by Western governments during the interwar period and the Great Depression. However, global capitalism, after a period of large-scale import substitution in much of the Global South following independence, has seen these policies reemerge through neoliberal globalisation.

Capitalism first took shape during the Industrial Revolution, which began in Britain’s cotton textile industry. However, Britain did not produce raw cotton, necessitating access to primary commodities grown in tropical and semi-tropical regions. To sustain its industrial growth, Britain, along with other Western European nations, required a steady and affordable supply of raw materials. The success of these industries hinged on securing cheap access to these resources. Furthermore, to achieve economies of scale and expand production, new markets were needed to absorb the surplus of finished goods. Consequently, these challenges were addressed through the control of tropical and semi-tropical regions, which were essential for the expansion of European industries.

Capitalism, at some stage, must address rising inequalities both within and between countries (Siddiqui, 2018). It also needs to strike a balance between production and consumption, particularly given the rapid automation of industries and the increasing use of new technologies, including artificial intelligence, which significantly reduces the need for human labour. Despite GDP growth, job creation and employment opportunities have lagged, a reality particularly unsustainable for developing countries with large unemployed populations. Therefore, state intervention may be required to redistribute surplus in the form of income protection, boosting domestic demand so consumers can afford domestically produced goods and services. Unlike in the 18th and 19th centuries when Britain exported a large portion of its population to colonies, there is no longer the possibility of large-scale migration to the Americas, Australia, New Zealand, or South Africa.

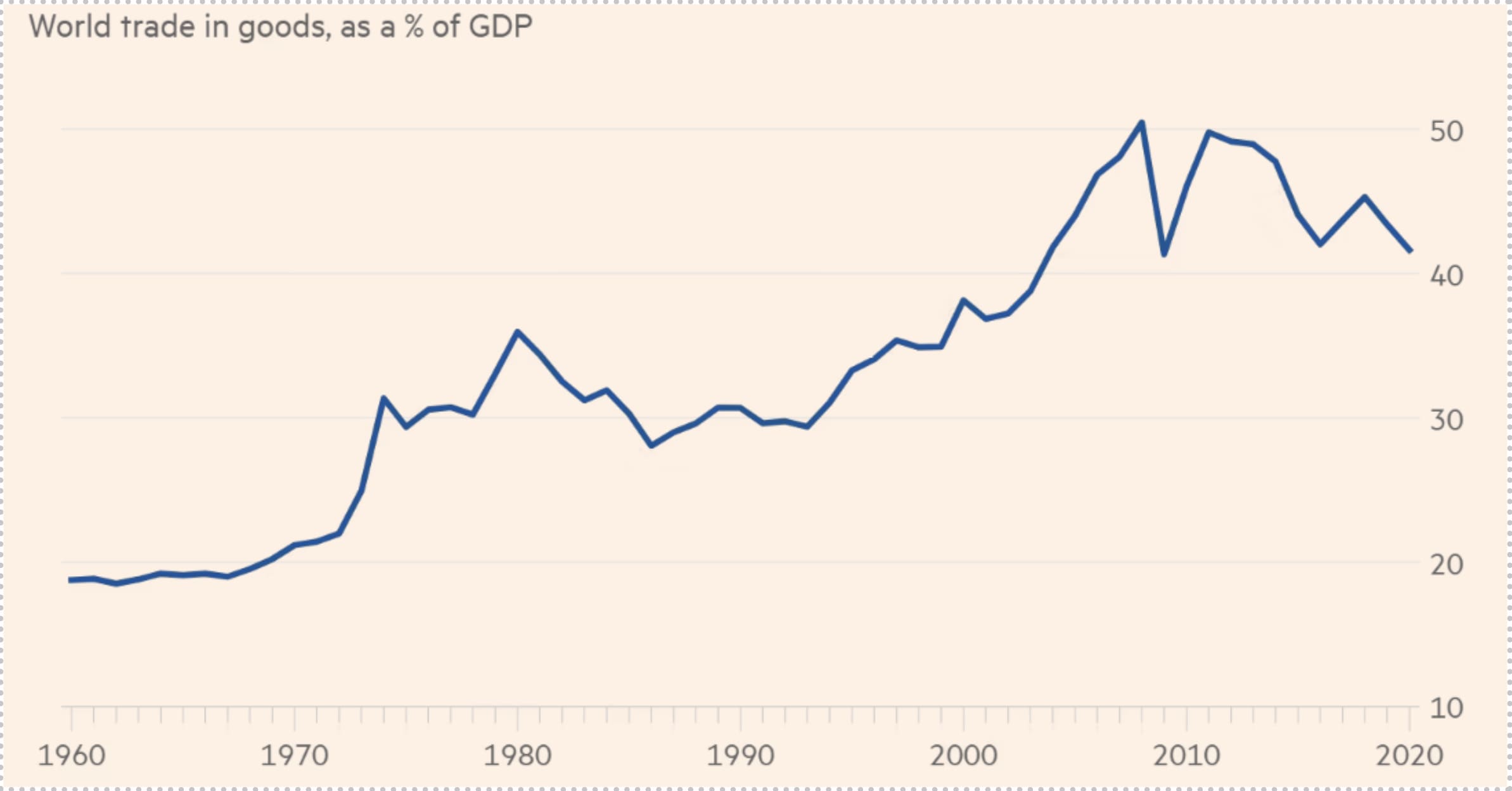

Recent advances in information technology have allowed companies to relocate production to areas where labour and raw materials are cheaper, generating greater profits. Additionally, the rise of broadband internet enables “trade in offices”- if an employee can work from home, the same tasks can be outsourced to workers in developing countries at lower costs. Since 2008-2009, world trade in goods has stagnated and has yet to recover to its pre-global financial crisis peak in 2015, as seen in Figure 1 (Wolf, 2022).

Figure 1: World Trade in Goods Relative to Output (trade in goods as a % of GDP).

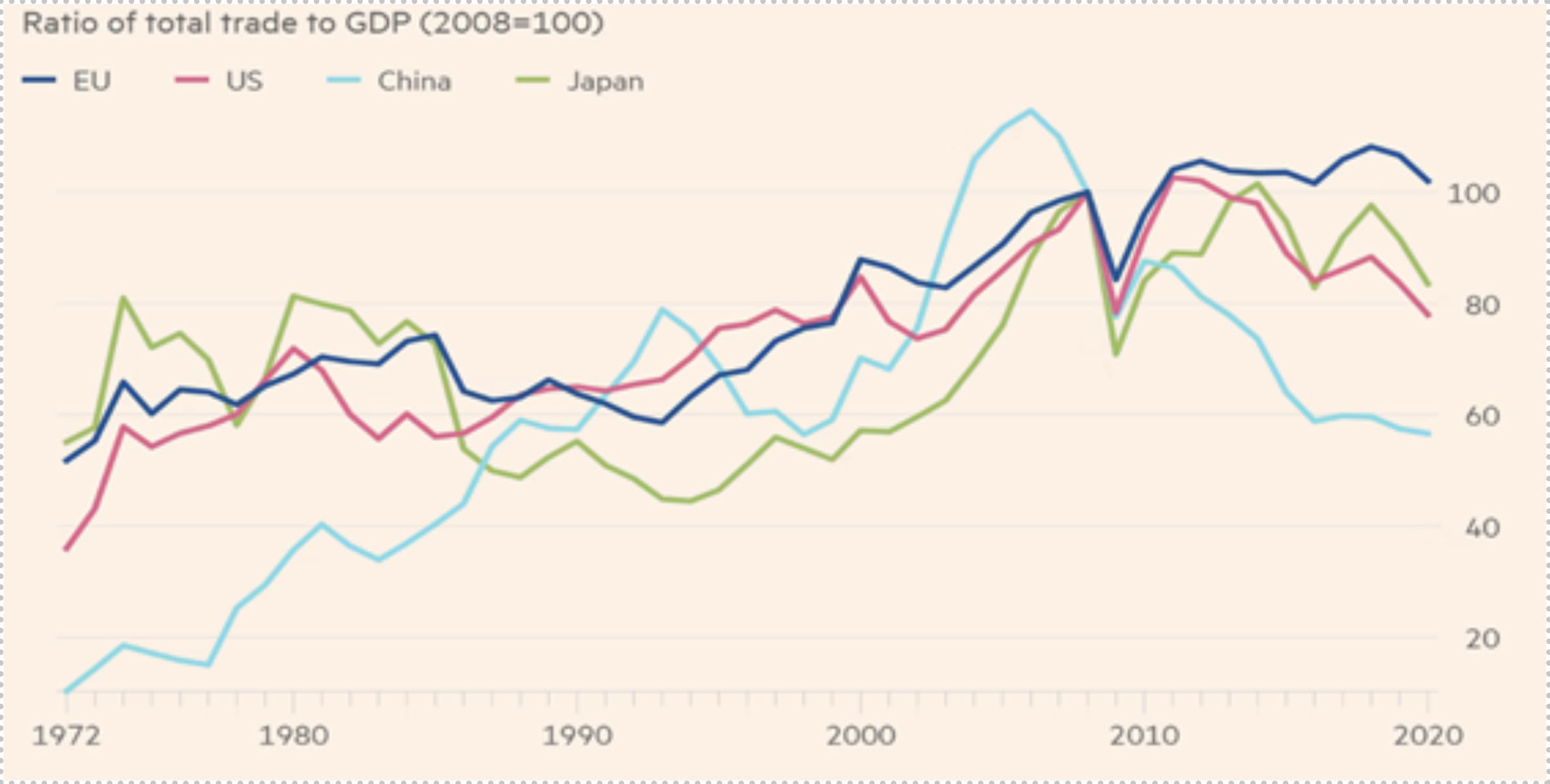

The economies of developed countries have not always been as open as proponents of globalisation and market integration often suggest (See Figure 2). Historically, these nations maintained protective measures before embracing the current era of free trade. The push for greater openness and market integration has primarily been driven by large corporations, which seek the benefits of expanded markets for the production and sale of their goods, as well as the opportunity to further monopolise global resources.

Figure 2: Peak in Openness to Trade across the Big Economies.

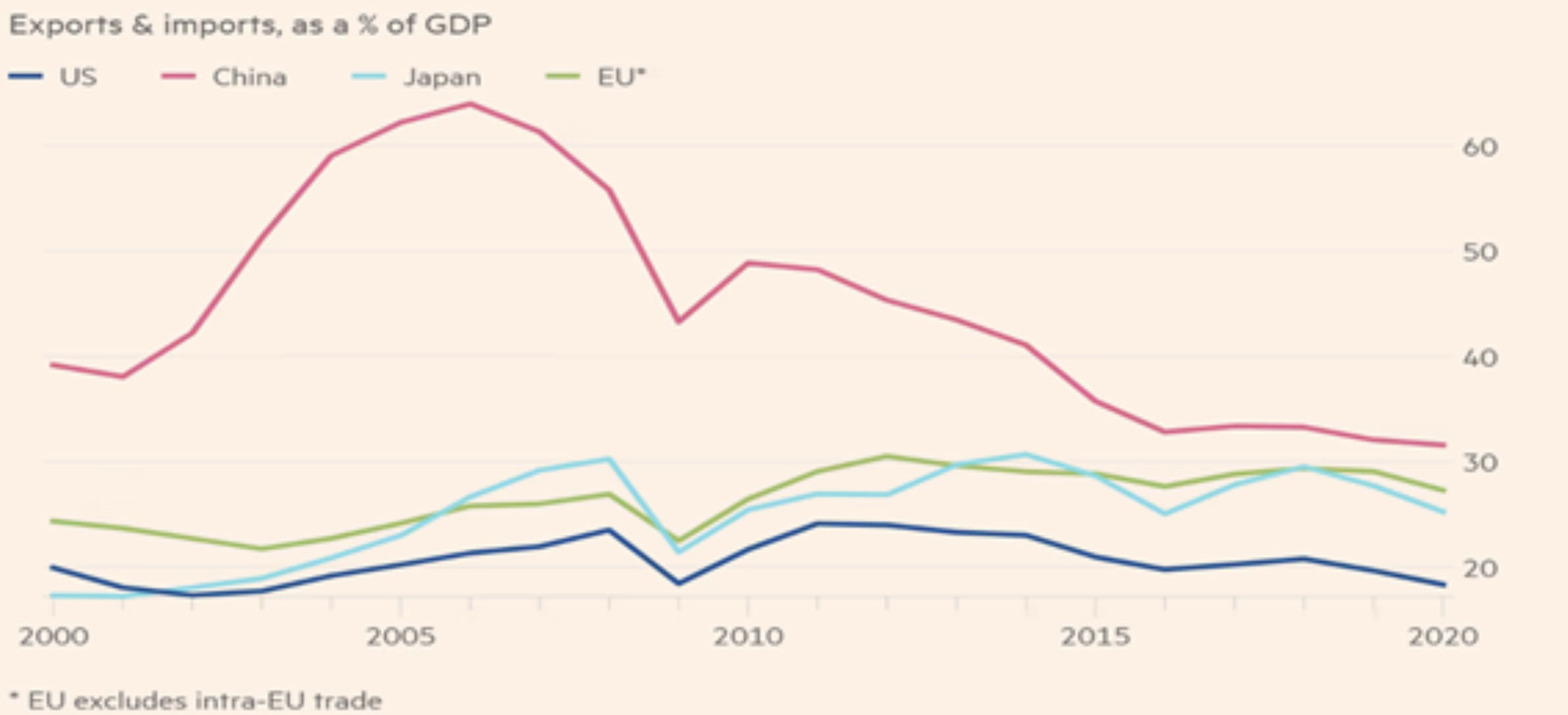

The trade ratio of China, the world’s second-largest trader of goods, peaked in 2006 (as shown in Figure 3). Similarly, the trade ratios for the third and fourth largest goods traders, the US and Japan, peaked in 2011 and 2014, respectively. While the European Union (EU) remains the largest trader, its trade ratio has stagnated rather than peaked. Notably, China has experienced the most significant decline in its trade ratio, which is not primarily attributed to increased protectionism but rather to a shift in its economic policy towards diversification. The primary factor behind the declining trade ratio has been the fall in commodity prices, rather than a decrease in trade volume. This price decline accounted for 5.7 percentage points of the 9.1 percentage points drop in the ratio of goods trade to world output between 2008 and 2020 (Wolf, 2022).

Figure 3: Trade Openness in the World’s Largest Economies (exports and imports as a % of GDP).

Foreign capital investments are often viewed as beneficial for enhancing production capacities, acquiring and assimilating new technologies, creating jobs, and most importantly, imparting skills and knowledge that collectively trigger a higher learning process. However, foreign investment may not always lead to the creation of new production capacities; instead, it can focus on acquiring existing capacities and exploiting the growing markets in developing countries. In cases of mergers and acquisitions, the production capacities may remain largely unchanged, while existing production organizations and labour relations often shift in favour of capital. Furthermore, many foreign direct investment (FDI) flows can be modes of round-tripping, designed to take advantage of tax havens.

Recent trends in FDI flows, as highlighted in the World Investment Report 2024, indicate that larger amounts of foreign investment are directed towards the Global North, or developed countries. Additionally, total foreign investment flows have declined over the past two years since the end of the Covid-19 pandemic. India’s aspirations to become the second-largest destination for FDI have faced significant setbacks. China’s share of global FDI inflows has decreased from 15.2% in 2020 to 12.3% in 2023, while India’s share fell from 6.5% to 2.1% during the same period (World Investment Report 2024).

In India, following the pro-market reforms of 1991, FDI inflows surged, averaging a growth rate of about 50.1% over the decade. However, this rate dropped to 30.7% in the 2000s and fell sharply in the 2010s, recording an average growth rate of only 4.6%. The IMF had previously stated that capital inflows would be directed towards capital-scarce economies, where returns would be relatively high, potentially increasing manufacturing in developing countries. Nevertheless, the automobile industry has shifted from the US and Canada to Brazil, Mexico, and South Korea, primarily driven by the pursuit of higher profits—either due to lower input costs or expanding markets. Despite expectations of rising FDI in India because of its growing middle-class market, workers’ wages have been kept low to make investments more attractive for FDI in the Global South (World Investment Report 2024).

Conclusion

While access to international markets can increase aggregate global wealth for developing countries, it often exacerbates inequality. This dynamic not only undermines the ability of international organizations to create institutions that could mitigate global inequality but also fuels resentment in the Global South.

The study reveals that globalization has curtailed the freedom of developing nations to choose economic policies tailored to their local contexts. Previously, during dirigiste regimes, petty producers and farmers enjoyed such autonomy. The withdrawal of state support has disproportionately affected poor households, leading to sharp increases in inequalities within many developing countries. These challenges are largely attributed to the neoliberal policies that define contemporary globalization. As a result, the capacity of governments to enact political interventions and introduce necessary changes has been significantly diminished.

Furthermore, institutions of international economic governance, such as the WTO, primarily reflect the interests of powerful, wealthy nations rather than those of poorer countries. Efforts to reform international trade, investment, labour, and environmental standards are still heavily influenced by the priorities of the Global North, perpetuating a system that disadvantages the Global South.

About the Author

Dr Kalim Siddiqui is an economist specialising in International Political Economy, Development Economics, International Trade, and International Economics. His work, which combines elements of international political economy and development economics, economic policy, economic history and international trade, often challenges prevailing orthodoxy about which policies promote overall development in less-developed countries. Kalim teaches international economics at the Department of Accounting, Finance and Economics, University of Huddersfield, UK. He has taught economics since 1989 at various universities in Norway and the UK.

References

- Girdner, E. and Siddiqui. K. (2008). “Neoliberal Globalization, Poverty Creation and Environmental Degradation in Developing Countries”, International Journal of Environment and Development 5(1): 1 – 27.

- Marx, K. (1974) Manifesto of the Communist Party, The Revolutions of 1848: Political Writings, Vol. 1, p.70, London.

- Siddiqui, K. (2023) “Marxian Analysis of Capitalism and Crises”, International Critical Thought, 13(4): 525-545.

- Siddiqui, K. (2020) “Globalisation, International Trade and the Developing Countries” European Financial Review, August-Sept. p.60 – 71.

- Siddiqui, K. (2020) “The Political Economy of Famines under Colonial India: A Critical Analysis” World Financial Review, July-August, p.56 – 70.

- Siddiqui, K. (2019). “Agriculture, WTO, Trade Liberalisation, and Food Security Challenges in the Developing Countries” World Financial Review, March-April, pp.31 – 40.

- Siddiqui, K. (2018). “Capitalism, Globalisation and Inequality” World Financial Review, Nov-Dec. p.72 – 77.

- Siddiqui, K. (2018). “David Ricardo’s Comparative Advantage and Developing Countries: Myth and Reality” International Critical Thought, 8(3): 1-28, Sept.

- Siddiqui, K. (2017). “Financialization and Economic Policy: The Issues of Capital Control in the Developing Countries” World Review of Political Economy 8 (4): 564 – 589.

- Siddiqui, K. (2016). “International Trade, WTO and Economic Development” World Review of Political Economy, 7(4): 424 – 450.

- Siddiqui, K. (2015). “Trade Liberalisation and Economic Development: A Critical Review” International Journal of Political Economy 44(3): 228 – 247.

- Siddiqui, K. (2015). “Foreign Capital Investment into Developing Countries: Some Economic Policy Issues” Research in World Economy 6(2): 14 – 29.

- Stiglitz, J. (2002) Globalization and its Discontent, New York: WW Norton & Company.

- Wolf, M. (2022) “Globalisation is not Dying”, Financial Times, 14 September, London.

{kind=link}